What are B2B Payments? Definition, Methods, Trends & Companies

B2B Payments Definition

The definition of business-to-business payments or B2B payments is the transfer of value denominated in currency from buyer to supplier for good or services supplied. B2B payments can be a one time or recurring transaction depending on the contractual agreement made between the buyer and supplier. B2B payments are more complex than business-to-consumer or B2C payments, since B2B payment processing requires more time to approve and settle the transaction which can take days or weeks. Whereas in B2C payment processing, the transaction is typically settled on the spot.

Types of B2B Payment Methods

The most common types of B2B payment methods are paper checks, ACH payments, wire transfers, credit cards (AP credit cards), and cash. Each B2B payment method has its own set of benefits compared to the next and here is how the different types of B2B payment methods differ.

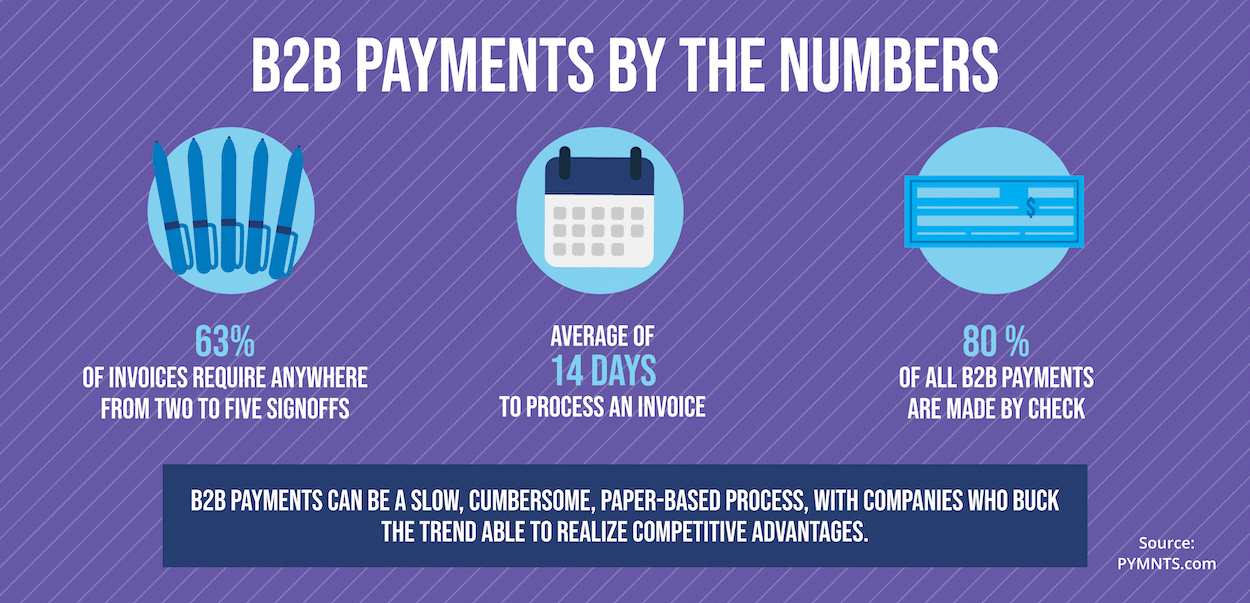

Checks: Despite technological advances in 2020, checks remain the most-common method of B2B payment, used for 80 percent of all business-to-business payments, according to PYMNTS.com.

ACH payments: Automated clearing house payments or ACH payments are electronic payments and have become commonplace in recent years, with the National Automated Clearing House Association reporting that the ACH Network processed a staggering 24.7 billion payments in 2019, or more than three for every person in the world. They’ve also become common for B2B transactions, with 93 percent of workers receiving payment through direct deposit, per a 2019 survey. NACHA also projects that ACH payments will soon account for around half of all B2B payments.

Wire transfers: Wire transfers represent less than 1% of the total number of B2B payments, but make up 93% of the total amount because they are often high-value payment transactions according to Glenbrook. While wire transfers don’t account for a fraction of payments that checks do — with a recent Federal Reserve study noting “if only 2 percent of the current corporate check volume moved to wire, wire volume would increase 47 percent” — they still accounted for 95 million payments according to that study. These payments typically happen one of three ways: Fedwire, CHIPS, and RTP.

