Brex Alternatives: When to Opt for Stampli or Other Options

Companies are generally wise to have a variety of payment options at their disposal and these days, there’s no shortage of potential ways to make payment. One of these is Brex, a San Francisco-based company founded in 2017 that offers a type of business credit card ideal for startups and small businesses.

But it might not be the last spend solution that a business will ever need.

While Brex is a fast-growing and useful solution in several areas, some companies might find that they need to look beyond it to get their needs met. For any business this might apply to, we’ve assembled some Brex alternatives. Read on to see where your business might land.

What Brex Is and Why It’s Sometimes Not an Ideal Fit

First, let’s look at a few basics about Brex and why it might not be the best solution for certain companies.

What Brex Is

Brex offers a business credit card and is a fast-growing FinTech company, with more than 20,000 customers as of April 2021, according to the blog for Y Combinator, the Silicon Valley startup accelerator where Brex got its start.

“Brex is building a full financial operating system that keeps getting more comprehensive, all of which will delight existing customers and attract new ones,” one of their investment partners said in a press release after a recent funding round.

But even as well as the company has been doing, there are some parts of the market it might not be able to reach optimally at this juncture.

Who Brex Best Helps

Brex, as that Y Combinator piece noted, got its start after its co-founders, who are from Brazil, couldn’t get approved for business credit due to their limited U.S. credit histories, despite having $125,000 in the bank. Perhaps like many entrepreneurs, they built a product that can help the types of customers they were, namely startups or small businesses.

Customers, who must be incorporated businesses and meet a few other requirements, essentially get a net-30 day card that gives businesses a month to pay for purchases. These purchases can earn the businesses rewards in the form of points. They can also help the businesses build credit histories, with Brex providing an option to report credit histories to Dun & Bradstreet and one of the three major reporting agencies, Experian.

As NerdWallet notes, some of the advantages of Brex, through its Brex Cash product, include a lack of fees, the availability of the Brex Card (which works with vendors and suppliers who accept MasterCard), and special expense management capabilities.

Types of Companies That Might Be Better Suited to Look Elsewhere

If you’re a small business or startup that’s incorporated, Brex can be a good solution. This leaves out a lot of market segments, though, such as freelancers or anyone operating as a sole proprietor, the latter of which is the most common type of business in the United States, according to the Small Business Administration. Even for incorporated businesses, Brex requires maintaining a $25,000 minimum balance. A lot of bootstrapped operations won’t have those funds available.

Brex also might not be the best solution for mid-market and enterprise-level businesses who’d like more functionality than what Brex currently provides. Among the limits, businesses can’t obtain individualized payment cards for their employees.

