ACH Payments vs. Paper Checks: When to Use Each

It’s no secret that, in recent years, paper checks have been steadily declining in popularity in the B2B payments space.

An Association for Financial Professionals study found in September 2019 that, for the first time, fewer than half of all B2B payments were made by check. Numbers for 2020 aren’t available yet, though it’s conceivable that the COVID-19 pandemic, which spurred a sharp rise in remote working, has led to even fewer paper checks and more electronic payments through methods like the automated clearing house, or ACH.

That said, there will still be times where businesses might need to opt for paper checks over using ACH payments. Join us as we explore what ACH payments and paper checks are in B2B terms, how they’re used optimally in this environment, and how the two payment types compare head-to-head.

B2B Payment Option No. 1: ACH

First created in the 1960s in the United Kingdom and brought to the U.S. a few years later, ACH payments are a form of electronic funds transfer (EFT), using a virtual waystation known as the automated clearing house to allow funds to move from one account to another.

The ACH is not technically a brick-and-mortar place, though it processes around as many total payments in a day as the number of passengers for all of 2019 at the world’s busiest airport (110.5 million at Hartsfield-Jackson in Atlanta for anyone curious). Even just looking at businesses, there were just shy of 11 million B2B payments with the ACH each day in 2019.

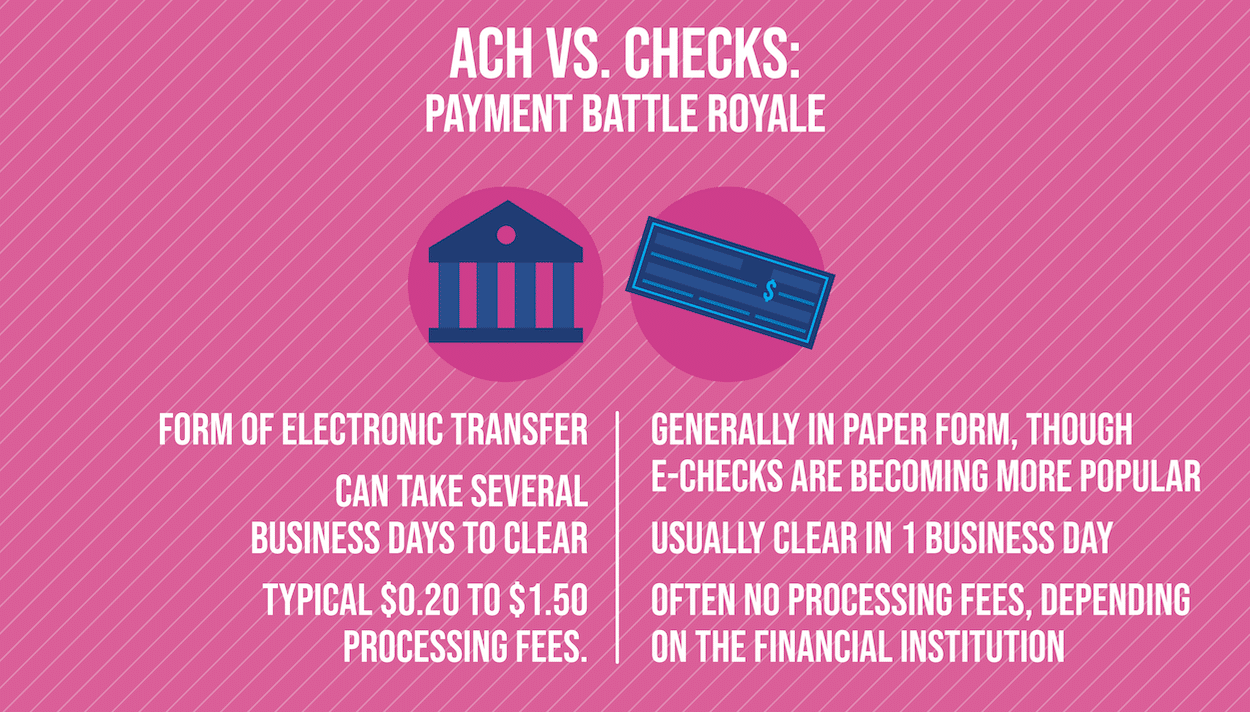

People and businesses often make frequent use of the ACH likely because it’s secure, affordable, and relatively quick, at least quicker than waiting on a mailed check. More than 90% of workers receive their paychecks via the ACH, since it’s generally how direct deposit travels. The ACH also works well for B2B payments, since its standard fees of $0.20 to $1.50 per transaction are a fraction of the average 1.3% to 3.4% credit card processing fees.

