How to Choose the Right Mix of Electronic Payments

It’s time for you to improve your working capital management by taking control of how your business makes electronic payments.

Today, business owners can choose from a huge variety of payment methods. Choosing the right ones can lower processing costs, improve payment efficiency, and build good vendor relationships.

However, there are pros and cons for each electronic payment type. Choosing the payment options that best suit your business can be tricky.

Read on to learn about the different types of electronic payments, their pros and cons, and what you can do to optimize your payments mix.

Let’s start by explaining what electronic payments are.

What is an electronic payment?

Electronic payments are fast becoming the norm for vendor payments.

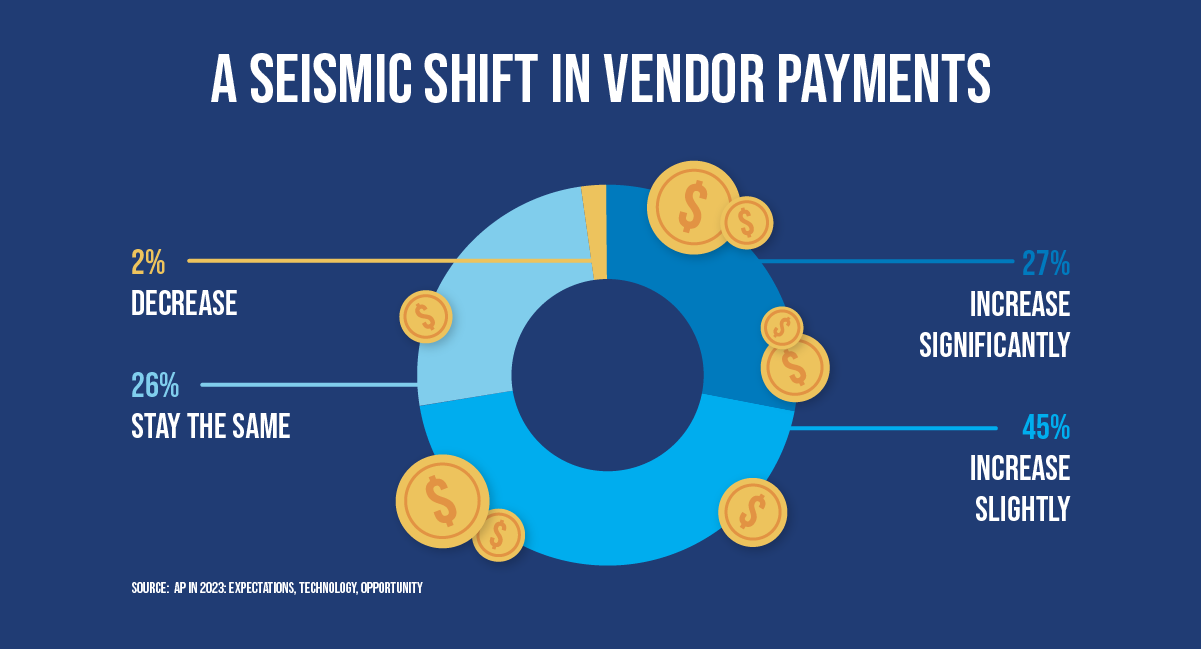

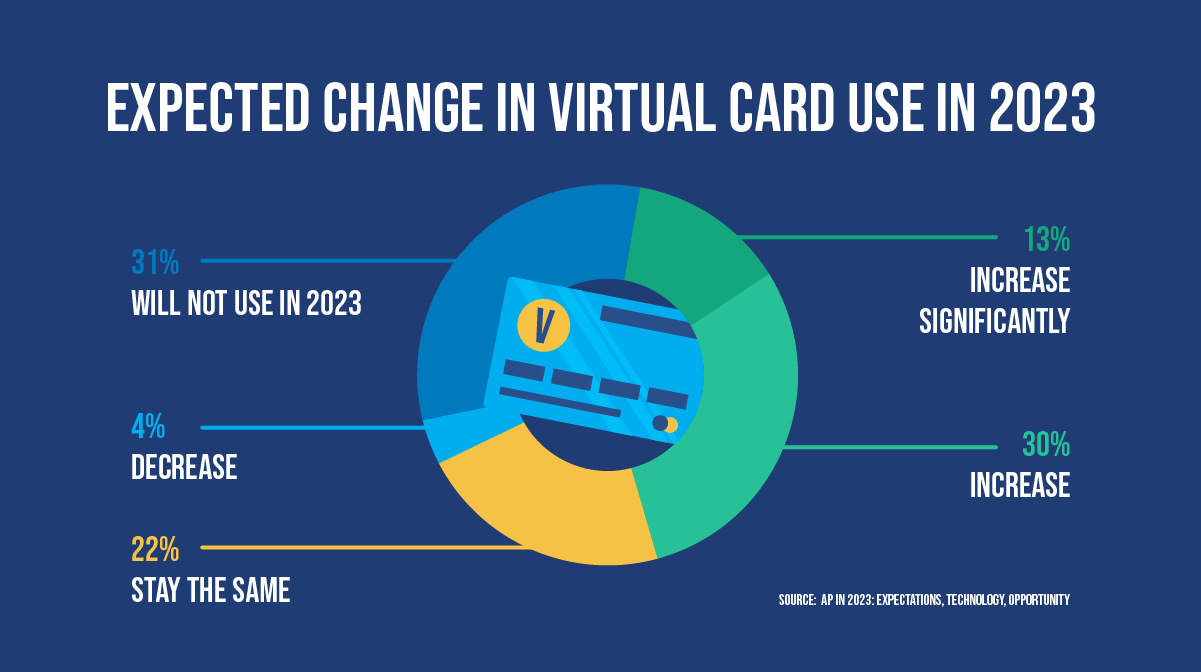

In 2022, Stampli surveyed 251 financial leaders across the US about their expectations for 2023. Almost three-quarters (72%) reported they expected to increase their use of digital payments to pay suppliers.

In a nutshell, an electronic payment (e-payment or digital payment) is any payment completed over a digital network. Every electronic transaction begins with a sender and receiver. The sender initiates an electronic funds transfer (EFT) with a payment services provider, such as a bank. The payment service provider transmits the payment information to the receiver’s financial institution, and the funds are transferred from the sender to the receiver.

The type of electronic payment depends on how the EFT is processed. For example, wire transfers are processed over member-based banking payments networks. Credit card payments are completed over private networks owned by the credit card provider.

Electronic payments are fast and secure and promise significant benefits to your business. However, they also come with some risks that you must be aware of.

Let’s take a look at both, starting with the benefits.

Advantages of electronic payments

Here are the key benefits of using electronic payments in your business.

Convenience and efficiency

Electronic payments are faster and easier to use than paper checks. For starters, you don’t need to print, sign, and mail a stack of paper checks every week. Payment by check can take over a week, while electronic payments can usually be completed within one to two business days.