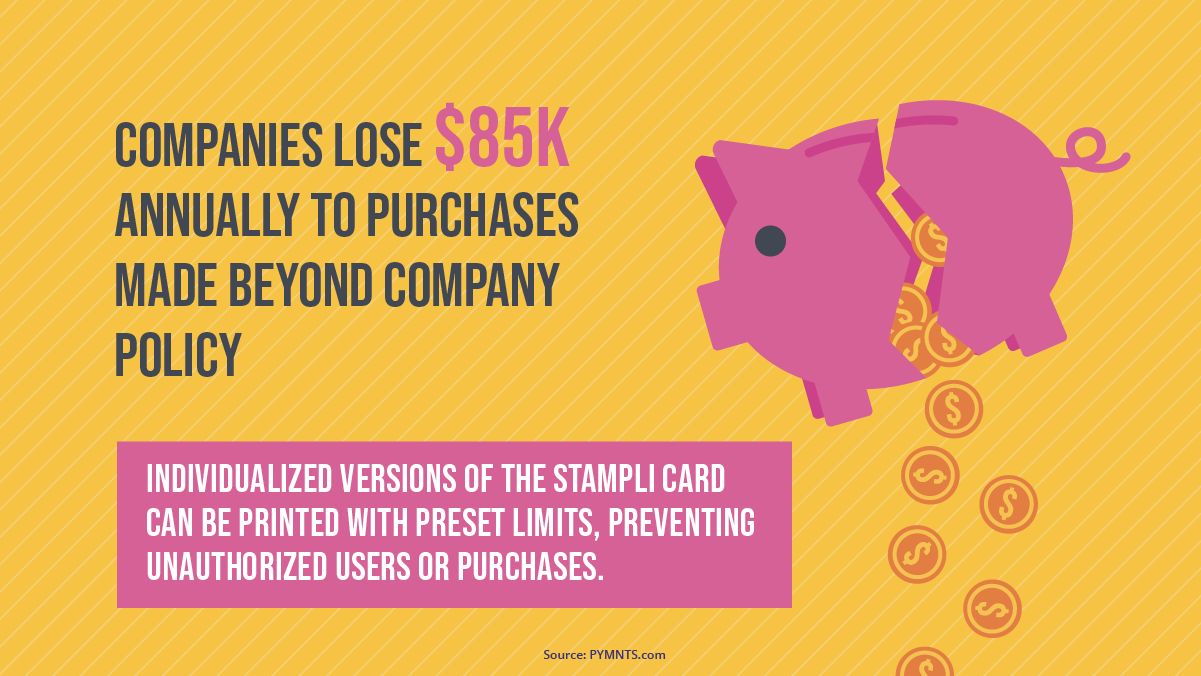

Cards with preset limits for each transaction can be excellent protection against internal fraud. Fraud remains a common scourge, with companies losing an annual average of $85,000 “on purchases made outside of company policy,” according to PYMNTS.com in October 2021.

This isn’t to dissuade businesses from ever using Brex. It just might be good to have some alternatives lined up.

Three Brex Alternatives to Consider

Not every business is going to fit the type of customer Brex can serve. Here are three Brex alternatives to consider.

1. Stampli

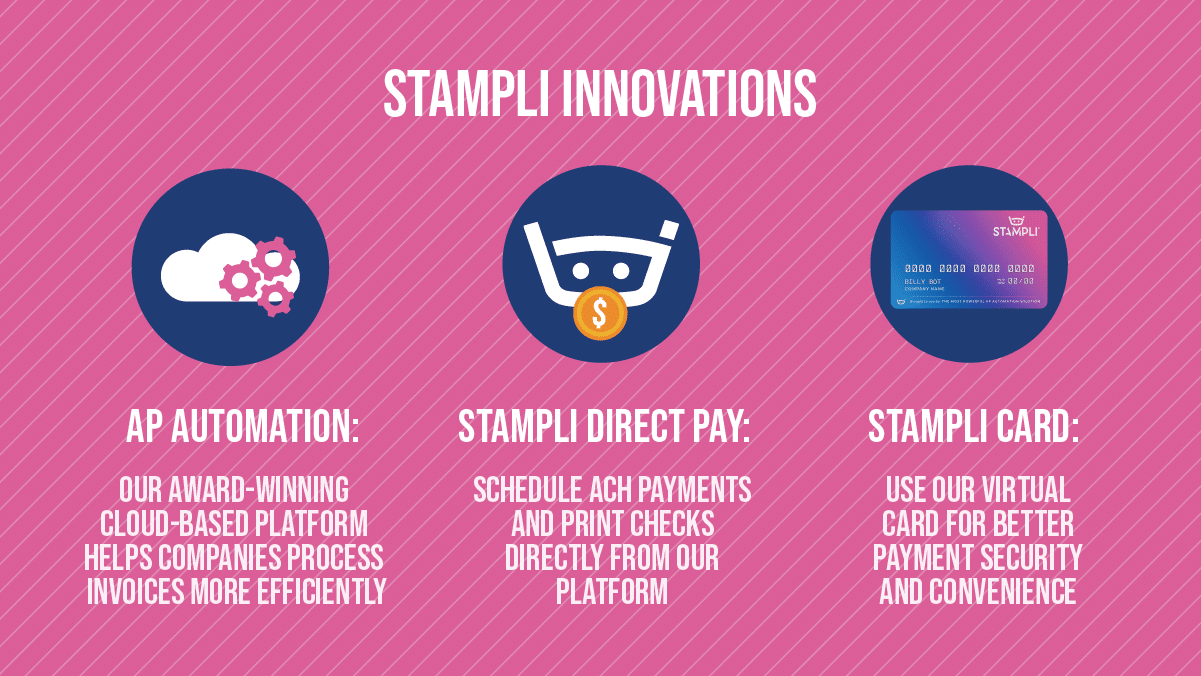

Stampli has made its name providing a cloud-based AP automation platform that uses artificial intelligence and machine learning to help companies process invoices cheaper, faster, and with fewer errors. It primarily benefits mid-size and enterprise-level companies, though it can also work well for smaller businesses, provided they have sufficient invoice volume to justify the cost of accounts payable software.

