Are Your Accounts Payable Internal Controls Strong Enough?

Accounts payable internal controls matter because the potential for things to go wrong is never that far away.

PYMNTS.com wrote in July 2021 about scams that had impacted businesses, including a former bookkeeper for small businesses receiving a three-year federal prison sentence after stealing approximately $1 million from her clients. Then in early September, the New Hampshire Union Leader reported on the city of Nashua being scammed out of a little over $40,000 by someone who represented themself as a vendor agent.

These days, companies need strong accounts payable internal controls to protect themselves. Today, we’re going to explore some of the basics of accounts payable internal controls, tips and strategies including AP automation, and how Stampli can help companies improve their controls.

Basics of Accounts Payable Internal Controls

First, let’s review a few basics of accounts payable internal controls, including a simple definition of what they are and a review of things that can happen when poor controls exist.

Accounts Payable Internal Controls, Defined

Essentially, accounts payable internal controls are the safety mechanisms a company has for optimal performance from its AP departments. As we’ll explore in the second section here, accounts payable internal controls can vary greatly, everything from putting good policies and procedures in place to leveraging technology that can eliminate blindspots & uphold strict segregation of duties, such as AP automation.

What Poor Accounts Payable Internal Controls Can Lead To

When a company has strong internal controls, they protect themselves from a slew of issues (spend chaos, unapproved purchases, duplicate payments, etc.). But when internal controls are weak or ill-defined, they’re left to face repercussions that can be crippling to the organization.

Here are five things that can happen:

- Internal and external fraud: Weak accounts payable internal controls make it easier for fraudsters to steal. But remember that fraud risk is not limited to outsiders — your own employees know your systems best. While most employees would never dream of taking advantage, it happens all too often, sometimes from the employee you least expect.

- Tax issues: Lack of proper controls or inaccurate financial reports could result in you under- or overpaying on your taxes, neither of which is good for your bottom line.

- Extraneous invoices and payments: Maybe it starts with an honest mistake; for example, a vendor sends a second invoice because you’re closing in on the payment due date. Your processes aren’t quite perfect, so a second payment goes through. A less-than-scrupulous vendor might realize your accounts payable internal controls are not up to par and send a few extra invoices a year. If you don’t notice, you could lose thousands of dollars on duplicate payments.

- Inaccurate financial reporting: Your company, like most, makes critical business decisions based on financial documents like your balance sheet, P & L statement, and cash flow position. What if those documents are wrong due to poor accounts payable internal controls? Inaccurate financial statements and financial reporting can create huge issues for executives who rely on faulty information to make critical business decisions.