Credit cards: Credit cards aren’t overly popular in the B2B payment world, since some vendors prefer to duck the 3-4 percent processing fees that credit card companies often charge. That said, many businesses still make frequent use of plastic and are sometimes willing to accept payment by them. Payments Journal found that 93 percent of small businesses were accepting Visa as of 2019.

Cash: Cold hard cash remains a surprisingly common form of B2B payment, with 70 percent of small businesses still accepting it as of 2019, according to Payments Journal.

The Current State of the B2B Payment Space

The world of B2B payments is tough and getting tougher. With accounts payable work already a sometimes-thankless chore of hitting deadlines and keeping vendors and contractors satisfied, a global pandemic and other pressures in 2020 have added a whole another layer of tension. But those who can rise above the tension can be richly compensated, with global payment volume in the B2B space estimated at approximately $120 trillion in recent years.

In this section, we’ll take a look at the current state of the B2B payment space (and associated problems), how COVID-19 and other factors are encouraging rapid change, and how electronic payment systems can help businesses thrive amidst the uncertainty.

Here’s the current state of the business-to-business payment space as well as some of the problems that are associated with typical payment methods.

B2B Payment Method Issues

Needless to say, there are all sorts of problems with different B2B payment methods, particularly ones that aren’t made electronically. As any business person who’s filed a tax return could attest, it can be difficult to show proof of cash payment to a vendor. And that’s far from the only problem associated with accepting cash, even if some vendors insist on it. As it is with checks, processing and document reconciliation will take longer than it should with electronic solutions.

ACH payments, wire transfers, and credit cards make the process go a little smoother, though companies that hope that merely encouraging these types of payments without implementing a fully-integrated, payment agnostic accounts payable automation system are probably leaving money on the table.

Traditional, non-automated payment systems drive up invoice processing expenses, offer poor visibility, less actionable data, and longer payment cycles. And in 2020, the problems are only getting worse.

B2B Payment Trends

The world of B2B payments has changed dramatically in 2020, these trends are primarily due to the same reason so many other parts of the world have changed: the novel coronavirus, or COVID-19 pandemic and its cascading series of impacts.

1. COVID-19: A New B2B Payment World

COVID-19 has fundamentally altered how businesses function for the foreseeable future, from widespread wearing of facemasks in customer-facing businesses such as retail to an increase in patio dining for restaurants, and other retailers moving goods and services outdoors. COVID-19 has also impacted B2B organizations from essential businesses to organizations that have shifted to a remote workforce.

