Top Ramp competitors for complete spend management in 2025

Many businesses looking for a spend solution turn to Ramp, a well-known player in the space. The company has extended beyond corporate cards to offer accounts payable (AP) automation for more of an all-in-one spend management solution.

But does Ramp really offer complete spend management?

On the surface, Ramp may look great. It has a low entry price and well-established corporate cards with new AP features to round out their offering. The truth, though, is that corporate card solutions like Ramp only solve the payment piece of spend management, while leaving procurement, approval workflows, and invoice processing disconnected.

What you really need is a Ramp competitor that offers corporate cards as just one part of a complete procure-to-pay (P2P) ecosystem. This means seamless integration between card spend, purchase requests, approvals, vendor management, and invoice processing.

Below, we’ll unpack why card-only spend management looks streamlined and affordable on the surface, but actually costs your organization more than you think. And then we’ll look at Ramp alternatives you’re likely to consider — and the one that actually connects every dot in the procurement process.

What is Ramp (and why does it fall short)?

Ramp is an expense management platform that’s best known for its corporate cards and associated features. It broke into the market in 2019 as a no-fee corporate card promising cash-back savings and automated receipt capture. Since then, it’s layered in bill pay and, more recently, basic AP.

Ramp is now a seemingly appealing option for businesses looking for a broader AP automation solution. It’s well-known in the space and seems to be growing to offer a more expansive set of expense management features over time.

But despite its expansion, Ramp is still architected around the card. Approvals, GL fields, and vendor data are attached after a card swipe, not before it. That means users gain real-time visibility into card charges but can still find themselves reconciling purchase orders (POs), invoices, and non-card spend in separate workflows.

In other words, Ramp’s low upfront price point comes with hidden costs — your team’s productivity. You’re forced to adapt your processes to their rigid, one-size-fits-all system, leaving you with manual workarounds, limited customization, and fragmented workflows that directly drains your efficiency.

Why card-only platforms leave costly gaps

Ramp (and similar card-first tools like Brex and BILL) excels at features like instant card issuance, spend limits, and cashback perks. But the moment a purchase requires a PO, split general ledger (GL) coding, or three-way match, those advantages stop at the swipe. There are hidden gaps, like these:

| Hidden gap | Real-world impact |

| Disconnected procurement intake | Purchase requests still live in Slack threads or emails, so finance sees spend after it’s committed. |

| One-size-fits-all approval flows | Complex orgs need dynamic routing. Card tools force workarounds or multiple rejections and resubmissions. |

| Laggy or shallow enterprise resource planning (ERP) syncs | Daily batch exports mean budget owners act on stale data, and finance spends hours chasing reconciliation exceptions. |

| Vendor and invoice silos | Card transactions, ACH payments, and paper invoices land in different systems, killing true spend visibility. |

| Support and scaling friction | When card tools bolt AP on later, edge cases (multi-entity, partial receipts, dropships) trigger tickets, not touchless flows. |

Card-only platforms solve payment execution but leave procurement, approvals, vendor collaboration, and invoice processing to spreadsheets or secondary tools, dragging your team back into manual mode.

What to look for in a Ramp alternative

As you weigh other tools, consider that a robust competitor should check at least these boxes:

- Unified workflow from request to payment. That means cards, ACH, checks, invoices, and POs are all tied to one timeline.

- Dynamic, no-code approval routing that adjusts to amount, entity, project, or category changes in real time.

- Deep two-way ERP integration for live budget visibility and painless reconciliations.

- Vendor onboarding and compliance baked into the same platform (not a separate portal).

- AI assistance across all spend (for example, GL coding, duplicate detection, and policy checks), rather than card-only insights.

A solution that covers these five key areas will give you full visibility and control over your spend management.

9 top Ramp competitors to consider

Below, we walk through some of the leading Ramp alternatives, looking at where they shine and where costly gaps remain.

