Ramp vs Divvy vs Stampli: Which financial platform is right for your growing business?

The modern finance stack promises to streamline everything from corporate cards to invoice processing, but not all financial platforms are created equal. As companies scale beyond basic expense tracking, the architectural decisions these platforms made early on become increasingly apparent — and consequential.

Ramp built a corporate card platform and expanded into accounts payable.

Divvy (now BILL Spend & Expense) built virtual cards for small business spend control.

Stampli designed comprehensive procure-to-pay (P2P) automation from day one.

These different origins matter more than marketing messages suggest. A platform’s foundational architecture determines how well it handles the complex financial workflows your growing business actually needs — multi-step approval chains, sophisticated vendor management, real-time ERP integration, and the seamless flow from purchase request to payment reconciliation.

This detailed comparison cuts through the feature lists and pricing pages to examine how each platform performs in the day-to-day realities of finance teams managing procurement, invoices, and supplier relationships at scale.

For finance leaders tired of choosing between sophistication and simplicity, this comparison will help you see which one will best serve the needs of your team.

Ramp: Sprawling ambition meets product sprawl reality

Since launching as a corporate card startup in 2019, Ramp has aggressively expanded into a comprehensive financial operations platform, adding expense management, travel booking, procurement automation, and select accounts payable features.

This rapid evolution demonstrates technical capability but raises a fundamental question: Can one platform excel across multiple complex financial functions?

Unlike focused SMB solutions like Divvy/BILL that optimize for specific business sizes — or specialized platforms that master one domain — Ramp’s strategy involves building competitive features across corporate cards, T&E, procurement, and accounts payable (AP) automation simultaneously.

It’s a breadth-first approach that can dilute the deep expertise businesses need as their P2P requirements become sophisticated.

Ramp’s key features

- Corporate payment solutions with spending controls

- Expense automation and receipt processing

- Travel management platform

- Procurement processing with some automated workflows

- Accounts payable processing with approval routing

- Financial operations analytics and reporting

Ramp’s strengths

Unified financial data across multiple payment types

For organizations seeking consolidated visibility across corporate cards, employee expenses, travel costs, and supplier invoices, Ramp provides this integration within a single platform architecture. Companies report efficiency gains from having all financial transactions flow through unified approval workflows and reporting systems.

Rather than managing separate platforms for cards (like standalone Divvy), basic AP processing (like traditional BILL setups), and specialized P2P automation, Ramp provides connected workflows across all payment types. This eliminates data silos and reduces reconciliation complexity.

Mid-market companies with straightforward financial operations appreciate having corporate cards, basic procurement, and AP automation managed through consistent user interfaces and unified vendor relationships.

But customer feedback suggests Ramp’s multi-product approach works effectively until businesses need advanced functionality in specific areas.

Complex procurement hierarchies, sophisticated vendor portal management, or enterprise-grade ERP integration depth won’t come standard.

Ramp’s weaknesses

Multi-product development constraints

Building competitive capabilities across corporate cards, travel management, procurement, and accounts payable simultaneously creates inherent resource allocation challenges that customer reviews consistently highlight.

G2 reviewers note that while Ramp offers features across multiple financial functions, depth in specific areas can lag behind focused competitors.

