ACH Payments vs. Wire Transfers

When businesses go to pay their vendor bills these days, it’s safe to say they have a lot of options for business-to-business (B2B) payments. Aside from cutting a check in or paying by cash, companies also have innumerable electronic payment methods to fit their current accounts payable payment processes.

Here, we’ll explore two payment methods:

- The increasingly-popular automated clearing house, or ACH commonly used for B2B payments.

- Wire transfers, also known as “large-value systems.”

There isn’t necessarily a right or wrong method when it comes to parsing ACH vs. wire transfer payments, though a keen understanding of them can help guide when businesses should use each of them.

ACH Transfer Uses

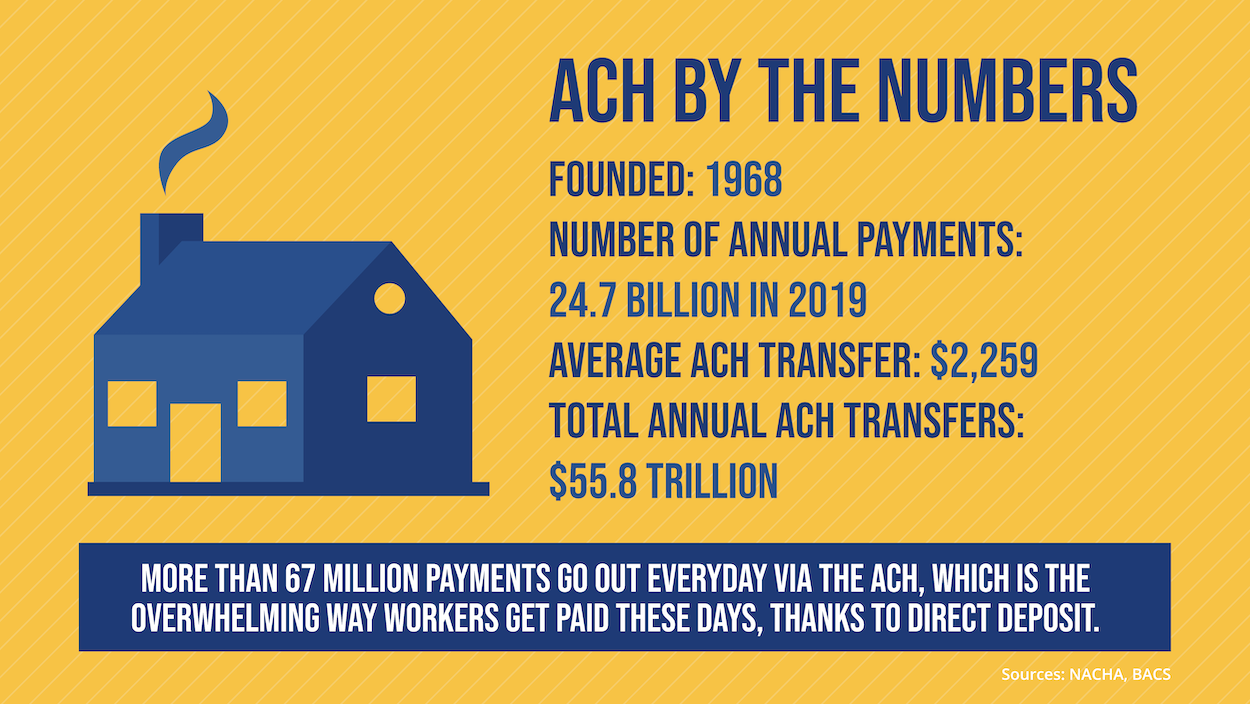

Many American workers might recognize ACH because the symbol can show up on their bank statement anytime they receive a paycheck direct deposit, which has become the preferred means of payment for more than 90 percent of employees.

That said, the ACH — which was first operated by BACS in the United Kingdom in 1968 and brought to the U.S. via the Federal Reserve Bank of San Francisco in 1972 — has a number of other applications aside from direct deposits, including:

Streamlined ACH Preparation

When ACH payments are prepared in an invoice processing system, accounts payable gains easy access to relevant details, invoice history, and supporting documents for seamless payment approvals.

ACH Payment Approvals & Controls

ACH payments provide businesses with control for how and when they pay their vendors. By establishing segregation of duties for payment processors and approvers, businesses can set up payment approval workflows. These workflows are typically based on payment amount thresholds, where approvers can easily make a decision to either approve or reject the payment.

When ACH payments are approved, they are either assigned to the second approver depending on the workflow, otherwise, sent to an outbox tab where the payment will be paid dependant on the scheduled date.