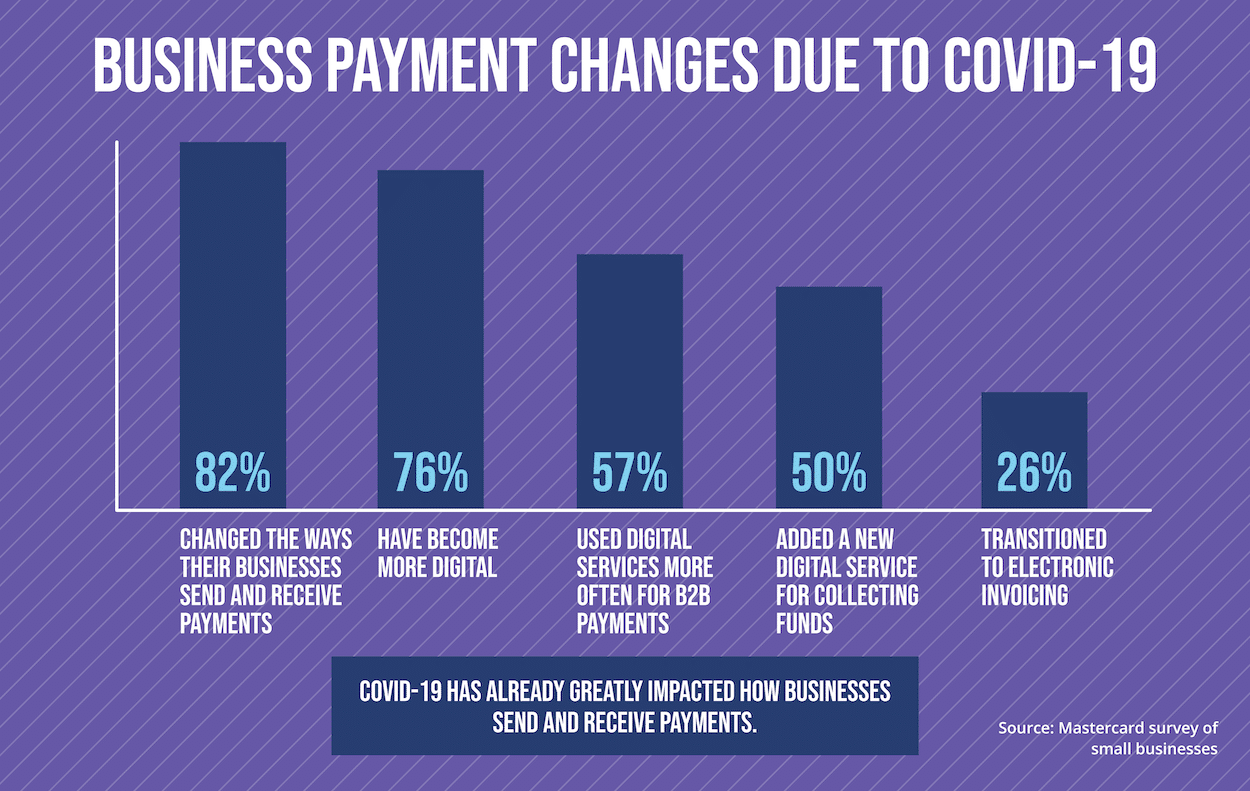

The world of B2B payments has been affected as well, with 76 percent of respondents saying in a recent Mastercard survey of small businesses that the pandemic had forced them to become more digital and 82 percent changing the ways their businesses send and receive payments. Fifty percent of survey respondents reported adding “a new digital service for collecting funds while (roughly) one in four transitioned to electronic invoice processes,” according to a press release about the study.

In addition, 68 percent of small businesses in the survey said cash deposits took too long, forcing them to decrease use of cash and checks “more than any other payment types during the pandemic,” the press release noted. More than half of small businesses also reported using digital services more often for B2B payments.

Benefit of electronic payments: Digital payments offer many benefits seemingly tailored to a COVID-19 world, from decentralization to automation to not requiring any touch. Solution providers like Stampli have risen to meet the challenges posed by COVID-19, increasing capacity to help more firms get up and running with remote accounts payable operations.

2. Rising Threat of Financial Crime

Aside from the lifestyle changes mandated by public officials during the pandemic, the economy has experienced significant volatility since early 2020. As the saying goes, desperate times breed desperate measures, with businesses facing rapidly-increased odds of financial crime associated with their payment processing.

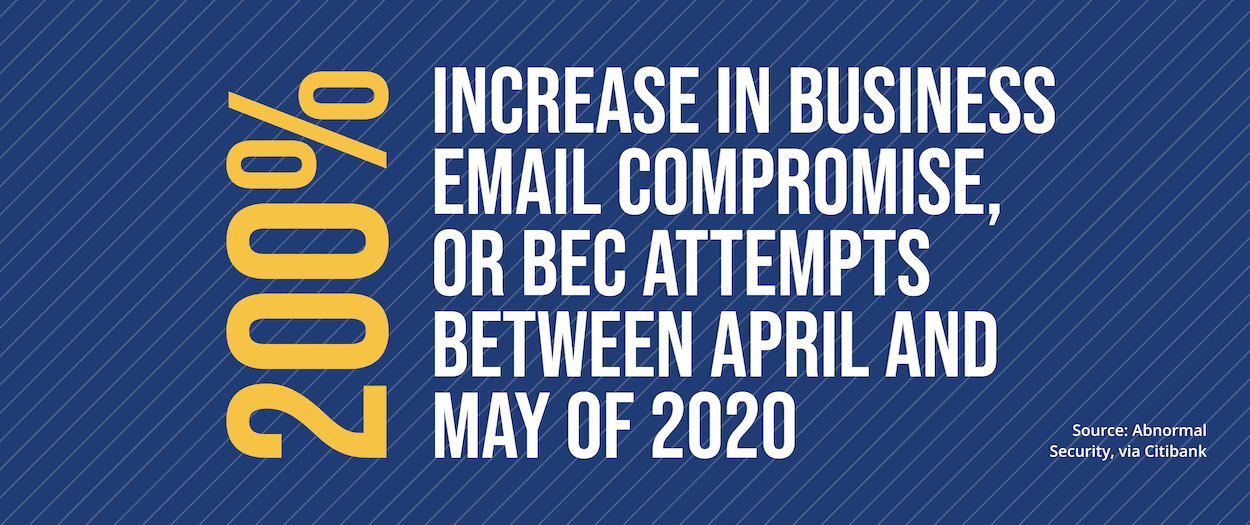

Citibank warned in July of the rising risk, stating that already fraudsters were overwhelming targeting businesses before the pandemic, with 81 percent of payment fraud ploys in 2019 made against businesses, per the 2020 AFP Payments Fraud and Control Survey. That article noted that fraudsters typically preferred invoice fraud or business email compromise (BEC) and that security solution vendor Abnormal Security attested that “BEC scams involving payment and invoice fraud” rose by 200 percent between April and May.