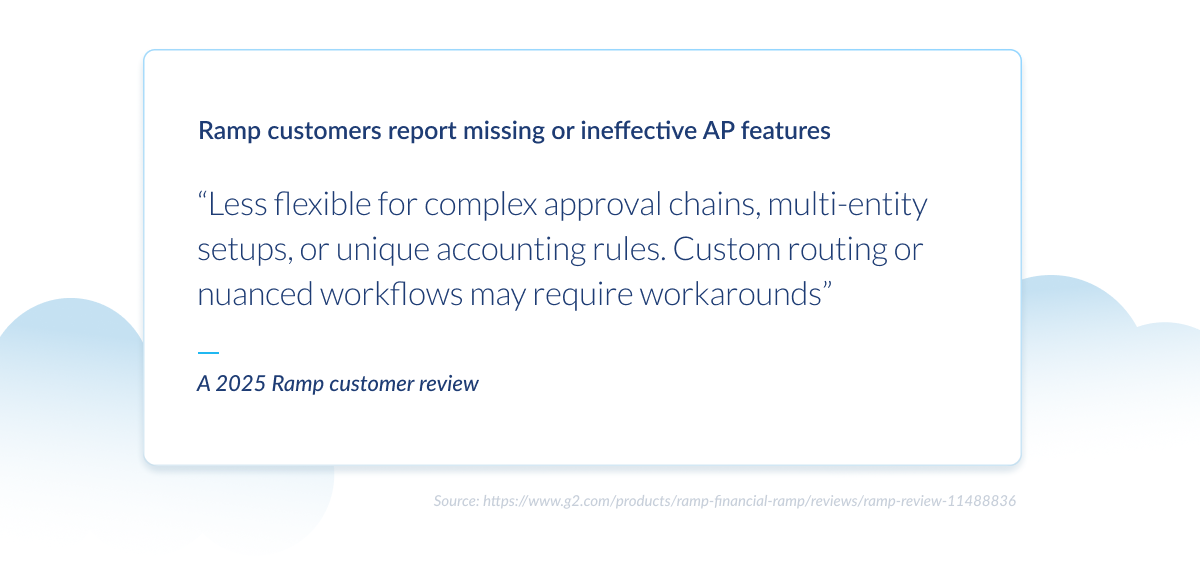

One verified customer explains, “Ramp is streamlined and easy to use [but] less flexible for complex approval chains, multi-entity setups, or unique accounting rules. Custom routing or nuanced workflows may require workarounds.”

Another reviewer details specific functionality limitations, saying, “the Bill Pay feature lacks a way to claim vendor credits and doesn’t batch invoices for a single payment. Each invoice is a separate payment. This creates more work for our Accounts Payable team and for our vendors.”

Ramp distributes engineering efforts across multiple financial product areas, potentially limiting advancement in any single domain.

Stampli’s team is dedicated to a single product and platform. Functionality is all part of a unified P2P ecosystem rather than a fragmented constellation of individual products.

ERP integration complexity across multiple modules

While Ramp offers accounting system connectivity, managing integrations across cards, expenses, travel, procurement, and AP modules creates coordination challenges that dedicated solutions typically avoid.

Customers say there are gaps in Ramp’s ERP integrations. “It is not fully integrated into our SAP system, requiring additional work on our end to transfer work order numbers and service order tracking,” explains one reviewer.

Rather than mastering deep ERP connectivity for specific use cases, Ramp must maintain reliable data sync across multiple financial function areas, creating potential points of failure for customers to experience.

Additional reviews highlight workflow gaps when using Ramp, “The Treasury syncing to Sage Intacct hasn’t always been smooth…I end up booking those manually.”

These challenges emerge when multiple product areas must coordinate seamlessly with external ERP systems.

Specialized P2P platforms like Stampli invest deeply in ERP integrations. Real-time two-way data sync, advanced matching logic, and custom field mapping are non-negotiable elements that modern financial operations require.

“Stampli provides a single source of receiving and processing ALL of our bills into one platform and syncing with NetSuite,” one customer explains. “We no longer have ‘exceptions’ with our complicated processes that a platform cannot handle.”

User experience consistency across expanding feature set

Ramp’s rapid feature expansion has created navigation and workflow complexity that customers increasingly report as functionality spans multiple financial domains.

Recent customer feedback reveals usability challenges.

“Ramp is clearly trying to innovate and remain ahead of the curve,” says one Capterra review. “The most recent update to the website has overcomplicated the end user experience.”

As the platform scope expands, user administration has also become more complex.