When an ACH payment is rejected, a payment processor will either cancel the payment and create a new payment or else re-submit for approval with the correct payment information. The payment approval process helps businesses deliver accountability and complete control over their payment processes as every action is recorded for audit later.

Batch ACH Processing & Reconciliations

Need to send out payment en masse to a number of vendors? ACH payment processing can be great for allowing large numbers of payments to be scheduled in bulk. Payments systems like Stampli Direct Pay enable payments to be withdrawn on a transaction-by-transaction basis rather than a single lump sum withdrawal, which in turn makes reconciliations easy.

This can be particularly useful for companies that process multiple invoices for the same vendor month over month, slashing time and expenses associated with all of the previous individual payment preparations. Not to mention the time saved when it comes to reconciliations, as transactions will be individually listed on banks statements when processing batch ACH payments.

Vendor ACH Payment Details

Vendor Portals are available for vendors to view the status of their invoices and to send any invoice questions to you directly. These portals save time for both accounts payable and your vendors as they come in with built-in self service options which will cut down on the number of vendor inquiries regarding ACH payment status. Moreover, you can ask your vendors to enter their ACH payment details directly in the portal, with a final confirmation required by accounts payable to ensure complete control over payment details.

Wire Transfer Uses

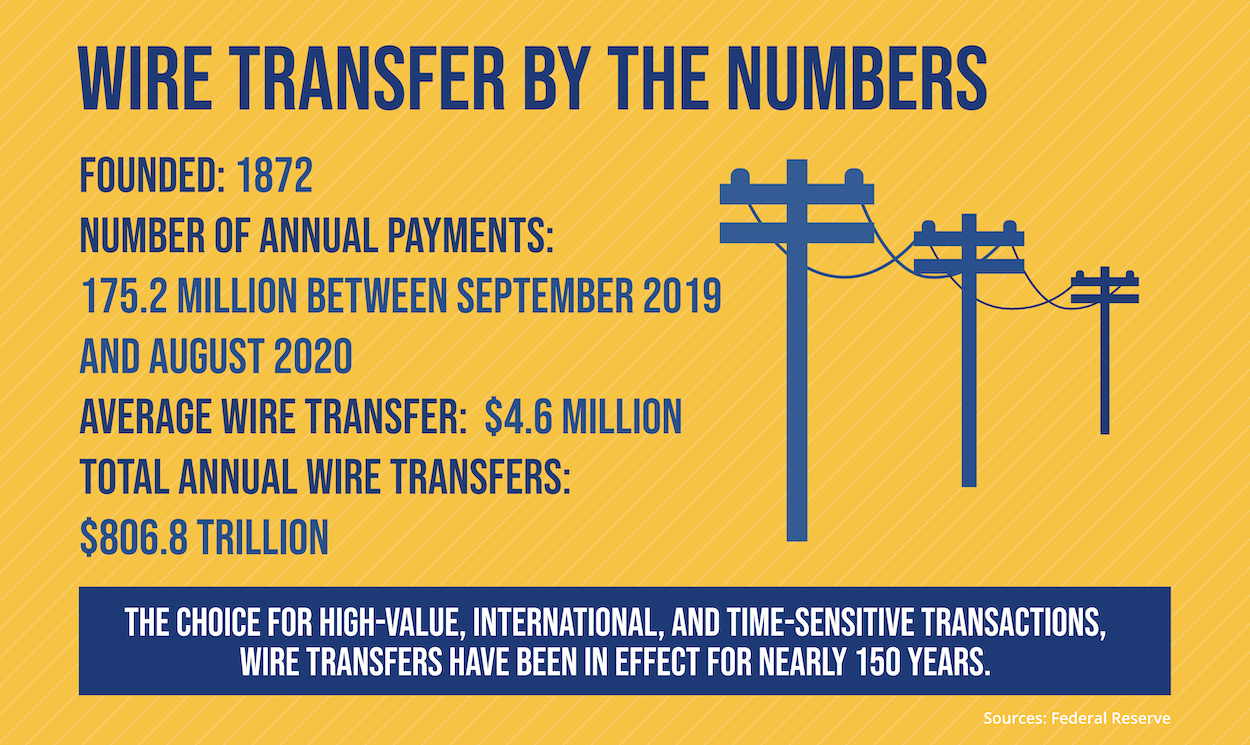

First operated by Western Union in 1872, wire transfers are a less frequent transaction in comparison to ACH payments, with 175.2 million wire transfers between September 2019 and August 2020. According to Fedwire, one of two services send wire transfers, along with the Clearing House Interbank Payments System (or CHIPs). This was as opposed to 24.7 billion transfers with the ACH Network in 2019, the most recent year statistics are available through the National Automated Clearing House Association.