Growing Popularity of ACH

Over 100 million times a day, and the number’s still growing, people or businesses make use of the ACH Network.

“The first quarter results show that the ACH Network is poised for another year of sustained growth,” Jane Larimer, Chief Operating Officer for the National Automated Clearing House Association, or NACHA, which governs the network, said in a May 6, 2019 press release, not long after the network broke 100 million daily payments for the first time.

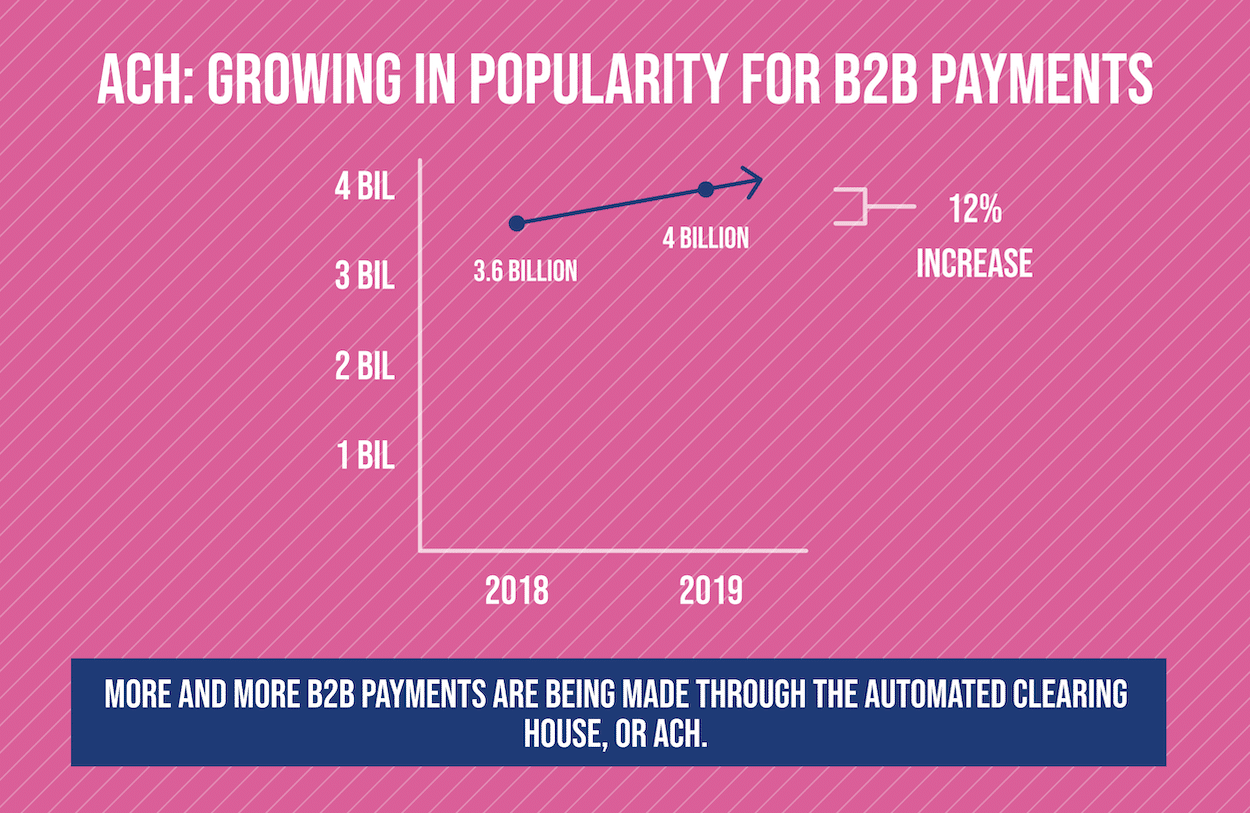

The network would go on to move 24.7 billion payments valued at close to $56 trillion in all in 2019, PaymentsJournal noted in November. Of these, around 4 billion were B2B, representing a 12% growth. Even with the pandemic, volume grew in 2020, with 6.6 billion total ACH payments in the second quarter, a 7.9% increase from the same quarter in 2019.

