What are ACH Payments? Definition, Processing & Requirements

What are ACH Payments?

An automated clearing house payment or ACH payment for short, is a form of electronic funds transfer sent from one bank account to another and can be either a credit or a debit. ACH payments are also US-based bank-to-bank transfers that are aggregated and processed in batches through the Automated Clearing House network, run by NACHA. ACH payments can be referred to as direct payments.

NACHA, formerly the National Automated Clearinghouse Association manages the ACH network. NACHA is a self-regulating non-profit organization with supervisory and rule-making functions for ACH transactions, funded by US financial institutions. All ACH transfers are processed through the ACH network run by NACHA, the centralized system that securely transfers money to the proper bank account.

Given that ACH payments are both digital and automated, they are more reliable and quicker compared to the paper equivalent check, which helps streamline account payable processes. ACH is a separate network than the major credit card systems like Visa, Mastercard, American Express, etc.

ACH Payment Requirements:

- The name of the financial institution receiving the funds (bank or credit union)

- The type of account at that bank (checking vs. savings)

- The ABA routing number of the financial institution

- The recipient’s account number

ACH payments are extremely common. In February 2019, The ACH Network set a record in by sending more than 100 million ACH payments in a single day.

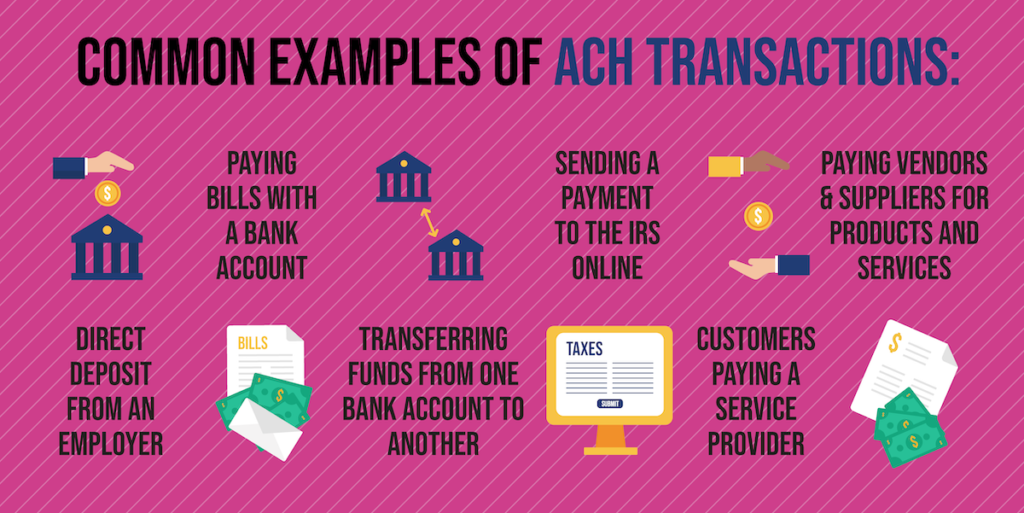

ACH Processing Examples:

- Direct deposit from an employer (your paycheck)

- Paying bills with a bank account

- Transferring funds from one bank account to another (Venmo, PayPal, etc.)

- Sending a payment to the IRS online

- Customers paying a service provider

- Businesses paying vendors and suppliers for products and services

In this post, we’re going to unleash an incredibly thorough examination of ACH payments from the ground up. We’ll define the term, discuss the benefits, describe the functionality, and of course, explain how you can set up ACH payment processing at your own organization.

We have a lot of ground to cover, so let’s get started.

That’s right, you can pay invoices with ACH, and if you work in accounts payable, that’s likely what you’re most interested in—we’ll get to that part a bit later in this post.

There are two types of ACH transfers: ACH credits and ACH debits.

The key difference is that an ACH credit is the money that’s delivered into an account, while an ACH debit is the money that’s pulled out of an account. There are actually several different types of ACH debits that have different purposes and functionality (such as one-time vs. recurring payments). Each type of debit has its own Standard Entry Class (SEC) code—you can see the full list here.

How long does it take to process an ACH payment?