Benefit of electronic payments: In a COVID-19 world, businesses need every light they can to shine on possible fraud. Payment systems offer built-in protections, from three-way matching of documents assuring that transactions are valid to tools that can flag suspicious or outright phony invoices.

3. Faster Expectations

Businesses are also seeing increased pressure to pay their bills sooner, with the pandemic hurting cashflow in many sectors. Where a business might have once had upwards of a month, with fairly leisurely terms with their client for getting payment in, today they might be getting an anxious call as soon as that invoice is sent over.

Benefits of electronic payments: Electronic payment platforms offer quicker payment cycles for both accounts payable and accounts receivable.

4. More Remote Employees, More Remote Payment Approvals

More employees than ever are working from home, with 97 percent of North American office workers in a recent survey by Global Workplace Analytics saying they’d “worked from home for more than one day per week, even though 67 percent had not participated in remote work previously,” according to Entrepreneur magazine. By extension, this likely means that more payments are being approved remotely these days, which was already a trend pre-pandemic.

Benefits of electronic payments: Invoice processing, approvals, and payments can be processed from anywhere at any time with B2B payments automation solutions.

5. More Payment Devices, Courtesy of the Internet of Things

Quietly, the world is also in the midst of a revolution for the Internet of Things, essentially the idea of a decentralized network of devices capable of accessing the web, from refrigerators to gaming platforms to home security systems. McKinsey reported last year that IoT technologies had rose from 14 percent in 2014 to 25 percent and that the number of IoT-connected devices could hit 43 billion by 2023.

Benefit of electronic payments: As the number of IoT-connected devices continue to rise markedly in the years to come, businesses are going to want more and more ways to pay. Electronic payment systems can be updated automatically by their vendors to recognize seemingly whichever devices a critical mass of businesses will have decided to use for payment within a few years.

Action Item Checklist for Electronic B2B Payment Companies

This guide helps business directors and others considering adopting electronic B2B payments, offering the benefits and how to go about doing it. Choosing a business-to-business payment system doesn’t have to be that long of an undertaking, though a few best practices are advisable. Here’s what to look for in B2B payment companies.

Payment Freedom

Identify B2B payment providers that have invoice approvals built in, with option to pay how you’d like to pay. While touchless checks and ACH payments are the most common and widely utilized, opt for a B2B payment system with approval workflows to provide oversight and ensure control. Then see if you can pay outside of the system because payment freedom is yours to lose, that in addition the benefits associated with not being locked into a single payment system – such as rewards or for convenience.

Look for Experts, Know Their Lingo

Just Google “AP Automation” and multiple pages of possible solution providers pop up. Businesses looking for ACH or check payment systems will want to look toward experts in the space and will be able to spot them by the sorts of things they talk about on their websites and in their blogs.

Leaders in B2B payments talk about how they offer a flexible solution which aligns to your accounts payable payment processes. They understand how much the business world has evolved in recent years and this comes through in how they talk about their solution.

Identify a Secure Solution

As noted earlier, cyber crime is on the rise for businesses and was an area of concern even before COVID-19. Thus, any business considering the transition to electronic payments should identify a secure solution at the top of their checklist which is part of the Nacha Affiliate Program, in addition to AICPA SOC 1 and SOC 2 compliant.

Verify Audit Trail of Bank Data Updates & Payments

Last but not least, verify the B2B payment solution offers an audit trail of all activities related to payments. The audit trail should be available in the payments feed or payment details page. These audit trails typically display user data, including payment activities with date stamps from the time a payment was created to approvals for submission.

Want to have more control over your B2B payment process? Read how Stampli Direct Pay provides maximum flexibility and control over B2B payments by enabling you to pay by ACH, check, or pay your way.

B2B Payments FAQs

Business-to-business payments or B2B payments are transactions processed between buyer and supplier for goods or services delivered.

B2B payment methods range from Electronic Funds Transfers (EFTs) in form of Automated Clearing House (ACH), wire transfers, virtual cards, and eChecks — to paper forms such as checks or cash.