Since launching our AP solution, though, we’ve discovered that it has more applications than just end-to-end invoice processing. One of these applications is payments, and we’ve launched multiple tools related to it in the past two years. These include the Stampli Card, a virtual payment solution that is the only card directly integrated with an AP automation platform.

With the Stampli Card, companies can quickly issue individualized virtual cards to employees with preset limits geared around specific transactions. This is great for ensuring that employees are able to immediately make whatever purchases they need, while assuring companies that the same employees won’t make additional unauthorized purchases. Having a B2B payments application directly tied into our platform also offers spend management benefits.

Types of customers best-suited: Mid-size and enterprise-level businesses, and any business that needs a higher level of payment security than what Brex can offer.

2. Divvy

Stampli launched as AP automation software and has evolved to include payments and spend management capabilities, and Divvy is similar. Divvy was initially an expense management tool. It now offers free cards as well as the ability to pay bills and reimburse employees for expenses, among other applications.

Small businesses might also be interested that Divvy is currently available free of charge and, similar to Brex, offers a points-based rewards system that scales depending on how often companies are willing to make payments.

Some drawbacks of Divvy include that it works with vendors who accept MasterCard, but not Visa. It also has limited ability to integrate with certain ERP systems (unlike Stampli, which is extremely versatile and can integrate with systems from Microsoft, Oracle, Sage Intacct, and SAP, among others.)

Types of customers best-suited: Small businesses that would like a free solution and haven’t invested in an ERP.

3. Ramp

Not every business will be enticed into using a payment card or system strictly for the possibility of earning points, which can be like the equivalent of amusement park dollars – fun to collect and with some redeemability, but pretty limited in their use overall. For customers who would prefer to earn cash rather than rewards, one option to consider is Ramp.

New York-based Ramp (which is not to be confused with a UK-based company of the same name seeking to be the PayPal of cryptocurrency) provides 1.5% cashback on every purchase. Like other solutions here, it can provide expense management and also offers a report on savings. Similar to Stampli, it can also prompt employees to take certain actions and it can assist in reconciliations.

Types of customers best-suited: Businesses that are looking to receive cashback on purchases.

See if a Brex Alternative Such as Stampli is Right For You

In 2021, Stampli and Treasury Webinars produced a survey report, “How & Why Companies Choose Payment Types” that confirmed something we believe strongly in: There isn’t a right or wrong way for companies to make payments. Some companies prefer to pay their suppliers by check, some prefer ACH, and some prefer other methods.

Again, there isn’t a right or wrong way to pay, or a single method that should be locked into at the expense of all others. There’s just what works in a given situation based on a number of factors, including the preference of a recipient vendor or supplier.

Here’s why you should include Brex alternatives like Stampli among your payment options:

The Importance of Payments Security

Fraud has plagued businesses and their accounts payable payable departments for generations and will likely continue to be an issue for the foreseeable future.

In a distributed and remote business landscape, companies need to know that they have payment options that are both convenient and secure. Partners like Stampli and its Stampli Card innovation help ensure that this will continue to be the case.

Enhanced Expense Management with AP Automation Integration

Economic times continue to be uncertain and many businesses these days want to know that they’re making essential purchases and not unnecessarily bleeding money. Accordingly, expense management is becoming increasingly important for businesses, as is finding new and innovative ways to do it.

In the past, an accounts payable specialist could just look at a monthly credit card statement or go through receipts on an expense report and know that everything was alright. Expense management will likely be much smoother if it’s being performed by an AP automation platform such as Stampli, which addresses every step of the procurement to payment process.

Aside from all of the necessary data for a company to do expense management living within the platform, our AI and machine learning tools can rapidly review the data to sense purchasing trends and unusual transactions.

Stampli: An All-In-One Solution to Take Your AP Operations to the Next Level

Overall, there are a lot of different business credit card solutions on the market. Where Stampli can differentiate itself is that payments are just part of everything we do.

We’re an all-in-one solution that can help companies transform their procurement-to-payment process and enjoy a new era of AP capabilities.

Stampli, an all-in-one corporate card and spend management solution. Try the Stampli Card today.