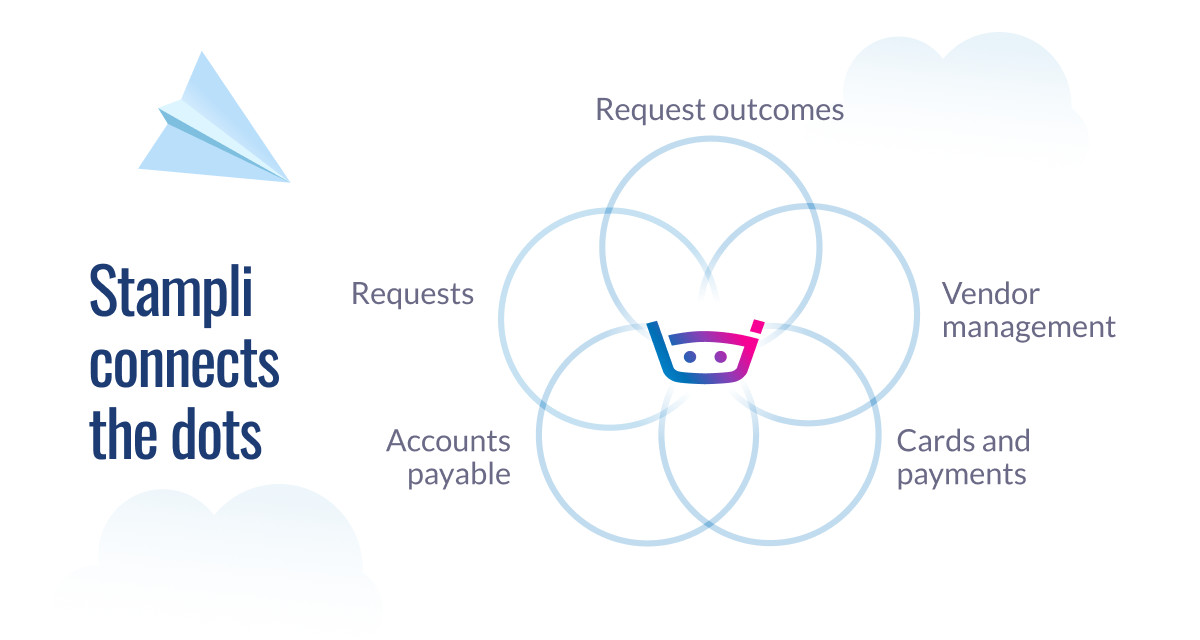

Stampli: The only platform that connects every dot from procurement to payment

Stampli began as best-in-class AP automation and has grown from there. Today, it’s the only solution that’s a true procure-to-pay (P2P) hub rather than an AP bolt-on.

It gives you one workspace that covers purchase intake, dynamic approvals, PO creation, corporate cards, vendor onboarding, invoice capture, payments, and ERP reconciliation. This is all while Billy the Bot AI automates every repetitive step, saving you time so your team can focus on upping efficiency and productivity.

Key features

- Integrated procurement workflow. Create purchase requests, route for approval, issue purchase orders, track fulfillment, and connect to invoice and payment—all within Stampli. Procurement data is linked to budgets and vendor compliance, and every stage is unified with AP and payments in one system

- Complete spend visibility. Cards, invoices, ACH, checks, and POs live on a single timeline, so budget owners see committed spend before money leaves the bank.

- Integrated approval workflows for compliance before spend occurs, not just tracking after. Card issuance is auto-tied to approved requests and live budgets, and rules adapt in real time when an amount, entity, or GL changes.

- Vendor management integration with cards issued for specific vendors and automatic vendor compliance checking.

- Deep, no-rework ERP integrations with 70+ pre-built connectors — no middleware or consultants required.

- AI-powered spend optimization via Billy the Bot, who provides spending insights across cards, invoices, and purchase orders.

- Physical and virtual cards, with settings designed for different types of spend.

- Customizable spending controls with spending limits and restrictions for airtight compliance with internal policies.

- Real-time transaction visibility for complete financial oversight.

“Stampli has been a force multiplier,” one customer says. “It has allowed us to process invoices faster, obtain approvals more efficiently, and gain greater visibility and control over our financial operations.”

Card + AP platforms

1. Brex

Brex still thinks like a card company. It began with startup credit in 2018, then bolted on bill pay and reimbursements over the last few years. It often appeals to VC-backed tech firms needing generous limits, since it offers both a free card tier and a paid “Enterprise” bundle. Plus, the UI is clean and the global FX support can be attractive.

But Brex’s AP feels like an afterthought, resulting in manual work and process breakdowns.

“We’ve had some integration issues [connecting Brex with] with Sage, which has caused us to do some manual work instead of being able to upload transactions directly into Sage,” one customer says.