Ramp customers mention that they’re unable to support multi-functioning roles within the system.

Stampli customers, in contrast, consistently praise the ease of use and attention to detail. “Since everything is in one place, it saves a lot of time and reduces a lot of manual work,” says one Stampli customer in their G2 review.

Ramp pricing

Ramp operates through interchange fee revenue rather than traditional software subscriptions, creating economic incentives that influence platform development priorities and customer payment method choices.

Current pricing structure:

- Free plan: Core functionality at $0 monthly cost with basic features across all modules

- Plus plan: $15 per user monthly with advanced automation and premium integrations

- Enterprise: Custom annual contracts for organizations requiring extensive customization

Since interchange fees from card transactions provide primary revenue, Ramp has economic incentives to prioritize card usage over alternative payment methods.

While initial pricing appears low compared to specialized solutions, organizations requiring comprehensive P2P automation may discover that free or low-cost multi-product platforms lack the functionality depth they actually need.

This is different from a solution like Stampli, which offers transparent and all-inclusive pricing.

Divvy (now BILL Spend & Expense): Stitching together a financial system

Divvy began with a “free virtual cards” model that challenged traditional corporate card offerings, but its 2021 acquisition by BILL transformed it from a standalone spend management platform into the card component of BILL’s broader finance cloud ecosystem.

While this integration promises comprehensive financial operations for QuickBooks-centric businesses, it reveals the challenge of combining a card-first platform with traditional accounts payable software.

These two different approaches to financial management that don’t always align seamlessly.

Divvy’s key features

- Real-time budget enforcement and spending limits

- Virtual and physical cards with spending controls

- SMS receipt capture and expense categorization

- Light bill pay integrated with BILL’s AP platform

- QuickBooks integration (no additional cost)

- BILL ecosystem access for more comprehensive AP automation

Divvy’s strengths

Spend control that prevents overspending

Divvy’s real-time budget enforcement stops transactions before they exceed approved limits. This proactive approach appeals to businesses struggling with expense policy compliance and budget overruns.

Finance teams can set department, project, or vendor-specific spending limits that automatically decline transactions, eliminating approval delays and reducing manual oversight requirements.

However, this strength in spend control can become a constraint when businesses need sophisticated procurement workflows or complex supplier payment capabilities that require more flexibility than automatic decline rules provide.

While real-time budget blocks work well for card transactions, companies processing supplier invoices, purchase orders, and complex approval hierarchies often discover that spend prevention tools can’t replace comprehensive procurement-to-payment workflows.

Divvy’s weaknesses

Acquisition integration challenges

The 2021 merger of Divvy’s card-first platform with BILL’s traditional AP software created a hybrid solution that customers must navigate across two distinct financial management philosophies.

While both companies promise “seamless integration,” the reality often involves managing separate workflows for card spending versus supplier invoice processing.