According to an AFP study, “this year’s survey results… suggest companies in the U.S. are more amenable to shifting their payment methods away from checks to electronic alternatives,” the report noted. “One reason for this could be the vast array of new solutions and providers whose offerings are more compelling than checks.”

When to Use the ACH for B2B Payments

ACH payments can take several (3-5) business days. Thus, they’re best deployed by businesses when they can either be planned well in advance (as is typical with doing payroll) or with vendors or contractors who don’t need their funds immediately once a business deal is agreed upon.

Due to the affordability of ACH transfer fees, businesses also have some negotiating power when looking to make B2B payments with them. They can offer a 2% to 3% discount, since it’s what credit card companies would be charging them anyway. Or they can offer to increase future orders with suppliers using the money they’re saving.

Additionally, ACH payments are great in terms of security, since they’re reversible, unlike wire transfers and can’t be washed and forged, unlike stolen checks.

B2B Payment Option No. 2: Paper Checks

Sometimes, though, ACH isn’t going to cut it, and a business may want to look to a paper check to get a B2B payment out.

In some cases, it’s a matter of certain old school vendors and contractors preferring to receive a physical check in the mail or pick one up in person at a business, as opposed to providing their banking information to it for an ACH payment. There are other times that paying by check might be the right tactical decision for a business.

Here’s a look at the relevancy of paper checks for businesses.

Paper Checks: Tried, True, and Still Common in B2B

Business checks in the United States go back to the late 17th century and the first printed checks were used by a British banker in 1762.