Key features

- Unlimited virtual and physical cards

- Live Budgets

- Slack approvals

- Premium plans unlock multi-entity GL mapping

Key integrations

- NetSuite

- Intacct

- QBO

2. Airbase

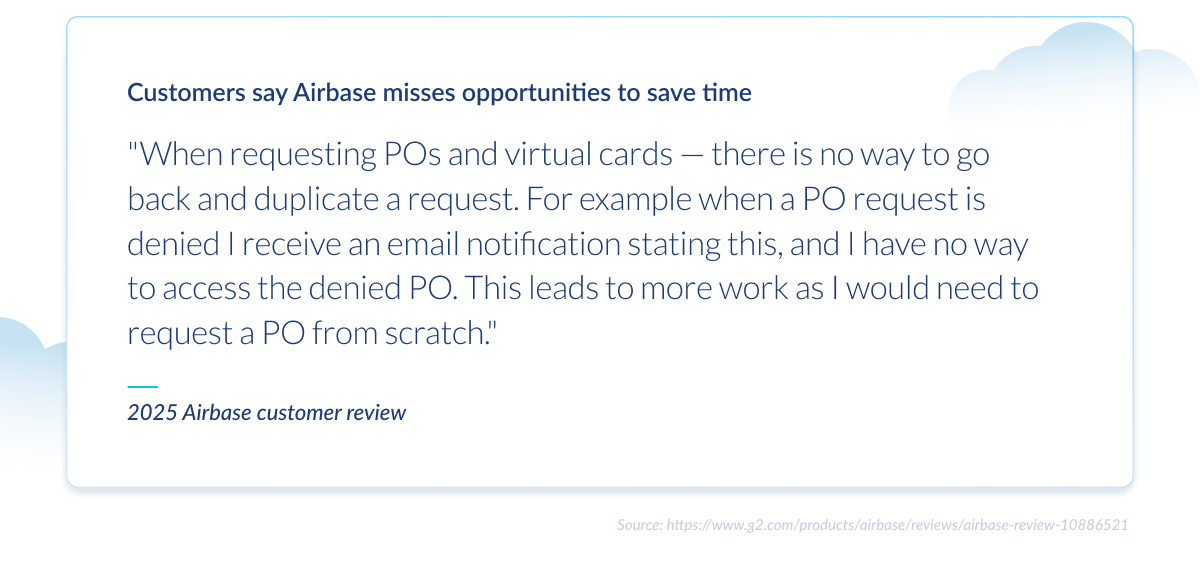

Airbase, owned by Paylocity, markets a “procure–pay–close” suite that bundles cards, AP automation, and reimbursements. Its strength is consolidation, but it gets mixed reviews for its high price tag and procurement depth.

One customer warns, “When requesting POs and virtual cards — there is no way to go back and duplicate a request. For example when a PO request is denied I receive an email notification stating this, and I have no way to access the denied PO. This leads to more work as I would need to request a PO from scratch.”

Key features

- Guided intake forms

- Automatically created purchase orders

- Auto-accruals to NetSuite/Intacct

- AI OCR

Key integrations

- NetSuite

- Intacct

- Dynamics BC

- QBO

Card-only platforms

3. BILL Spend & Expense (formerly Divvy)

Divvy pioneered free virtual cards, and after BILL acquired the company in 2023, it became the card front-end to BILL’s wider finance cloud. It now offers spend management for Quickbooks-centric small- to medium-sized businesses that need spending discipline, not deep procurement or AP.

Key features

- Real-time declines when budgets are exceeded

- SMS receipt capture

- Light bill pay

Key integrations

- QBO free

- Intacct/NetSuite via paid BILL plan

4. Rho

Rho fuses fee-free checking, corporate cards, and basic AP into one portal, pitching itself as “the new standard for business banking.” It’s particularly appealing to bootstrapped startups — it markets heavily to seed-to-Series C orgs looking for simple spend controls — because the platform is free. Rho earns its revenue from interchange and treasury spread.

Key features

- Same-day ACH

- Treasuries-backed sweep accounts

- Mobile receipt texts

Key integrations

- QuickBooks

- NetSuite

- Intacct

- Dynamics 365

5. Rippling Spend

An extension of Rippling’s existing HR and IT cloud, Spend offers precise control over card and bill-pay policies based on employee data. Companies already running Rippling for HR that want lightweight spend in the same login will likely find it to be a convenient add-on.

But for those outside Rippling’s ecosystem, it’s inconvenient. Spend is an additional module that isn’t available as a standalone, and it comes with per-employee costs that add up quickly.

Key features

- Auto-shutdown of cards when offboarding employees

- Role-based limits

- Instant spending rules when issuing cards

- Automated approval workflows

Key integrations

- QBO

- NetSuite

- Intacct

Traditional expense suites

6. SAP Concur

SAP Concur is a legacy enterprise travel and expense (T&E) giant that pairs tight policy control with global spend features — like VAT reclaim and deep travel inventory. It can be a solid choice for international enterprises that already run SAP and need vast travel content with granular policies.