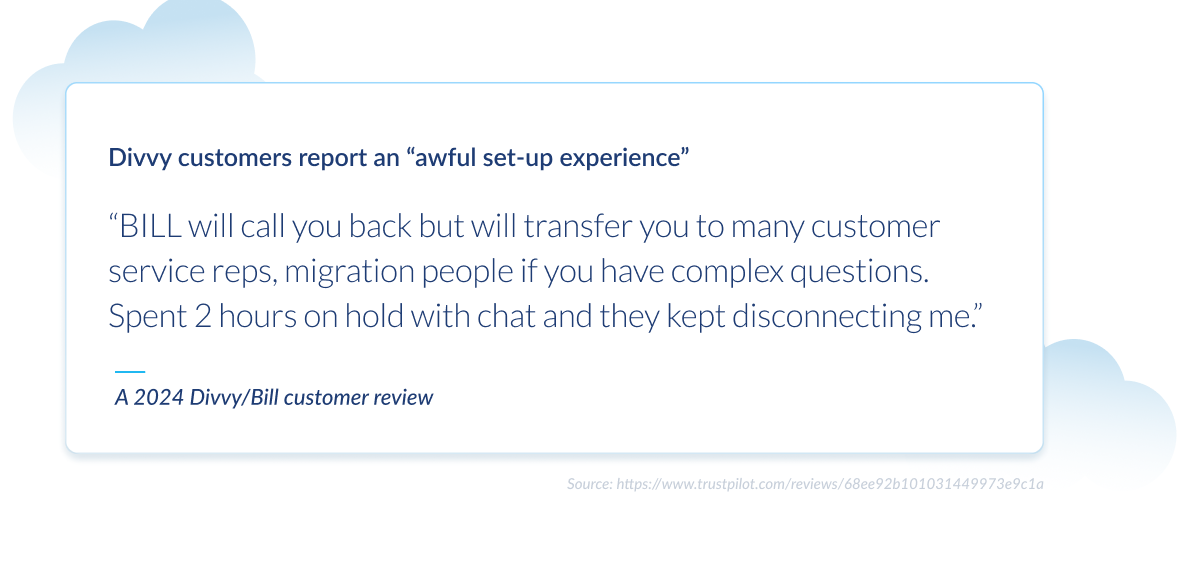

Plus, customers say that the setup and support experience can be frustrating.

“Awful set-up experience,” says one BILL customer. “BILL will call you back but will transfer you to many customer service reps, migration people if you have complex questions. Spent 2 hours on hold with chat and they kept disconnecting me.”

While even multi-product platforms like Ramp that built everything on the same foundation, Divvy customers navigate the complexity of truly separate systems that were merged through acquisition.

Both of these approaches struggle to achieve the kind of seamless integration of Stampli, a purpose-built P2P platform where cards, expenses, and invoice processing flow through unified workflows.

QuickBooks dependency limitations

While Divvy/BILL’s tight QuickBooks integration appeals to small businesses, this focus creates constraints for companies using other ERPs or requiring enterprise-grade financial operations capabilities.

Companies growing beyond small business needs often discover that their financial operations have outgrown both QuickBooks’ capabilities and Divvy’s QuickBooks-optimized workflows.

Some customers even say that the QBO integration is not always reliable. “Sometimes transactions will not sync,” one BILL customer explains. “I notice that it is always specifically three employees whose transactions will not sync … signing up for Bill Spend and Expense was a bit tricky because they experienced many hiccups.”

This is one of the key reasons Stampli supports 70+ ERPs with native, real-time integrations. Because your business shouldn’t have to change its entire tech stack to work around your financial automation platform.

Stampli customers frequently mention the integrations and seamless setup as one of their favorite things about the platform. “Stampli integration was efficiently completed within a day,” says one customer, “and we were able to implement the new processes within less than a week.”

Limited P2P depth beyond spend control

Despite BILL’s AP automation capabilities, the Divvy integration focuses primarily on spend control and basic bill pay rather than the comprehensive procurement-to-payment workflows that scaling businesses require.