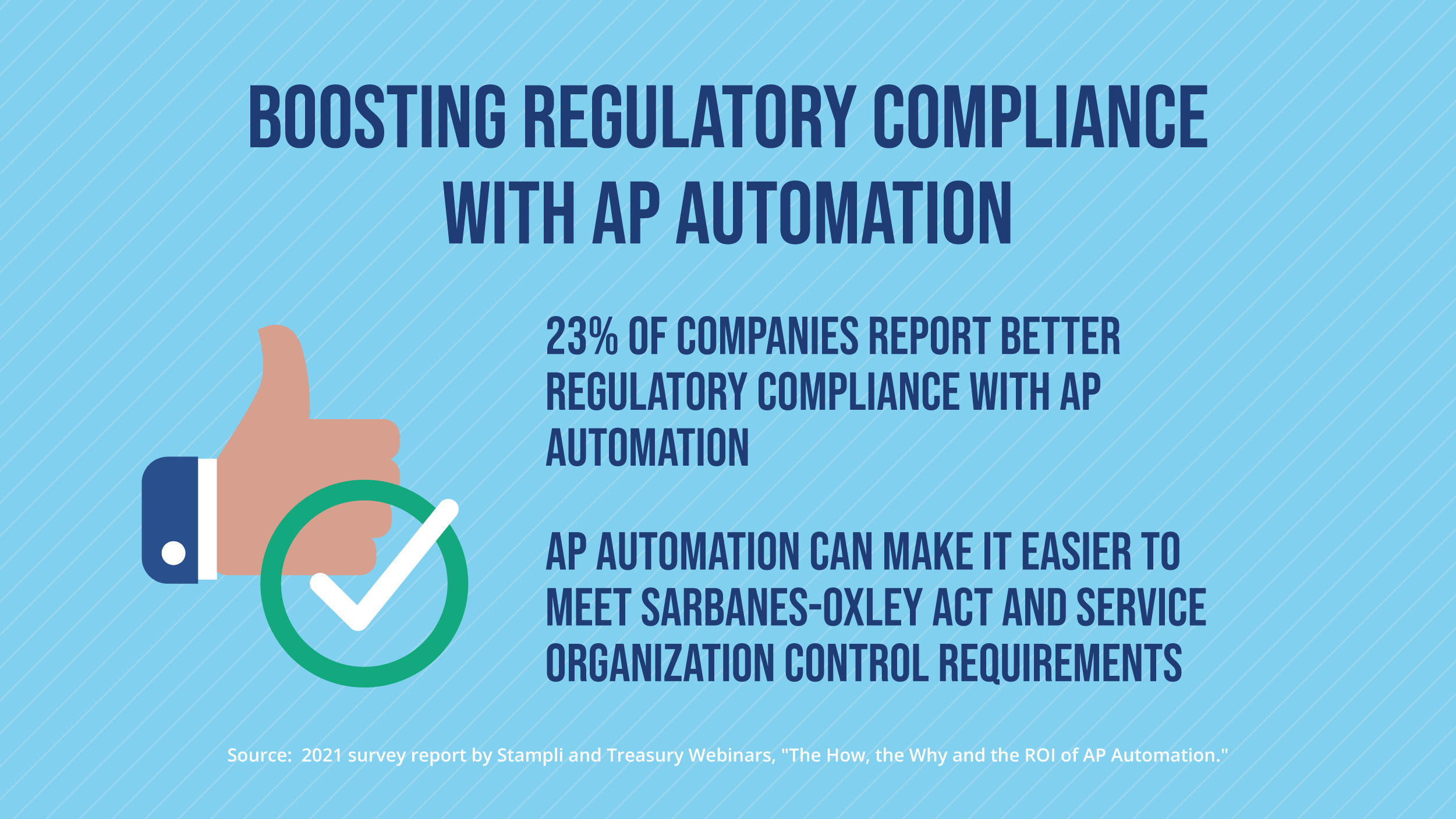

- SOX regulatory noncompliance: In 2002, Congress passed the Sarbanes-Oxley Act (SOX), aimed at protecting stockholders from accounting errors — and it upped corporate requirements for accounts payable internal controls. Other internal control audits such as the Service Organization Control (SOC) report serve similar purposes. When accounts payable internal controls are weak, your SOX and SOC certifications may be in jeopardy, but so is your ability to conform with a whole slew of other regulatory requirements.

4 Tips and Strategies for Boosting Accounts Payable Internal Controls

So, how do you make sure your company is well-protected from fraudsters, tax implications, and regulatory issues? It’s all about accounts payable internal controls – critical best practices to protect your company’s assets and best interests.

Here are four accounts payable internal controls worth considering:

1. Insisting on Teamwork

Ideally, employees should never be responsible for conflicting duties. There should always be a system of checks and balances in place ensuring that even long-time employees do not have access to multiple aspects of the AP process.

When too much responsibility is concentrated in the hands of one employee, bad things – such as fraud – can start to occur.

Depending on the size of your company, it may be necessary to assign tasks to another group or outsource accounts payables to achieve full segregation of duties. Or assign responsibilities in such a manner that deter the possibility of a fraudulent act being committed. Another thing to consider is splitting check printing and signing duties.

2. Automating Data Entry and Three-Way Matching

Humans can easily make mistakes when they’re inputting invoices details into an accounting system. They can also neglect to do three-way matching, which groups invoices with purchase orders and receipt reports to prove transactional validity.

Using AP automation software can eliminate much of the manual data entry process. This saves time, but is often far more accurate, as computers don’t make human errors, such as transposing two numbers or failing to add a dash to an invoice number.