Better vendor relationships

You can pay vendors faster with electronic payments. Paying faster lets you avoid late payment and negotiate early payment discounts with vendors. Many payment platforms also provide a vendor portal. The vendor portal allows vendors to check on their payment status.

Lower processing costs

Check processing is labor intensive and requires ink, paper, printing, and postage. Electronic payments are labor efficient. Usually the only cost is the transfer fee.

Some credit and virtual cards also offer rebates on purchases. These rebates can offset the costs of payment processing and even earn a profit.

Better transaction security

Electronic payments are significantly more secure than paying by check. Electronic transfers are encrypted to prevent fraudsters from accessing critical data. Some credit and virtual cards use tokenization security to protect credit card information during transactions.

Digital payment solutions also automatically track and record transactions, ensuring a complete audit trail. Tracking makes it easier to detect and control fraud and errors more easily.

Finally, in the US, EFTs are also protected under the Electronic Fund Transfer Act (EFTA), which provides additional protection from fraud.

Improved visibility into transactions

Electronic payments make it easier to track transactions and manage your cash flow. Because each transaction is recorded, you can closely monitor what you’ve spent. This improved visibility makes it easier to make informed decisions about payments.

Risks of EFT transfers

Although electronic payments have many benefits, they also come with unique risks. Assess these risks carefully when you’re considering payment types.

Vulnerability to fraud

Electronic payments are vulnerable to payment fraud. For example, internal fraudsters can alter payment batch files or invoices to defraud their employer. Internal and external fraudsters can also process fake or duplicate payments, steal and duplicate credit card information, or intercept and redirect wire transfers. Ensure you understand the fraud risks associated with the payment methods you’re considering.

Difficult to reverse payments

It can be difficult to reverse a wire transfer or other digital payment in case of an error. Make sure you understand the process to stop or reverse a transaction with each payment type.