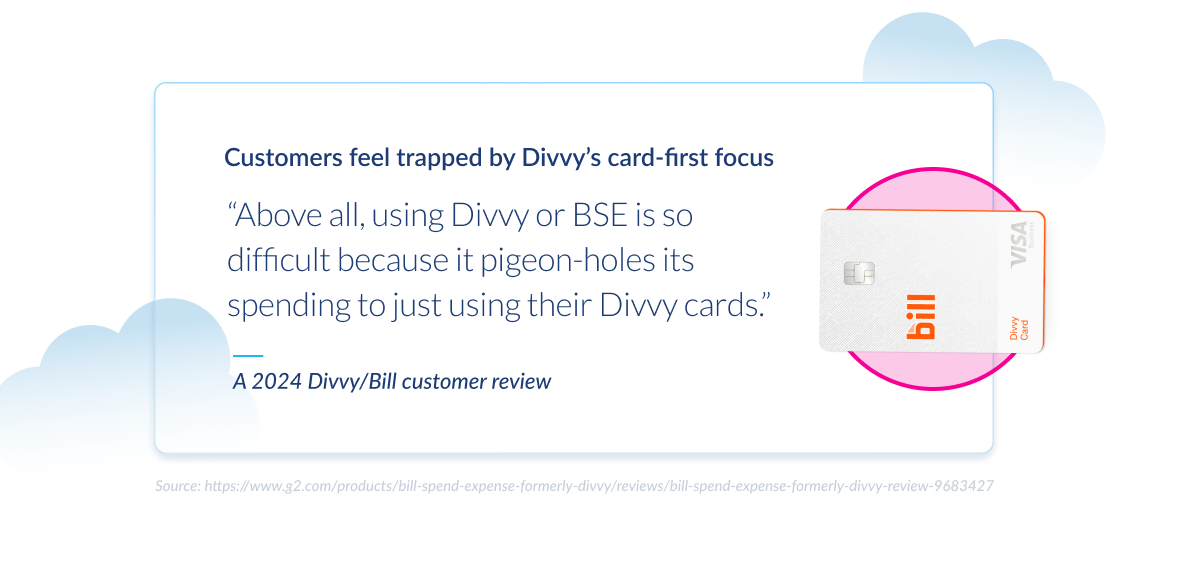

One customer expresses their frustration with the fragmentation and functionality limitations in a review, saying, “above all, using Divvy or BSE is so difficult because it pigeon-holes its spending to just using their Divvy cards.”

They went on to say:

“What’s worse, if you try making reimbursement requests, there’s a ton of extra work involved, and that’s just for reimbursements. If we want to make ACH, check, or wire payments, they have to be done outside of Divvy. We want to buy into Bill.com, but it lacks travel management. We need a centralized platform that can handle AP, travel, personal card spend, security, and everything else.”

While Divvy excels at preventing overspending through real-time controls and BILL handles traditional AP processing, the combined platform lacks the purpose-built P2P sophistication that companies need for comprehensive procurement-to-payment automation as they scale beyond basic spend management.

Divvy/BILL pricing

Divvy maintains its original “free” card platform model, but accessing BILL’s AP functionality requires paid upgrades that can significantly increase total cost of ownership for companies needing full financial operations capabilities.

Current pricing structure:

- Divvy spend management: Free with unlimited virtual cards, basic expense tracking, and QuickBooks integration

- BILL AP + Divvy: Starting at $45/month for AP automation features integrated with Divvy spend controls

- BILL enterprise: Custom pricing for advanced multi-entity, workflow customization, and premium ERP integrations

The “free” reality for P2P operations:

- Free tier works for basic card spend control but limits companies to expense tracking without comprehensive supplier payment capabilities

- AP automation features require paid BILL subscriptions, making total costs comparable to dedicated P2P platforms

- Advanced features like multi-entity support, complex approvals, and non-QuickBooks integrations require enterprise-level contracts

Cost escalation factors:

- Transaction volume-based pricing on BILL side can create unpredictable monthly costs

- Multiple user fees across both Divvy and BILL platforms for different functional roles

- Integration costs for ERPs beyond basic QuickBooks connectivity

Unlike transparent subscription models from specialized platforms like Stampli, Divvy/BILL customers must navigate hybrid pricing across two different billing systems. They pay once for card management and another price for AP automation, which can increase total cost of ownership and, ironically, make it difficult to predict and budget total spend.

Stampli: Procurement-to-payment built right the first time

Finance teams shouldn’t have to choose between a card company that added AP later and a free SMB tool welded onto an AP suite.

Stampli skips the retrofit by starting — and staying — with procure-to-pay.

One data model, one UI, one AI brain. No modules bolted on after a funding round, no surprise platform hand-offs between different product interfaces.