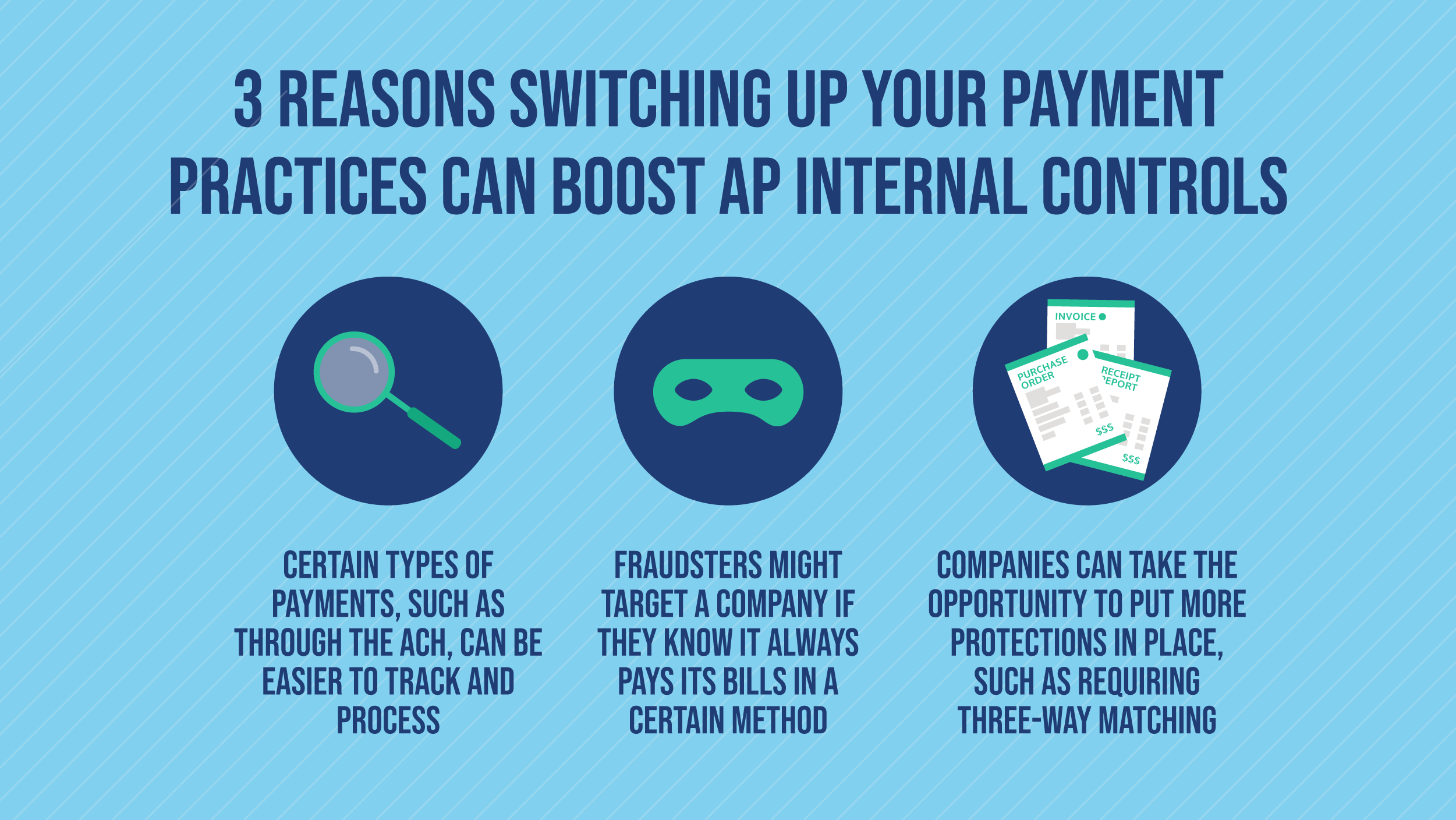

3. Updating Payment Practices

It might be awhile since some companies updated their payment practices. In a 2021 report by Stampli and Treasury Webinars, “How & Why Companies Choose Payment Types” the three most popular answers for how companies chose payment types were 46% of companies saying they made their decision based on processing costs, 37% following their suppliers’ preferences, 31% saying it was the way they’d always done things.