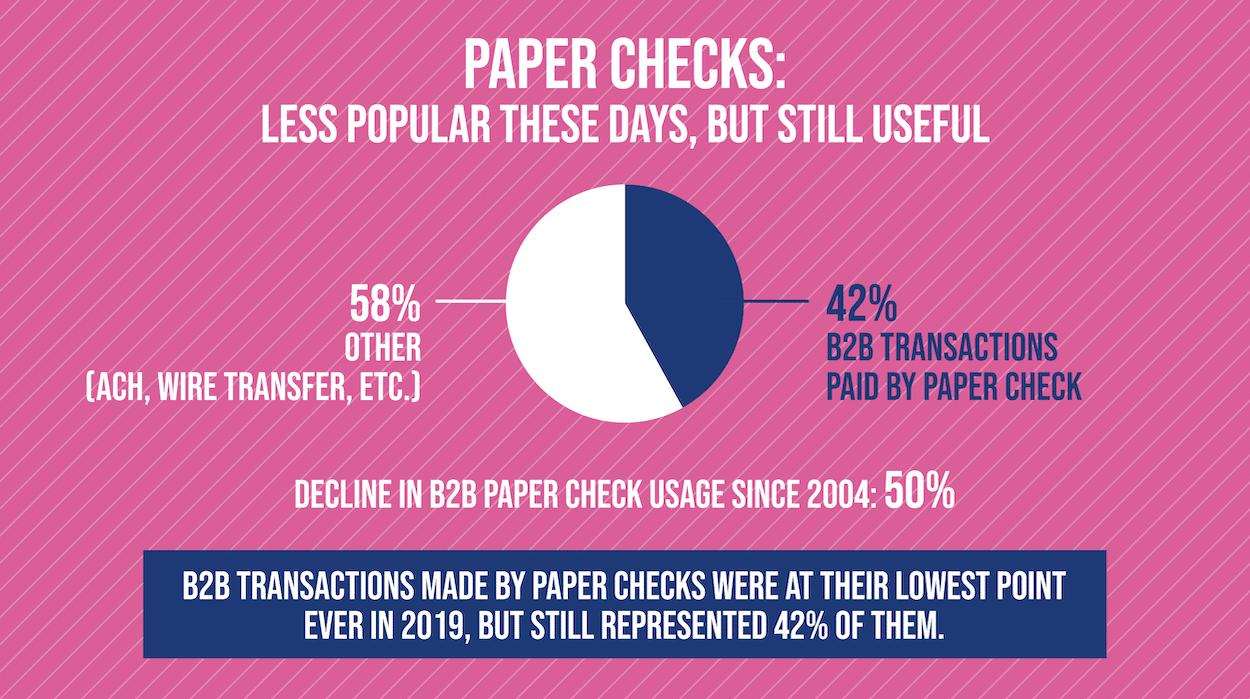

The ease of ACH as well as the rise of the internet, smartphones, and a paperless society have all cut into the ubiquity of paper checks in business in recent decades. But checks still remain widely used in the B2B world. While AFP noted when discussing the results of its 2019 survey that B2B check usage had fallen to an “all-time low” and were down nearly 50% overall since 2004, they nevertheless represented 42% of B2B transactions.

Just over 80% of businesses were using paper checks to pay invoices as of 2019, with 51.8% satisfied with them, PYMNTS noted in its Payables Friction Index.

“Even though checks are slower to process than electronic payment methods and are more susceptible to fraud, they continue to dominate B2B transactions, signaling the challenge in changing internal processes,” AFP noted about its study. “Other barriers treasury departments face in moving away from checks are a lack of IT resources, and difficulty convincing business partners to shift towards sending/receiving e-payments.”

Among other benefits, paper checks can be printed on a business’s premises, and are reversible in the event of a fraudulent or cancelled payment. Paper checks can also be painless with systems like Stampli Direct Pay, an optional service to invoice processing which helps AP finish the last leg of accounts payable; payments. Stampli Direct Pay does this by ACH, check and customers can even pay outside the system for maximum flexibility. How checks work with Stampli Direct Pay is the system automatically prints and mails physical checks from your bank account and uses your own signature. And they provide an easy record for tax purposes, with images of cleared checks automatically recorded in online dashboards.

When to Use Paper Checks for B2B Payments

Generally, businesses will want to opt for paper checks for B2B transactions when the ACH is either infeasible or the vendor or contractor they’re working with indicates that they’d prefer a paper check. There can also be hoops to jump through for international ACH payments, as NACHA noted.

Sometimes as well, people just prefer a check. Some of it can have to do with personal taste. Six percent of Americans also still lack broadband internet, which is helpful for accessing ACH payments. Five percent of U.S. households also lack a bank account, which is necessary for an ACH payment to be deposited in, while checks can always be taken to a check-cashing service.

How ACH and Checks Compare

Here’s how ACH payments and paper checks stack up when placed head to head.

Similarities

Similarities between the two types of payment include:

- Both ACH payments and paper checks are fairly low-cost to issue, with ACH fees generally topping out around $1.50 per transaction and paper checks costing slightly more due to postage, though there are staffing costs to consider. Checks can also have hidden expenses, such as stop payment orders or returned check fees.

- Each of these payment types can be reversible, unlike other types of payment in certain instances such as wire transfers or cash transactions.

Differentiators

There are also at least a few differences between the ACH and paper checks. Differences to note include:

- Paper checks are of course a physical document, though electronic or e-checks are becoming more popular. ACH payments are strictly digital.

- Depending on the financial institution, most checks clear within one business day. ACH payments, on the other hand, can take several (3-5) business days to clear, but one has to consider the time it takes for the check to travel to its destination by mail.

- Paper checks present certain longstanding security concerns, such as check washing, which has existed since at least the mid-1980s and costs consumers and financial institutions over $800 million a year. The Guardian noted recently that the best defense against check washing could be simply not using checks.

So Which is Better?

At the end of the day, it’s not so much about either paper checks or ACH payments being better than the other. It’s about which payment option works best in a given situation. And as any veteran corporate leader might know, every situation is different in business.

It’s up to them to make their assessment and then determine if the ACH or a check works better.

No matter which payment type you prefer, Stampli has you covered. Stampli Direct Pay offers users the ability to send payment by check, ACH or even outside of the system. Learn more about Stampli Direct Pay here.