While platforms like Ramp distribute development resources across corporate cards, travel booking, and AP automation, and Divvy/BILL navigates dual-platform complexity from their acquisition, Stampli concentrates a decade of engineering investment specifically on procurement-to-payment excellence that works for your business.

Stampli’s P2P-native capabilities

- Unified P2P automation: Requests, POs, invoices and payments live in the same record; nothing syncs “later” or requires separate user interfaces

- Billy, Your AI Employee: Over a decade of P2P-specific learning delivers accurate PO matching and auto-coding that improves with your organization’s patterns

- 70+ native ERP connections: Real-time two-way sync with NetSuite, Sage Intacct, SAP, Microsoft Dynamics, QuickBooks, and specialized industry systems

- Adaptive P2P workflows: Conditional routing by spend category, entity, or budget line without hard-coding workarounds or IT dependency

- Stampli Direct Pay: ACH, wire, check and virtual card from the same approval flow with zero interchange steering

- Budget management built in: Budget checks are incorporated into request workflows so approvers understand spend context before approving new purchases

Stampli’s strengths

Deep specialization focused on your P2P workflow

While Ramp juggles five product lines and Divvy coordinates two acquired platforms, Stampli pours every development sprint into richer P2P automation.

One customer explains how they experience the difference:

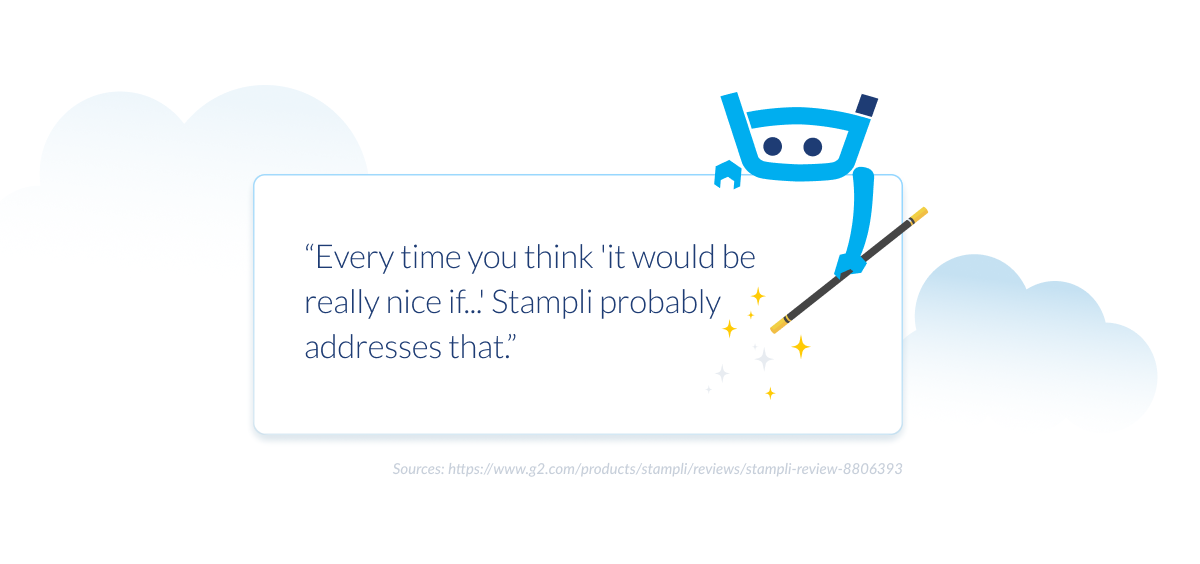

“It’s clear that Stampli was designed and improved by AP professionals. Every time you think ‘it would be really nice if…’ Stampli probably addresses that. We’ve eliminated a tough-to-fill and high-turnover AP position in our department, and still have more time within our group.”

Rather than competing for engineering resources across multiple financial functions, Stampli’s P2P specialization means continuous enhancement of procurement workflows, invoice matching logic, and approval intelligence that generalist platforms can’t match.