Inefficient manual processing

Tracking and processing invoices with a spreadsheet and paying vendors manually via a bank gateway or credit card is inefficient and error prone. It’s also difficult to enforce internal controls and separation of duties when relying on manual workflows. As a result, your business could be exposed to risks like wire fraud or human error.

By carefully considering these benefits and risks, you can better understand the right payment mix for your business.

Now, let’s look at the different electronic payment methods.

Types of electronic payment

The list of electronic payment types is always growing as payment providers continue to innovate. Here are the most common types of digital payments today:

- Wire transfers

- ACH transfer

- Credit cards

- Virtual cards/Ghost cards

- Payment cards

- Debit cards

- Digital wallets and peer-to-peer payments

- International payments

Let’s dive into the details.

Wire transfers

Wire transfers are the oldest form of digital payment. They are real-time payments where cash is electronically transferred from one bank account to another.

Pros

- Very fast: many wire transfers are completed within the same day

- Secure: wire transfers require confirmation of funds before the transfer is sent

- Large value transfers: wire transfers are good for large transactions

Cons

- Expensive: fees for wire transfer are usually higher than other electronic transfers

- Vulnerable to fraud: Wire fraud is common, especially for high-value transactions

ACH transfers

ACH (automated clearing house) transfers are electronic payments made over the ACH Network, an electronic payment system that reaches all US banks and credit unions. ACH transfers are an alternative to wire transfers for payments within the USA.

There are two types of ACH transfers:

- ACH Debit “pull” transfers are requests to “pull” funds from an account the payee doesn’t control. For example, pull transactions are commonly used for automatic monthly payments such as utility bills.

- ACH Credit “push” transfers are requests to “push” money from the payer’s account to the payee’s account. Credit transactions are most commonly used for electronic checks, vendor payments, and direct deposit.

Pros

- Inexpensive: ACH transfers are generally less expensive than wire transfers

- Secure: The ACH network is closely regulated, and transactions can be stopped or reversed

- Batch transfers: ACH transfers can be processed in batches to make it easier to pay multiple vendors or invoices

Cons

- Slower: ACH transfers are slower than wire transfers and can take 1-3 business days

- Vulnerability: ACH transfers involve sharing bank account numbers, which raises the risk of fraud

- Reconciliation: ACH transaction data isn’t automatically transferred from your bank, which can make it hard to reconcile invoices

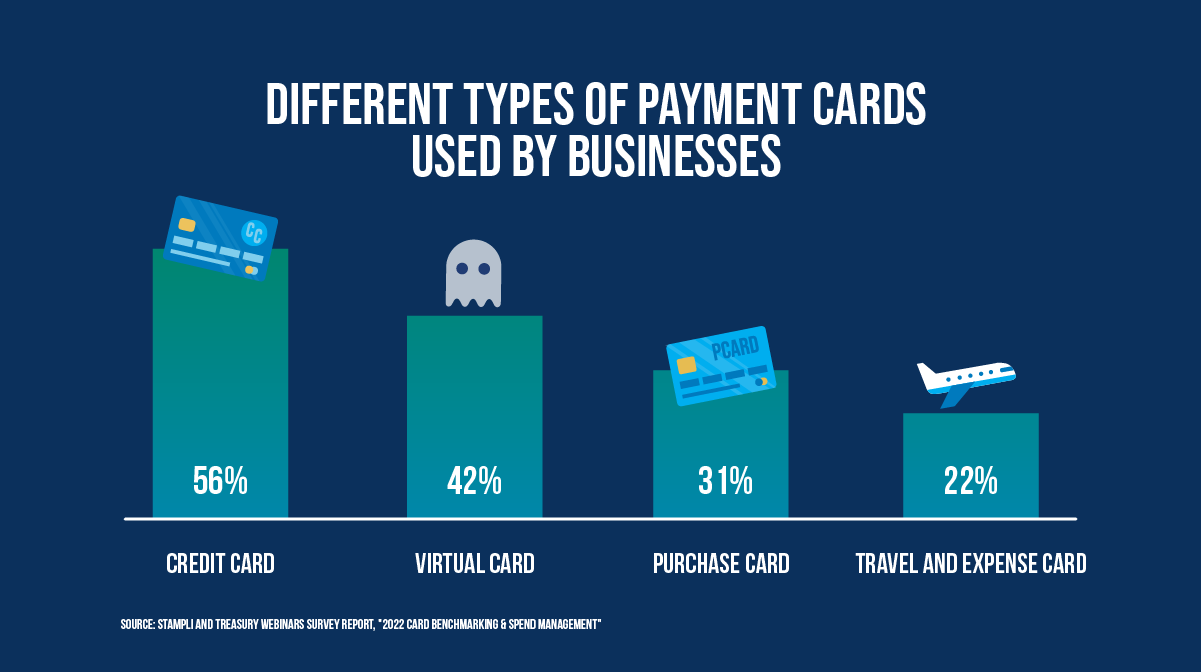

Credit cards

Credit cards allow payers to borrow money from the card issuer to make payments. Credit card processing is managed through private financial networks owned by card companies like Visa or MasterCard.