All the same, while not as ubiquitous as ACH these days, wire transfers have at least a few common uses and can be a great means of payment in the right situations. The trick is to know when wire transfers are needed, that is, if a vendor doesn’t indicate a preference.

High-Value Transfers

When wire transfers are issued, they tend to be for a significantly higher dollar value than ACH payments. The average wire transfer between September 2019 and August 2020 was about $4.6 million, according to Fedwire, as opposed to approximately $2,259 for each ACH payment, per NACHA.

If there’s a fundamental difference between ACH vs. wire transfer payments, it might lie therein. Think of it this way: When a worker receives their paycheck, it’s more than likely coming through the ACH network, and the same goes for paying a vendor for goods or services. But when a company is acquired by a multinational megacorporation, that money is probably being sent via a wire transfer.

There are just orders of magnitude in difference between the two different scenarios.

International Payments

More business has been happening internationally in recent decades. And in dealing with out-of-country vendors and contractors, the automated clearing house isn’t always the best option for payment as the ACH network is a U.S. based bank-to-bank infrastructure which runs into complications when borders are crossed.

The reason for this: While it’s possible to use the ACH to send international money transfers, according to the Consumer Financial Protection Bureau, other sources note that the process can be somewhat protracted, involving several steps, due to the setup of the U.S. ACH network. Wire transfers can offer more straightforward international payment options.