Purpose-built AI vs adapted automation

While competitors offer general automation adapted from other financial use cases, Stampli’s Billy leverages nine years of procurement-to-payment specific training. This specialization shows in real customer results.

Matthew Andersen, CFO at Superior Masonry, explains the difference: “Billy’s suggestions are 98% accurate — my team moved from coding to reviewing. Stampli has given us the ability to focus on the bigger strategic mission.”

Fast implementation without functionality trade-offs

Enterprise-grade P2P automation shouldn’t require months-long implementations. Stampli customers go live in weeks, not quarters, while maintaining sophisticated workflow capabilities that basic solutions can’t provide.

Implementation advantages:

- Dedicated P2P experts guide configuration rather than generic platform trainers managing multiple product areas

- Workflow mapping included that adapts to existing processes instead of forcing standardization across departments

- ERP connectivity pre-built for 70+ systems without custom development or lengthy integration projects

Median Stampli go-live requires 28 days with dedicated P2P experts, compared to multi-product platforms requiring separate training for different modules or SMB solutions that hit scaling limitations as complexity increases.

“The implementation was a very easy process and customer support walked us through each step necessary to go live,” says one customer.

Stampli consistently ranks highest in G2 for:

- Implementation Index (Ease of Setup, User Adoption, Time to Go Live)

- Relationship Index (Quality of Support, Ease of Doing Business)

- Results Index (ROI and Meeting Requirements)

Enterprise ERP depth vs platform constraints

Stampli customers report seamless ERP connectivity that adapts to their existing financial architecture rather than requiring workarounds for platforms optimized for different use cases or business sizes.

Whether organizations run NetSuite multi-subsidiary configurations, SAP environments, or sophisticated Sage Intacct setups, Stampli mirrors charts of accounts structures in real time and makes complex workflows seamless.

Stampli pricing

Stampli operates on simple subscription economics:

- Subscription-based platform fee

- Unlimited basic users and unlimited vendor portal users

- Direct Pay available with predictable fees (ACH, checks, international payments)

- One-time implementation fee applies; includes configuration, training, and customer success support

Stampli’s success depends on customer P2P success, not payment method steering or user limitation strategies that create artificial constraints as businesses grow.

Which platform fits your finance stack?

Every platform in this comparison solves a different primary problem. Match that problem to your reality, and the decision becomes straightforward.

Choose Ramp if your top priority is controlling corporate card spend across many employees and you’re comfortable with basic invoice workflows layered on top. Ramp works best for high-growth companies whose transaction volume is still more card-heavy than invoice-heavy, and who can work within their architectural constraints.

Choose Divvy (BILL Spend & Expense) if you’re a QuickBooks Online-centric small business that needs real-time budget guardrails and virtual card controls. Divvy’s spend management approach works well for <50 invoices per month, but procurement controls and deep ERP synchronization are outside its core competency.

Choose Stampli when invoices, purchase orders, and supplier payments are central to your operations.

Stampli’s purpose-built P2P architecture delivers:

- Real-time, two-way sync with 70+ ERPs, not daily batch uploads

- Rapid implementation and delivers documented 75% faster invoice processing

- G2 #1 ranking in Implementation Index

The strategic reality

Card-first platforms like Ramp excel at spend control but face architectural limitations when handling complex AP scenarios. Expense-focused solutions like Divvy provide excellent budget controls but lack the workflow sophistication for comprehensive procurement-to-payment operations.

Stampli eliminates the need to choose between spend management and AP automation. You get both. Plus the procurement integration and ERP depth that neither card-first nor expense-first platforms can deliver.

Your platform choice determines whether you’ll outgrow your solution as you scale, or have one comprehensive system that adapts to increased complexity. Purpose-built P2P platforms like Stampli give you both immediate functionality and long-term scalability without forcing architectural compromises.

Ready to see if Stampli is right for you?