Key features

- Verify, AI-powered anomaly detection

- Mileage and VAT automation

- TripLink off-platform capture

Key integrations

- Xero

- Intacct

- QuickBooks

7. Expensify

A mobile-first receipt app, Expensify later rounded out its expense management offerings by adding the Expensify Card and basic bill pay. It’s loved by users for how convenient some of its features are (especially SmartScan, an app that allows employees to capture and upload receipts by snapping photos and get reimbursed as soon as next-day). For small teams that value low cost and mobile ease-of-use over PO match or vendor onboarding, it can be a solid solution.

Key features

- SmartScan OCR

- Email-in receipts

- Daily card autopay

- Next-day ACH reimbursements

Key integrations

- QuickBooks

- Xero

- NetSuite

- Intacct

8. Navan (formerly TripActions)

Navan started in travel booking and layered on Liquid corporate cards and expense optical character recognition (OCR) to give travelers a single mobile app for a suite of expense management tools. This solution is best for sales-heavy orgs where travel spend dwarfs PO-based purchasing.

Key features

- Dynamic travel budgets

- Instant cards

- AI receipt capture

- Real-time, pre-coded expenses

Key integrations

- Quickbooks

- Netsuite

- Xero

Why integrated P2P wins

Card-first and expense-only platforms solve only a single slice of spend management: They boost visibility after money moves. But they still leave finance teams stitching together requests, POs, invoices, vendor docs, and ERP reconciliations after the fact. Every manual hand-off adds hidden cost — lost context, duplicate data entry, and late closes.

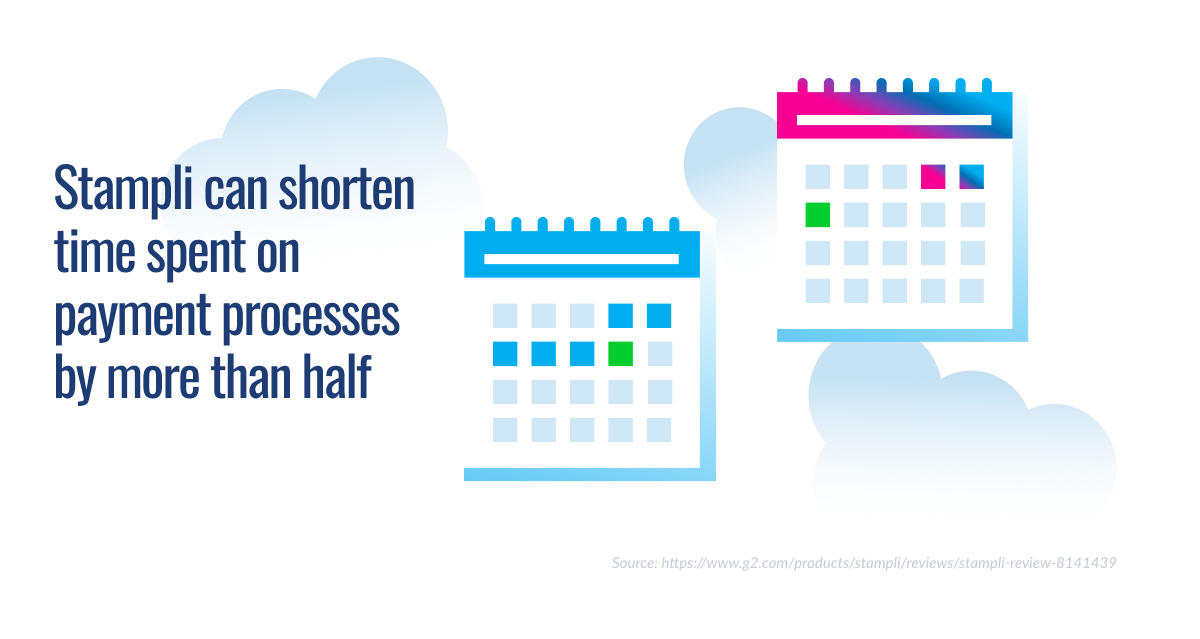

Stampli flips that model on its head. It gives you visibility before spend happens, because the card, the PO, the invoice, and the payment all share one approval timeline and one audit log.

As one customer put it, “The amount of time it takes us from start to finish for payments has gone from about 5 days to 2 days in most cases, some days even same day.”

With faster payments, cleaner audits, and fewer late-night reconciliations, finance stops being the back-office bottleneck and starts driving strategy.

If your goal is true spend control — not another silo to reconcile — see Stampli in action by booking a demo today.