EFT Payments: The Ultimate Guide

As a finance leader, I need to optimize my supplier payment workflows.

Payment efficiency and accuracy are my top priorities, but I’ve also got to reduce costs. Moving to Electronic Funds Transfer (EFT) payments seems like the right path for my business. Still, I’ve got some concerns about how it will work – I don’t want to add another layer of complexity to an already complicated process.

Read on to learn about EFTs: what they are, how they work, their risks and benefits, and how I can find the EFT payment options that are best for my business.

What are B2B electronic fund transfers, and how do they work?

A B2B EFT is any transfer between businesses via a financial institution where the transfer is completely digital. For example, banks have used wire transfers for over 100 years to make money transfers without using physical cash. Also, the IRS uses EFTs (https://www.eftps.gov/eftps/) to facilitate tax payments and tax returns for taxpayers and businesses.

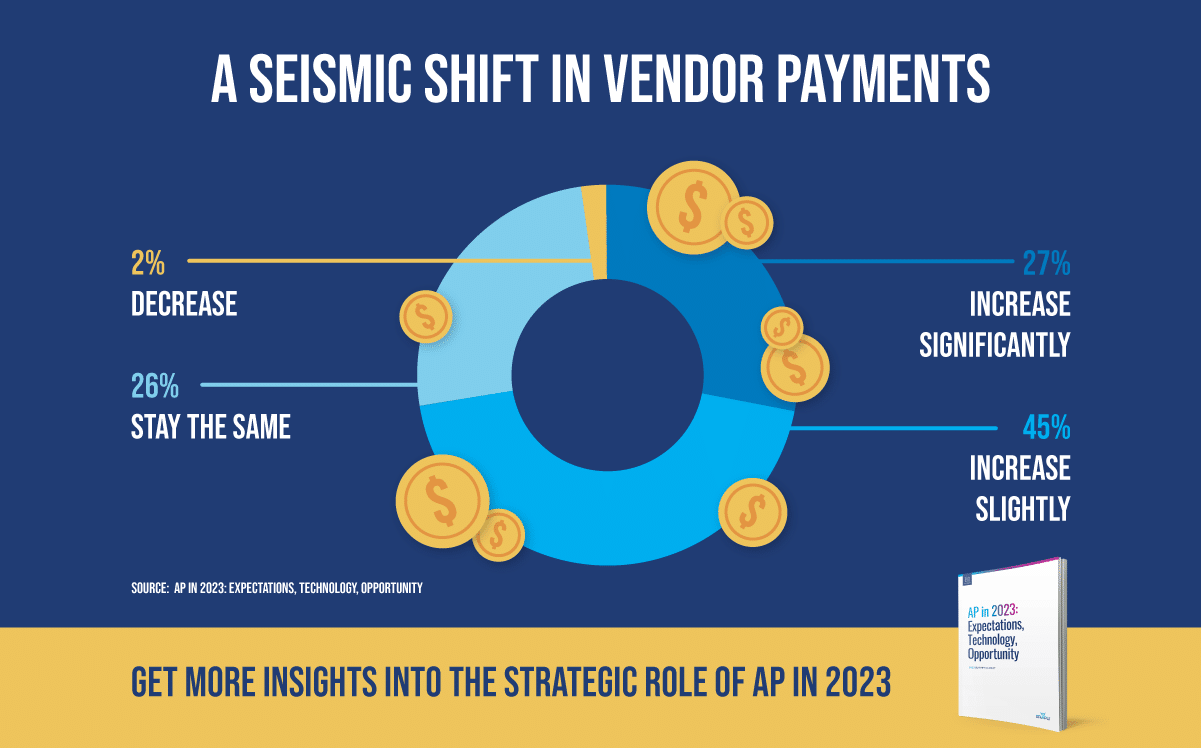

I can use EFTs to move money from one bank account to another anywhere in the world. They’re easy to use, secure and eliminate the need to send paper checks or cash. The use of EFTs by businesses is growing rapidly – in a 2023 survey of finance leaders, 72% said they expect digital payments to increase by 2024. As e-commerce continues to boom, we can expect this growth to continue. I want to get ahead of the game.

Types of EFT payments

There are several types of EFT payments. Here are the ones most often used for B2B transactions:

Automated Clearing House (ACH)

The ACH Network is an electronic payment system that reaches all US banks and credit unions. In 2022, the National Automated Clearing House Association (NACHA) reported that businesses and individuals made 30 billion ACH debit & ACH credit transactions with a total value of $72.62 trillion.