Pros

- Instant payment: Credit card payments let you pay vendors instantly to avoid late payments

- Reversible: Credit card transactions may be reversed more easily than wire transfers or ACH transfers

- Tracking payments: You can easily track payments via the credit statement or online portal

Cons

- Vendor fees: Some vendors refuse to accept credit card payments because they charge high vendor fees

- Vulnerable to fraud: Physical credit cards can be duplicated and used for fraudulent purchases

Virtual Cards/Ghost Cards

Virtual or “ghost” cards are credit cards without a physical card. Companies can assign individual virtual cards with unique card numbers, specified users and spend categories, and payment limits.

Unlike physical credit cards, virtual cards are very difficult to duplicate, which makes them less susceptible to fraud. If a card number is stolen or the company suspects a card may be used fraudulently, the card can easily be canceled and a new card issued.

Debit card

Debit cards are commonly used to make point-of-sale purchases. Instead of charging purchases to the cardholder’s credit line, the payment amount is funded directly from the cardholder’s bank account to the merchant account.

Pros

- Vendors are provided with certainty of payment and pay slightly lower transaction fees

Cons

- Debit cards can be stolen or duplicated and used for fraudulent transactions

Payment cards or Pcards

Payment cards and commercial cards are issued to employees to pay for purchases directly from a corporate line of credit. They are typically used for T&E expenses but can also be used for recurring and vendor purchases. Payment cards can be restricted to a specific cardholder or purchase category and usually include spending limits.

Pros

- Payment cards are easy to use and secure

- Employee purchases can be monitored and controlled in real time

Cons

- Commercial cards can be stolen or duplicated and used for fraudulent purchases

Digital wallets and peer-to-peer payment services

E-commerce payment systems such as digital wallets (eWallets) and peer-to-peer payment services are gaining popularity. Systems such as Apple Pay, PayPal, and BILL let businesses transfer funds to each other. They also offer banking services like online payments, virtual accounts, currency exchange, and escrow services.

Pros

- eWallet and peer-to-peer payments are usually instantaneous

- Easy to use and generally only require the payee’s email address to complete a payment

Cons

- Merchant and processing fees can be very high, especially for credit card or international transactions

- Transferring funds into and out of the payment service can take a long time

International payments

International or cross-border electronic payments are similar to domestic payments but with a couple of differences. International payments are generally slower than domestic payments. They also involve a currency exchange for either the payer or payee. Finally, they usually require more information to route payments between countries and financial institutions.

The two most common types of international payments are international wire transfers and Global ACH payments.

International wire transfers

International wire transfers are similar to domestic wire transfers. Both involve transferring funds between two bank accounts. However, most international wire transfers use the SWIFT system, a secure international bank messaging system, to share routing information.

The payer initiates the international wire transfer, and payment can be in the payee’s home currency. The payee needs to provide the payer with the SWIFT information for its bank account before the transfer can be made.

Pros

- International wire transfers usually take one or two business days to complete

- Wire transfers are secure and reliable

Cons

- Wire transfers are expensive, with a transfer fee for both the payer and payee

- Payees can be exposed to foreign exchange risk if exchange rates fluctuate during the transfer

Global ACH payments

Global ACH, or International ACH, is an electronic transfer service based on the US automatic clearing house (ACH) system. It provides fund transfer services using the ACH system and similar systems in other countries, like Canada’s Automated Clearing Settlement System (ACSS).

Pros

- Global ACH payments are less expensive than wire transfers

- Offer a similar level of security to wire transfers

Cons

- Slower than international wire transfers

- Not available in every country

Choosing the right payment mix

Find the right mix of electronic payment methods for your business by considering three factors:

- Current and future payment methods: What payment methods are you using today, and what do they cost? What is the cost of adding new payment methods?