While ACH is fairly quick; it’s generally not instantaneous. Transfers typically take around 3-5 business days, but factors such as time of day and day of the week play into exactly how long the funds take to transfer along with the type of ACH payment. Outside of the typical ACH, there are Next Day ACH transfers and Same Day ACH transfers. Next Day ACH transfers can settle in 1-2 days. While Same Day ACH transfers can be made within the same business day or next depending on when the ACH payment was initiated. Moreover, Same Day ACH transfers typically come with a same day processing fee.

What is the transaction cost for ACH payments?

According to NACHA (National Automated Clearing House Association), which is the governing body of ACH payments and transfers, the average processing fee for an ACH payment is 11¢.

There are some factors that can influence the cost per transaction, however. For example, the volume of transactions you plan to process—the more payments you send, the cheaper your per-transaction fees will be. This is because there are several different types of fee structures you can use.

By this time, you should have a pretty thorough understanding of the nuts and bolts of ACH payments. Let’s zoom out a bit and take a look at the business implications—both financial and operational—that ACH can provide for your organization.

Benefits of ACH Payments

We are going to primarily discuss the benefits of using ACH payments from a business perspective, but there are plenty of benefits to consumers as well that you can check out. But for organizations that need to issue payments and/or money transfers (aka every business on the planet), ACH comes with plenty of attractive benefits. Let’s take a look:

1. Convenience

If you’re comparing the convenience of ACH vs. writing checks, then there is no comparison. No paper checks, no file cabinets to store the checks, no pens to sign the checks, but from a convenience standpoint, ACH is indisputably superior to checks when it comes to the time it takes to cut the check and for a vendor to have the funds available in their account. It’s also not uncommon for vendors to set checks as their preferred method to receive payments, therefore, checks continue to be used throughout industries.

2. Lower cost than credit

Credit systems have a similar convenience as ACH, but can also carry significantly more costs. This is especially true for businesses that are going to accept lots of payments on a recurring basis.

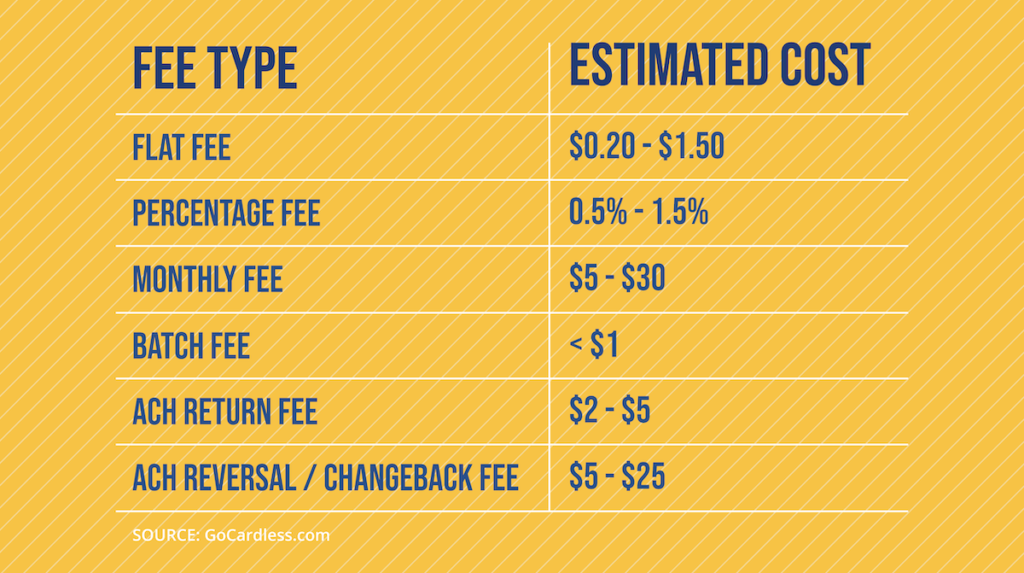

Credit cards generally carry a fee around 2.5% of the value of the transaction, and they have a flat-rate processing fee. ACH transactions usually cost between $.20 – $1.50. How many transactions are you processing every month and for what amounts? The savings ACH provide can accumulate rather quickly.