The ACH serves as a channel to transfer money between bank accounts. For example, when a business pays a supplier, they send their bank instructions (bank account number and routing number) on where to transfer the funds. The sending bank notifies the receiving bank of the transfer, and the money is deposited in the supplier’s bank account. You can send ACH in batches to pay multiple vendors.

ACH transactions generally settle in 1-3 business days. The ACH network also provides the backbone for electronic payment methods such as electronic checks (eChecks) and direct deposit.

Wire transfers

Wire transfers are the traditional method of transferring funds electronically between financial institutions worldwide. They are very fast and secure and are commonly used to send large-value transfers. Wire transfers take 1-2 business days, depending on the financial institutions and destination. International wire transfers can be completed over global banking networks like the SWIFT system.

Credit, debit, and payment cards

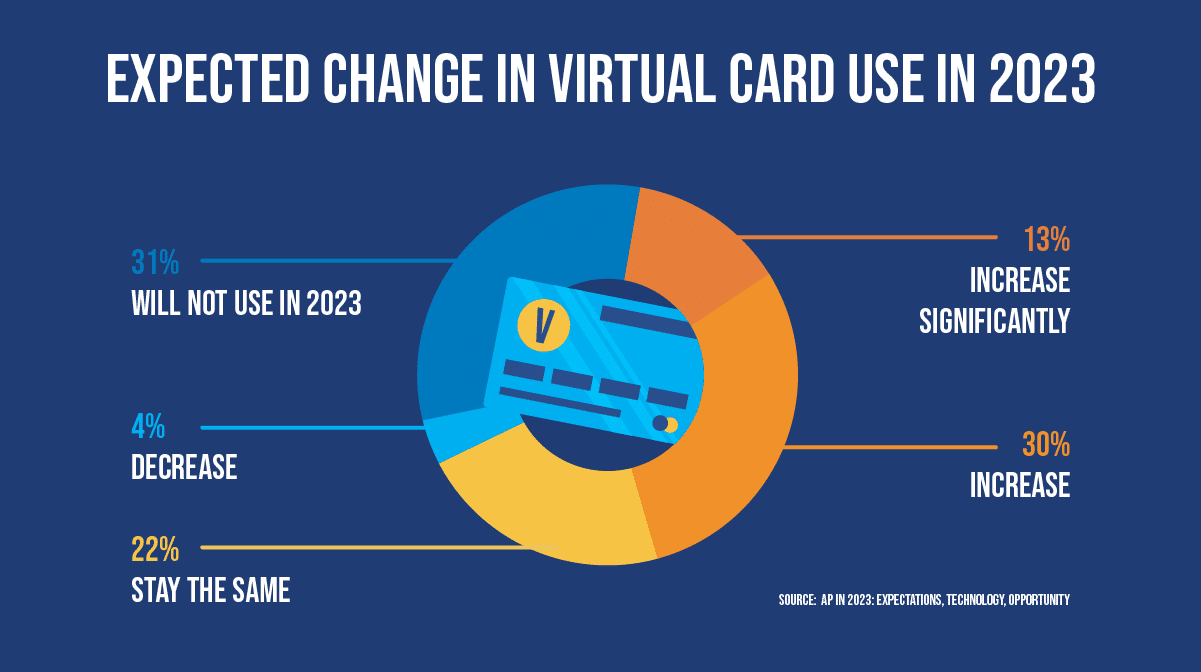

Credit and payment cards facilitate electronic transfers through private financial networks such as Visa or MasterCard. Credit payments are a good alternative to ACH or wire transfers because they are instantaneous, and I can reverse them more easily than ACH payments or wire transfers. Virtual cards are also a rapidly growing method of making B2B payments and offer additional security and spend control features.

Although they aren’t typically considered electronic transfers, cash withdrawals from ATMs are another form of EFT. The ATM provider verifies the transaction and bank account information with the debit or credit card issuer before issuing cash to the cardholder.

eWallets and digital wallets

eWallets and digital wallets such as Apple Pay are growing in popularity for B2B payments. Digital wallets provide a payment alternative to debit cards or credit cards for online payments, such as purchasing or subscribing to apps, and we can also use them for point-of-sale (POS) purchases. eWallet payments are generally instantaneous.

Peer-to-peer payments

Peer-to-peer systems such as PayPal, BILL, and Venmo enable businesses to transfer funds to each other and also provide services such as virtual accounts, currency exchange, and escrow services. Peer-to-peer payment networks usually rely on other EFT methods, such as ACH and wire transfers, to transfer funds between businesses. Payments on peer-to-peer systems can be instantaneous, but transferring funds into and out of the system can take more time, depending on the type of transfer used.