- Vendor relationships: How healthy are your vendor relationships? How do you choose how to pay each vendor? What payment method do your vendors prefer?

- Payment processes: How do you process payments today? Do you use separate methods for each payment type? What accounting or ERP system do you use?

Let’s dig into these.

Estimate the costs of current and future payment methods

Begin by tracking your current allocation of payments by payment type. Calculate or estimate the per-transaction cost for each type to better understand your total costs.

Next, calculate or estimate the costs of any new payment type you may be considering. Also, estimate the costs to your vendors as well. For example, credit cards and wire transfers usually charge fees to suppliers. Knowing these metrics will help you understand the impact on vendors if you switch payment types.

Once you understand the costs of each payment type, you can look at your current vendor relationships to determine the best mix of payment methods.

Consider vendor relationships

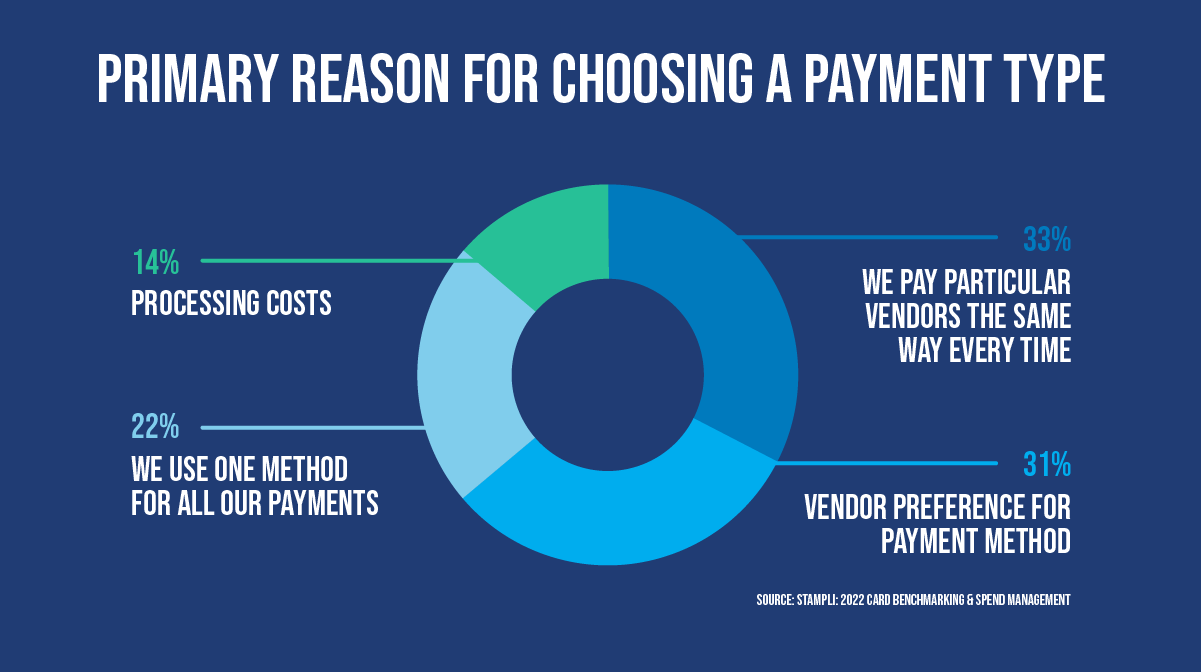

In Stampli’s 2022 survey of finance leaders (Card Benchmarking & Spend Management), 31% said they let vendors choose how they want to be paid. Another 33% said they made payments “the way we have always made payments to a particular supplier.”

Knowing the costs of each payment method is half the battle. To realize savings from a more cost-efficient payment method, you’ll need to convince suppliers to accept that method. Collaborate with your suppliers on choosing how you can pay them.

Ensure you understand and are transparent about the costs and benefits to your suppliers. For example, if you plan to implement virtual cards, explain that although virtual cards may charge a merchant fee, they are also a faster way to get paid. By being open and honest about the impact of changing payment methods, you will stand a better chance of success.

Of course, the most cost-effective and efficient payment method isn’t much use if you can’t make payments on time. To fully reap the benefits of electronic payment types, you need to ensure your payment processes are efficient.

Optimize payment processes

Look at how you process supplier payments today. If you use separate manual payment processes for each payment method, introducing a new payment type has little benefit. Manual processing is slow and error-prone. Adding a new payment type will only add complexity and extra work for your AP team.