It can be good for companies to take a deeper look to know their payments are accurate, on time, and protected from fraud. While there isn’t a right or wrong way to make a payment, companies can switch to electronic or ACH payments, which can be easier to track and process. They can store checks in a secure location to prevent theft and make it easier to verify check numbers. They should also verify that whoever manages the master vendor file isn’t an approver.

4. Opting for AP Automation for the Entire P2P Process

Having good policies and procedures in place is a good component of accounts payable internal controls. Still, it’ll only go so far. We noted earlier that a company will want to automate its data entry and three-way matching. But that’s also only a start. The good news is it’s easier than ever for companies to implement AP automation software and invoice tracking software for their entire procurement to pay (P2P) process.

Aside from invoice scanning and three-way matching, AP automation can resolve invoice exceptions, a common issue in accounts payable. The software can also help with invoice approval workflows, ensuring that invoices clear internal hurdles and are checked over by higher-ups before being paid. Automating the AP process can also improve payment controls, with a duplicate payment search able to help reduce double payments, too.

How Stampli Can Help Improve Your Accounts Payable Internal Controls

For any company ready for the benefits of full-scale AP automation, Stampli stands willing and prepared to help make it happen.

Whether you’re a major enterprise-level firm with thousands of employees or a small operation that processes hundreds or thousands of invoices each month, Stampli can implement a SaaS-based system that will boost your accounts payable internal controls while also helping you process invoices faster and more cost-effectively.

Here are some of the accounts payable internal controls that Stampli offers with its AP automation platform:

Superb Collaborative Tools

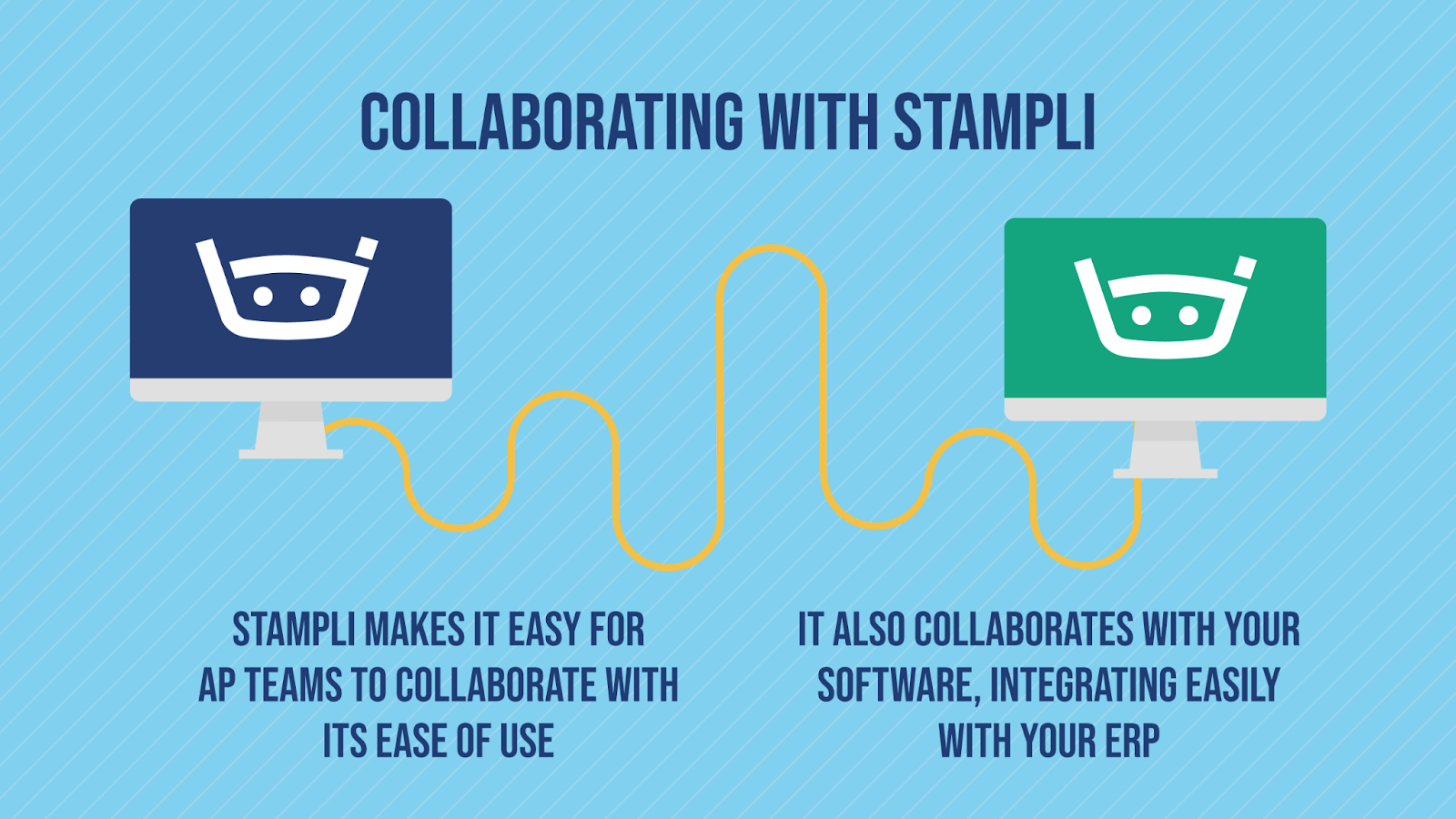

With Stampli, controls are in place from the first day to ensure teamwork and that duties aren’t being concentrated excessively in the hands of one employee.

Stampli’s AP automation platform enables superb collaboration, for many reasons. First, it’s intuitive and easy to use, ensuring that anyone on your team will feel comfortable with the software right away. It also keeps everyone on the same page – literally – with embedded communication tools on each invoice.

Poor visibility can be an issue with some AP automation systems, which can hamper collaboration. After all, it’s hard for people to take part in the P2P process without all of the necessary information. Stampli, however, can offer end-to-end visibility for everyone a company allows it to.

Data Entry and Three-Way Matching via Billy the Bot

As we noted earlier, data entry and three-way matching can be cumbersome for AP staff, with a strong potential for errors. Smart companies move as quickly as they reasonably can to remove these tasks from human staff and have them handled by artificial intelligence.

Stampli’s AI helper Billy the Bot makes data entry and three-way matching easy. Billy can automatically capture invoices from email, match those invoices to PO, and then send it off for approval in seconds. Billy does this by matching POs to the respective invoice by amount and PO number.

Billy can even work with a partial PO, selecting the items received and processing the remaining PO line items with the subsequent invoices and items upon receipt.

Invoice Exception Review

Invoice exceptions are bound to happen. Some sources online indicate that exception rates hover around a quarter of all invoices. While it’s important to review every last one of these exceptions to prevent payment of inaccurate, duplicate, or fraudulent invoices, having staff do this can quickly consume a lot of time.

Stampli’s AP automation platform makes it so that basic invoice exception reviews occur while staff is able to focus on other, higher-level tasks. The software monitors for changes or trends that look suspicious and flags them so your team can verify the change — or dig deeper if there’s an issue.

Payment Flexibility & Oversight

In addition to managing invoices and approvals, Stampli also offers payment flexibility which can be invaluable when streamlining your AP. With Stampli Direct Pay, teams can choose to conveniently pay vendors by ACH or check via Stampli, or opt alternative methods if they’d like to pay outside Stampli. In addition, Stampli offers the Stampli Card which helps companies manage credit card spend by allowing AP to issue unlimited cards to purchasers, but with added controls like spending limits, specific usage, and more. All purchases made with a Stampli Card are automatically added into the Stampli system and treated much like an invoice, giving control and oversight to AP while eliminating the need to manage card spend in a separate system.

In Conclusion

Accounts payable internal controls are vital and important. For companies that want to make sure they have the best controls in place, implementing a full-scale AP automation solution is indispensable.

Get a free demo of Stampli and see how easy AP management can be.