Although many different types of EFT payments exist, they all generally follow the same mechanics.

How EFT payments work

Although payment mechanisms vary, every EFT transaction begins with a sender and receiver. Senders choose an EFT method (usually the one the receiver prefers), enter or select the payment amount, and then enter the receiver’s bank account information. When the payment is approved and initiated, the transfer information is transmitted to the sender’s financial institution, which initiates the transfer of funds from the sender to the receiver’s bank account.

The actual EFT processing depends on the type of transaction. ACH and wire transfer payments are processed over a member-based banking payments network. eWallet or peer-to-peer payment providers may transfer funds between digital wallets or bank accounts. Credit and virtual card transactions are processed over private financial networks.

Regardless of how the EFT payments are processed, electronic payments are secure and fast and are a nice alternative to paper checks for my business. Let’s take a closer look at some of their other benefits and the risks my business might face if we adopt digital payments.

Benefits and risks of EFT transfers

EFT payments carry significant benefits for my business, but there are also some risks I need to consider if I decide to go with a digital payment solution. Here are the key benefits:

Convenience

I won’t lie – digital payments seem like a much better use of my AP team’s time than printing and mailing a bunch of paper checks. We can make our payment run in a couple of hours rather than a couple of afternoons.

Happy vendors

On the same note, our vendors would prefer having funds arrive quickly rather than waiting for a check to come in the mail. Plus, we can ensure our payments aren’t late, saving us on late fees and headaches.

Lower costs

Apart from the cost savings of not having to stuff all those envelopes, EFT payments also help us save a bundle on transaction fees.

More security

Digital payment solutions are more secure than printing checks. We have a transaction record and audit trail for each payment, and we can also detect fraud, errors, and duplicate payments more easily. EFTs are also protected by the US government under the Electronic Fund Transfer Act (EFTA), providing additional security.

Greater visibility

Because EFT payments are so easy to track, we can keep a closer eye on our expenditures, which helps me manage our cash flow better and make informed investment decisions.

Risks of EFT transfers

As nice as EFT payments sound, there are some risks I must consider.

Fraud

Although EFT payments are more secure than paper checks, we’re still at risk of loss due to payment fraud. For example, internal and external fraudsters can process fake transactions or payments, credit cards can be stolen or duplicated, and fraudsters can alter ACH payment batch files. Whatever payment solution we use needs to be able to detect and mitigate signs of fraud.

Errors

Similarly, although EFT payments are more secure, errors can still occur, especially if we process invoices manually. We should consider automating and optimizing our AP processes simultaneously as we move to digital payments.

Reversibility

In case of fraud or an error, it can be challenging to reverse digital payments. Some EFT payment methods, such as credit cards and virtual cards, allow transactions to be halted or reversed. We should understand how easy it is to reverse a transaction with each payment type if needed.

With these risks and benefits in mind, we can look at ways to make EFT payments at our business.

How to make EFT payments

Generally, we can make EFT payments in three ways: manually send payment instructions to our bank, an accounting system or ERP with accounts payable functionality, or a dedicated payment processing solution. Let’s look at each of these in more detail:

Manual EFT payment processing

Manual payment processing usually involves tracking our invoices and approvals with a spreadsheet or accounting software and then manually paying invoices after they’re approved via a bank gateway or by sending payment instructions to our bank. We can also pay suppliers using credit cards or other digital payment methods.

Some obvious problems with manual payments defeat the purpose of moving to EFT payments. First, manual processing is slow, and mistakes get made. It can be tough to detect these mistakes before we make a payment, and almost impossible to reverse an erroneous payment afterward. Second, we have little control over or visibility into our payments – whether they’re late, who we are paying, and how much we’re paying. This makes it difficult to manage cash flow.

Accounting system and ERP payments

Most accounting systems and ERPs include a payment processing system that allows EFT payments. These systems have a significant advantage over manual processes:

- They are efficient and accurate

- We can make payments automatically

- They can automate and streamline payment workflows

Accounting systems and ERPs also provide fraud and error detection capabilities and analytical tools that give us better visibility into our payments.

On the other hand, many accounting systems and ERPs tie you to a single bank or payment service provider, so if you want to use a different corporate card or ACH processor, you might be out of luck. Also, you may need to purchase additional accounts payable automation modules to access automation tools and functionalities fully.