Time-Sensitive Payments

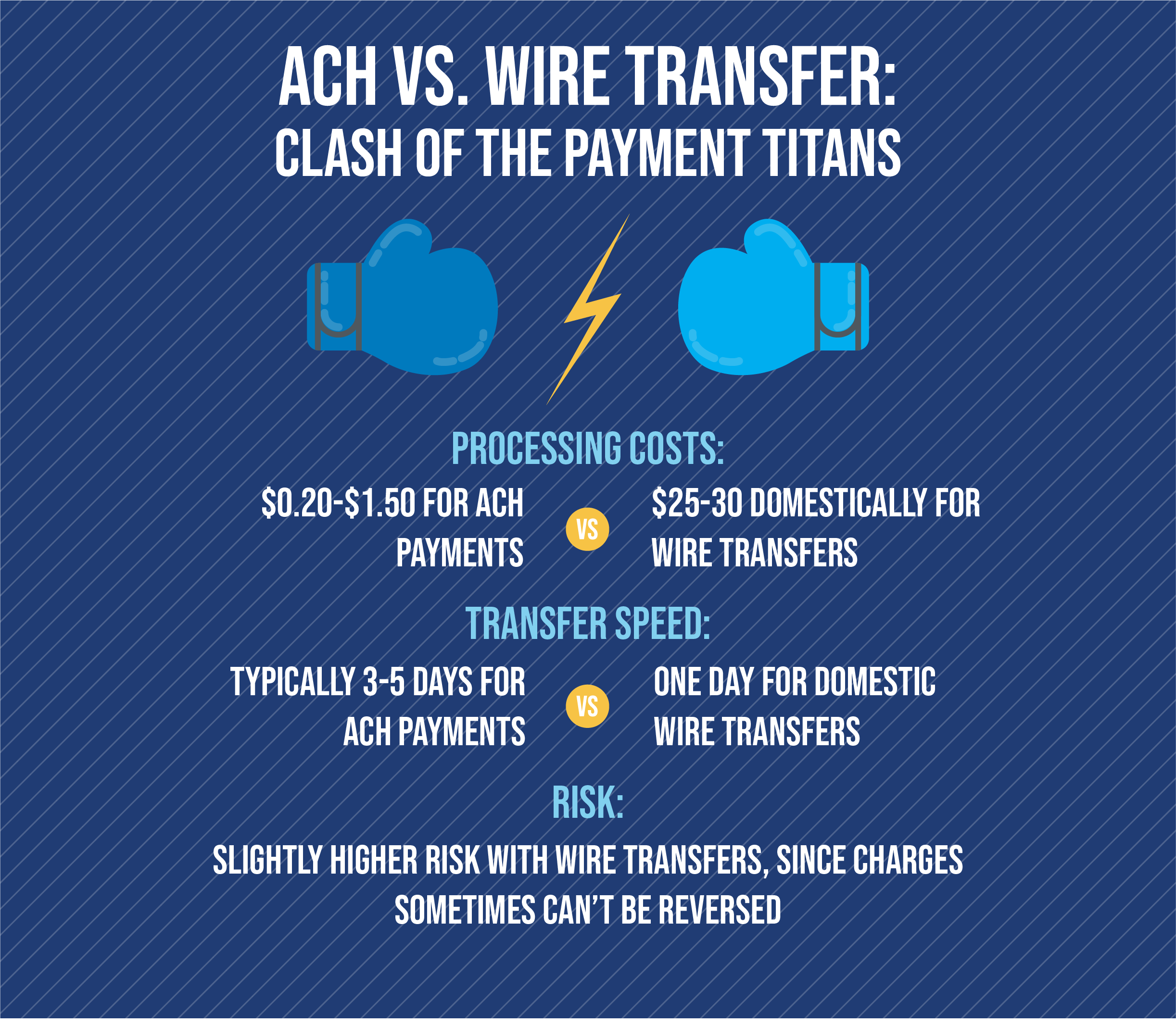

ACH payments are cheaper for processing payments and range from $0.20 to $1.50 per ACH transaction. On the other hand, ACH payments will take 3-5 business days before the receiving party will have the funds available in their bank account. At the same time for ACH payments, funds will be withdrawn from the sender’s bank on the same business day the payment was executed.

In comparison, wire transfers debit the sender’s account and credit the receiving bank account in real time. While wire transfer costs range from $25 to $50 depending on the relationship and type of transfer, it could be worthwhile to pay by wire transfer if late payment fees exceed the cost of the wire transfer, or to simply remain in good standing with suppliers.

Head-to-Head: How ACH Payments and Wire Transfers Compare

Here are some things to consider when choosing between ACH vs. wire transfer payments.

Processing Costs

Wire transfers come with the assurance that a lot of money can generally make it where it needs to go fairly quickly, though this service isn’t cheap.

Business Insider noted in July 2020 that wire transfers usually cost “between $25 and $30 for outgoing transfers to a bank account within the US, and between $45 and $50 for transfers going out of the US” with additional fees to receive the money of roughly $15. For this reason, even accounts payable departments willing to accept wire transfer fees on their end should always check with their vendor if they’re okay with them, or offer to cover them.

ACH transfers, on the other hand, come with a fraction of the costs, generally $0.20 to $1.50 per transaction, according to Merchant Maverick. The lower cost points typically are from a bank, while the higher ranges are where ACH transfers are typically performed by a service.

“If you don’t need the money immediately, an ACH transfer could be an easy and free way to send money,” Business Insider wrote. “An ACH transfer can often take several days, but these transfers generally don’t require fees.”

Winner: ACH

Speed

As noted earlier, wire transfers can be instantaneous, or at least within one business day domestically, while ACH payments usually take 3-5 business days. Granted, they can be scheduled to arrive in a person’s account on a certain day, though a company will need to get the ACH payment initiated a few days before to ensure it clears when it’s supposed to.

Thus, in instances where companies aren’t able to plan ahead and just need to send a lot of money somewhere very fast, wire transfers can win the day. But in the long run, victory loves preparation and saving money now has compounding value down the road.

Winner: Wire Transfer

International Wire & ACH Transfers

ACH transactions are common in the United States, which are governed by NACHA , formerly called the National Automated Clearing House Association. In short, NACHA is the backbone of the ACH network. In order to abide by international rules for cross-border payments, International ACH Transactions (IATs) are now regulated and is the regulatory format for all ACH payments entering or exiting the United States.

Due to IAT requirements, it can sometimes be hard to make international ACH transfers. Although international ACH transfers are possible, the best option is usually to simply go with an internal wire transfer due to the simplicity and speed at which money can be moved cross-border.

Winner: Wire Transfer

B2B Payments

Wire transfers are designed to handle high-value transactions, most often between financial institutions. While on occasion businesses outside of the finance space will make wire transfers, most make their vendor payments by means of ACH transfers. This is in part due to the ease of use given ACH is more automated than wire transfers, in addition to the lower costs on a per transaction basis.

Winner: ACH

Security

While fraud can strike business users of both the ACH and wire transfers, the risk might be a little more pronounced with the latter. The U.S. Federal Trade Commission warned that money transfers are essentially the same as cash in that they can’t be reversed. On the other hand, ACH transactions are reversible, whether because of an error made in payment or outright fraud.

Winner: ACH

Recap: Choosing Between ACH Payments and Wire Transfers

When choosing an electronic payment method such as ACH or wire transfers, companies don’t just have to opt for one or the other. For smaller payments, the ACH is a cheap, secure, and reliable means of payments. But for larger or international payments, or ones that need to be done quickly, wire transfers can be superior.

It’s all about knowing the situation and then opting for the right kind of payment for it. But if things still seem foggy, AP automation solution providers are available to help.

With Stampli Direct Pay, you have the freedom to pay your way by ACH, pain free checks, or outside the system.