3. Works well long distance

ACH can be used to transfer money internationally, which can shave days (or even weeks) off of a payment timeline if using a physical check. While there is no global ACH system, many countries have their own systems that will interface with ACH. For example, in Europe, the equivalent system is called SEPA (Single Euro Payments Area) and in Australia, they use “Direct Entry.”

4. Ease of tracking

Since the bank is directly attached to the electronic funds transfer, the accounting is much easier to sync up—there’s no need to update two different records manually the same way that you would ‘balance a checkbook.’ Many accounting tools and software services can integrate with the ACH system to provide you with detailed transaction history.

How do ACH Transactions work?

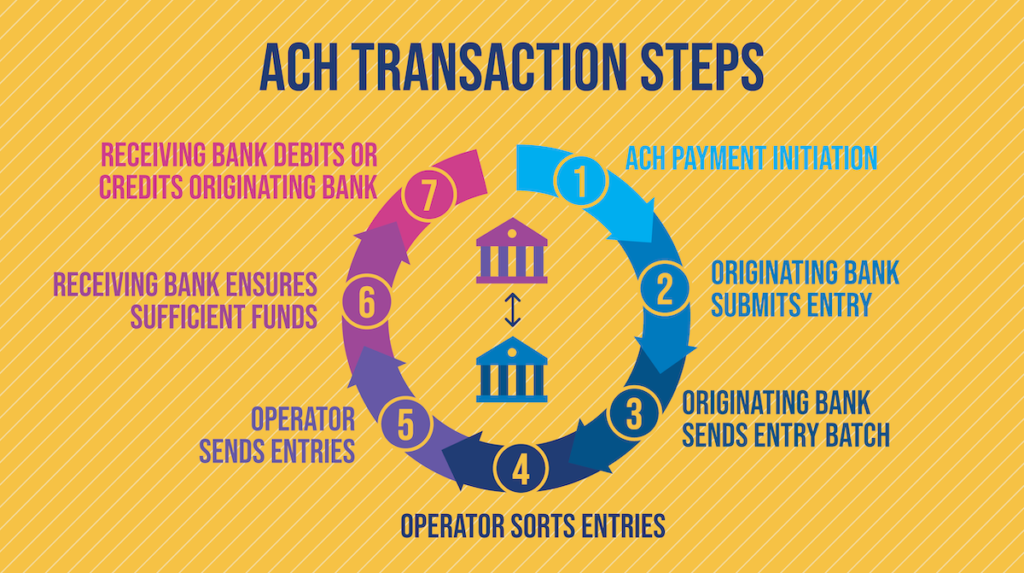

The entire ACH process is a pretty straightforward seven-step process:

1. Originator initiates the ACH payment

It all starts when the originator (bank, company, or individual) begins the transaction. This applies to both ACH debits and credits.

2. Originating bank submits ACH entries

The financial institution or payment processor of the originator (called an “Originating Depository Financial Institution) submits the ACH entry.

3. Originating bank sends ACH entries in batches to network operators

Next, the Originating Depository Financial Institution sends their batches of entries to an ACH operator such as the Reserve Banks or Electronic Payments Network (EPN).

4. Network operator sorts entries

The operator then sifts through the batches of entries and determines if they are deposits or payments.

5. Network operator sends entries to recipient bank

Once that fact has been established, the operator then sends them to the respective Receiving Depository Financial Institutions (RDFI).

6. Receiving bank ensures sufficient funds

Depending on if the transaction is a credit and involves the removal of funds, the receiving bank needs to make sure that there is sufficient funding available in the ODFI.

7. Receiving bank credits or debits originating bank account

Lastly, it depends on whether the transaction is a deposit or a payment, but the RDFI will debit or credit the receiving account.

Perhaps it’s not the most exciting process, but it works. If at this point you’re thinking, “Hey, this all sounds pretty good, but how do we implement ACH?” keep reading!

How to Set up ACH Payment Processing

Before we get into the details of how to set up ACH payments for your organization, there are a few rules you need to know.