Consider investing in a payment automation system as part of your payments strategy. An automated payment solution has several advantages over manual processes, including:

- Unified payment gateway: use a single platform for multiple payment types to eliminate process duplication and complexity

- Better processing efficiency: streamline approval and payment processing workflows to reduce days payable outstanding

- Freedom to choose payment type: payment-agnostic payment platforms let you choose any payment type

- Integration with accounting systems: payment platforms integrate with ERP and accounting software to share payment data

Choosing the right payment automation solution allows you to implement new payment types easily, collaborate with suppliers, and pay invoices on time.

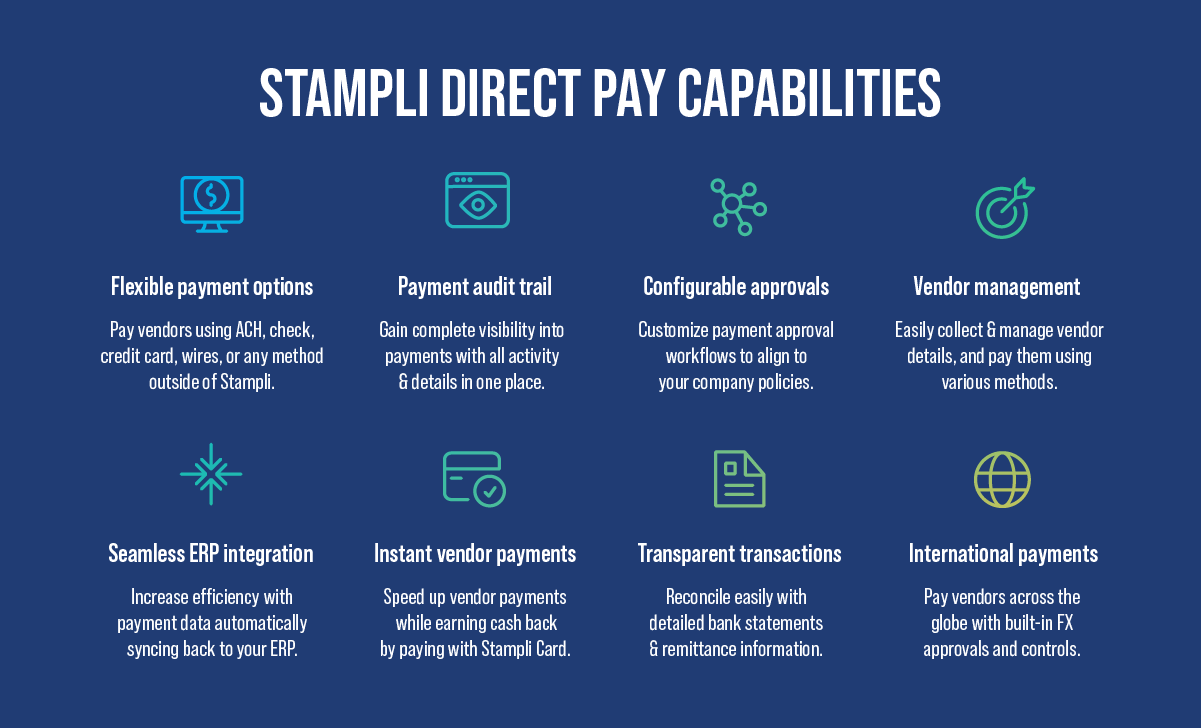

Take control of electronic payments with Stampli Direct Pay

Take complete control over your vendor relationships and make payments without involving any middle party. Stampli Direct Pay is a payment-agnostic solution that extends your payment efficiency and gives you the freedom to pay vendors how you want.

Direct Pay seamlessly integrates with most major ERPs and accounting software providers through APIs, ensuring that your entire company can access accurate real-time business transaction data at any time.

Here’s how Stampli Direct Pay gives you payment freedom:

Payment agnostic

Choose the electronic payment method that suits you and your vendors best.

Simple payment approvals

See payment information and related documents on one page to make approvals easy.

Powerful vendor portal

Vendors can provide payment information, choose a payment method, and check payment status.

Flexible International payments

Manage foreign exchange risk, save on transaction fees, and pay international contractors quickly.

Handle consolidated and partial payments

Make partial payments, consolidate payments, and issue vendor credits with total flexibility.

Own your data

Keep your vendor data even if you switch to a different payment provider.

Enjoy payment flexibility. Contact Stampli today for a free demo of Stampli Direct Pay.