Accounts Payable and payment automation

Purpose-built accounts payable automation and payment processing solutions are designed specifically for accounts payable. They automate and streamline all aspects of the procure-to-pay workflow and offer flexible payment methods. Many AP automation solutions (like Stampli) also integrate with your existing accounting and ERP systems to provide seamless data transfer, ensuring everyone is reading from the same page.

Stampli Direct Pay – Take control of EFT vendor payments

Stampli Direct Pay is a payment-agnostic solution that extends your payment efficiency, visibility, and control over invoice payments.

With Direct Pay, you can fully control your vendor relationships with no middle party needed for your vendor payments. And with seamless API integration with most major ERPs and accounting software providers, you can be confident that your entire company can access accurate real-time business transaction data when needed.

Here’s how Stampli Direct Pay gives you total control over vendor payments:

Payment agnostic

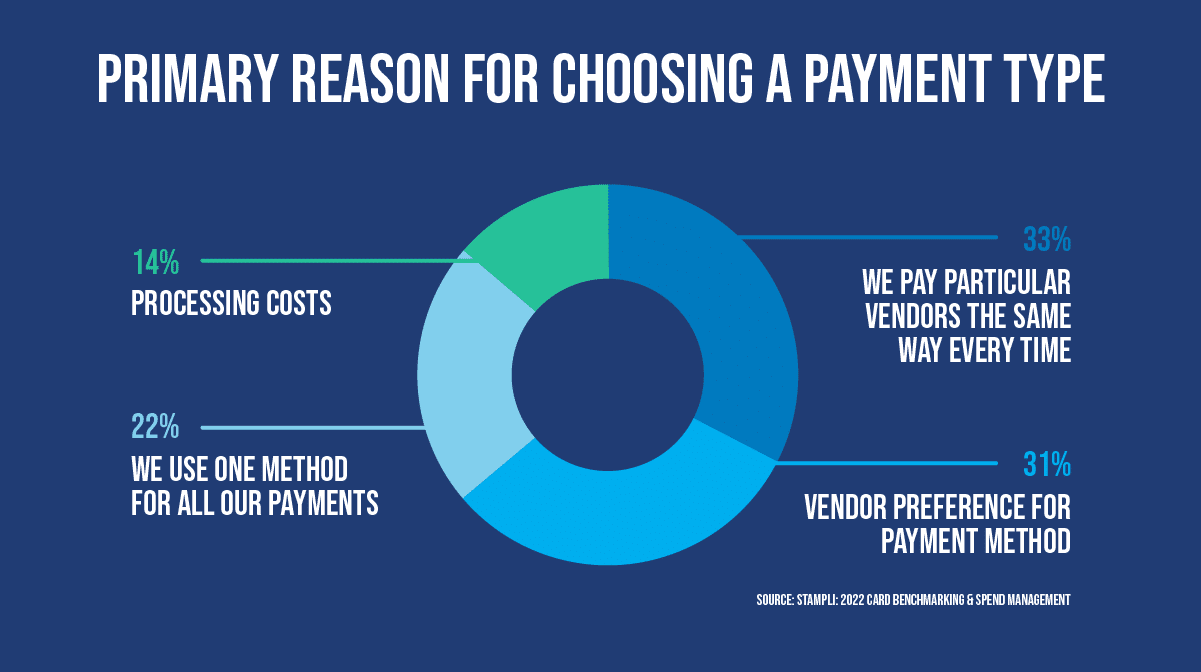

Get total flexibility in selecting the payment type that suits you best. You have the freedom to choose any payment method or provider you prefer.

Streamlined payment runs

Easily view payment information and related documents for a simple payment approval process.

Easy and accurate ACH reconciliation

No more manually matching transactions. Process your ACH payments with individual reconciliations in your bank statement. Other payment solutions make you log into a separate system – outside your bank – for reconciliations.

Powerful vendor portal

With our simple and powerful vendor portal, vendors can easily provide payment information, set their preferred payment method, and check the status of their payments.

Own your data

You can keep your vendor data even if you switch to a different payment provider. Simply download your vendors’ payment information from Stampli Direct Pay.

Direct ACH payments

You can make ACH payments directly from your bank account without setting up or funding a separate settlement account.

Handle consolidated and partial payments

You have the option to make partial payments, consolidate payments, or issue vendor credits with maximum payment flexibility.

Take control of your vendor payments. Contact Stampli today for a free demo of Stampli Direct Pay.