- Account info verification – You’ll need to regularly check to ensure your account info is up to date with ACH. To do this, you can send micro-deposits (usually .01¢ – .50¢) to another bank account, which when they acknowledge receipt, confirms that your account is properly connected and funded. These deposits will be returned to you. You can use a tool provided by NACHA or a third-party validation tool.

- NACHA certification – This is a trust signal to your customers that your business is operating within the governance of the ACH network. More info on the NACHA website. Note—this certification is for third-party operators who handle the transactions, not your organization, but it’s good to choose an operator with this certification.

- Rules for same-day ACH – Due to the growing popularity of ACH, there is now an option for same-day payments. This allows receivers to get access to their funds at 1PM local time, just so long as the payment was processed in that morning.

Got it? Good; here’s a step-by-step guide on how to set up ACH payment processing.

Step 1 – Choosing an ACH merchant

First off, call your bank to see if they themselves are a merchant provider—many banks are. If not, your best course of action is to review a list of ACH merchant providers and examine their service offerings. A few things you’ll want to look out for:

- Transaction fees and structure

- Support offered (live, same-day, etc.)

- Software and automation

- NACHA certification

- Security

Don’t be shy about interviewing several merchant providers and making sure that their service offerings fit your needs such as invoice processing, employee payments, etc.

Step 2 – ACH onboarding

Once you’ve selected a merchant, it’s time to get up and running through what’s generally referred to as the corporate enrollment process. It varies depending on which vendor you use, but the process usually consists of the following:

- Instructions for entering vendor account info

- Instructions for initiating transactions,

- Instructions for setting up recurring transactions

- Instructions for bringings payments and remittance in the same place to optimize vendor payments

This process is unique to each ACH operator.

Step 3 – Acquire permission

In order to actually transfer money with ACH, you’ll need to acquire permission from both parties. It’s best to obtain this permission digitally because if there is ever a dispute about a charge, it’s easy to look up that data. Always check to make sure the vendor’s account info is accurate, as well as your own info, to make sure you don’t deposit money into someone else’s account due to a typo.

Step 4 – Using the operators portal

Once you’re in, explore your operator’s portal for functionality. Again, these capabilities are unique to each operator, but here are a few common things you should be able to execute:

- View payment statuses in advance

- View rejected payments

- Re-issue payments

- View reports and charts of your payments

Step 5 – Start making payments

Now that you’re all set up, it’s time to start making payments and enjoying the benefits of ACH! Lower transaction fees, more convenient (and faster) payments, and superior tracking and accounting.

So what do you think—are ACH payments right for your organization?

If you have any questions about this article, or how ACH payments can work with your existing accounts payable processes, feel free to chat with one of our AP Heroes!

ACH Payment FAQs

Automated Clearing House or ACH payments are US-based bank-to-bank transfers which are processed through the ACH network run by NACHA. ACH payments are also referred to as direct payments and are commonly used for business-to-business transactions, in addition to employee direct deposits.

ACH payments are common for both consumers and businesses. Consumers use ACH payments to pay bills online, mortgage payments, and other types of loan repayments. Businesses use ACH payments to pay both their employees by ACH direct deposit and pay their vendors or suppliers.

ACH payments can be reversed by your bank which often comes with chargeback or ACH return fees. There are only a few circumstance where ACH payments can be reversed such as: payment was issued in the wrong dollar amount, the payment was a duplicate, or the receiving account information is incorrect.

ACH debit payments are pull payments and are typically used by consumers to pay bills such as monthly utilities. By entering their bank, account and routing number, consumers can have their bank account withdraw or pull funds via debit to issue the ACH payment.

ACH credit payments are push payments and are often used by businesses to pay their employees and vendors or suppliers. This requires the payer to initiate the ACH payment and have the funds pushed into the receiving bank account.

ACH payments are considered to be secure. An ACH payment is processed through the highly regulated and monitored network called NACHA, and the information exchanged during the transaction is encrypted to mitigate any unauthorized access.

ACH Payments vs. Wire Transfers

ACH Payments vs. Paper Checks: When to Use Each