The Nuances of EFT vs ACH Payment Methods

Business, like so much of life, is situational. What works in one instance might not work so well in another.

Today, we’ll explore a hypothetical situation of a business having to choose between initiating an electronic funds transfer (EFT) or automated clearing house (ACH) payment. We’ll show how business leaders can choose between those payment types and how accounts payable (AP) automation software can help them do it.

Option 1: ACH Payments

It was 2 p.m. on a Tuesday when the hypothetical company we’ll write about, a Midwestern law firm, realized it needed to send a payment of $80,000 as soon as possible to a private investigator (PI) it regularly used to research pending cases. Good PIs don’t come cheaply and when they become disgruntled, the legwork needed to build a case can grind to a halt.

The firm knew the clock was ticking and thought first of using one of the most common methods of payment in the US today: the ACH.

General ACH Uses

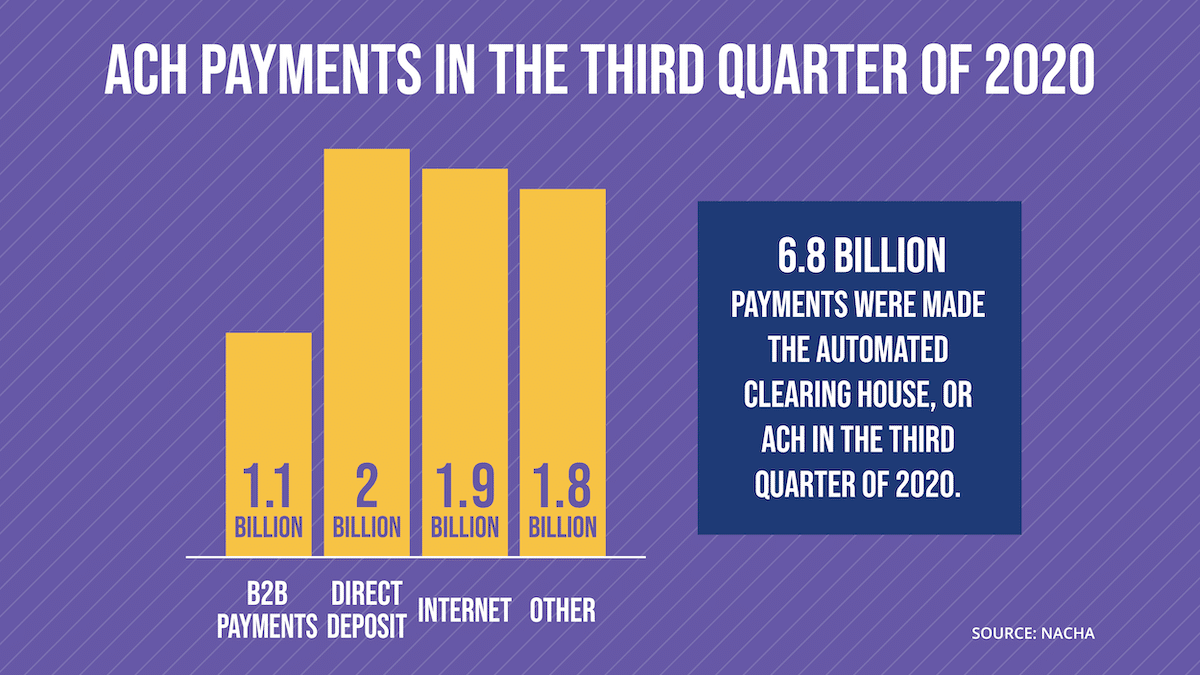

In the little over 50 years that it’s been in use, the ACH has grown to become a highly-utilized payment form. Roughly 6.8 billion payments were made with the ACH in Q3 of 2020, according to the National Automated Clearing House Association, or NACHA, representing a 9% rise over the same period in 2019.

Workers have opted for the ACH for years, with more than 90% of employees receiving their paycheck via it, since it’s the preferred method for direct deposit. Among the Q3 ACH payments, 15.8% or approximately 2 billion were used for direct deposit. The ACH has been increasingly popular for B2B payments as well, with those rising 12% in the third quarter of 2020 over the same period the year before.

The Upsides of ACH Payments

People like the ACH because it’s reliable, puts money into their bank account without any action on their part, and is relatively quick, with payment typically arriving within 3-5 business days. The fees are also cheap, at most a few dollars per transaction, according to Nerd Wallet and generally $0.20 to $1.50 per payment. It’s often cheaper than the cost of a stamp to mail a paper check and that doesn’t even factor in the savings in personnel time.

There’s really not too much downside with the ACH. With a little bit of planning, businesses can schedule an ACH payment and know that it will get where it needs to go by the time they need it to, so long as they initiate the process well enough in advance. As long as the person or company they’re paying is comfortable with being paid by ACH, it’s generally a good way to go.

ACH Drawbacks

Sometimes, though, the ACH isn’t always the best way to go, including for higher dollar transactions or ones that need a higher level of security than the ACH might offer.

Beyond this, limits exist for ACH transfers at different banks, including $25,000 per day at Chase, $2,000 per day at Citibank, and $10,000 per day at Capital One. People may also need their money sooner than 3-5 business days, which was the case in our hypothetical scenario, with the law firm’s investigator hoping she might be paid the same day.

While there has been a sharp rise in same day ACH payments in recent years, with volume climbing 41% over the preceding year, per NACHA, not every accounting system or company is equipped yet to make these types of ACH payments. The daily cutoff window for same day ACH is also currently 1:45 p.m., which was 15 minutes before the law firm realized that it needed to make a payment.

Option 2: EFT Payments

The law firm knew that its private investigator needed her $80,000 as soon as possible. With time running out on a Tuesday afternoon and the possibility that an ACH payment might not even reach the investigator until the following week, the firm turned to a second possible payment type: An electronic funds transfer.

General EFT Uses

Broadly speaking, electronic funds transfer or EFT payments can mean anything from a credit card swipe at a supermarket checkout stand to a sophisticated wire transfer. As Bankrate.com defines, “An electronic funds transfer is a widely used method for moving funds from one account to another using a computer network. Electronic funds transfers replace paper-based transfers and human intermediaries, but provide the customer with the convenience of doing her own banking.”

Technically, EFT payments can include ACH payments, though that doesn’t make them one in the same. But in this case, the law firm quickly began to zero in on another type of EFT payment: a wire transfer.

The Upside of EFT Payments

EFT payments like wire transfers, which have existed since Western Union made the first ones in the mid-19th century, are payments initiated between two financial institutions.

There’s no requirement that EFT payments like wire transfers pass through the automated clearing house in the middle of the transaction. They’re relatively straightforward and direct transactions. Not surprisingly, EFT payments can go through much quicker than ACH payments, sometimes almost instantaneously and usually within one business day. It’s the way to get people paid who need their money as soon as possible, but aren’t available for in-person payment.

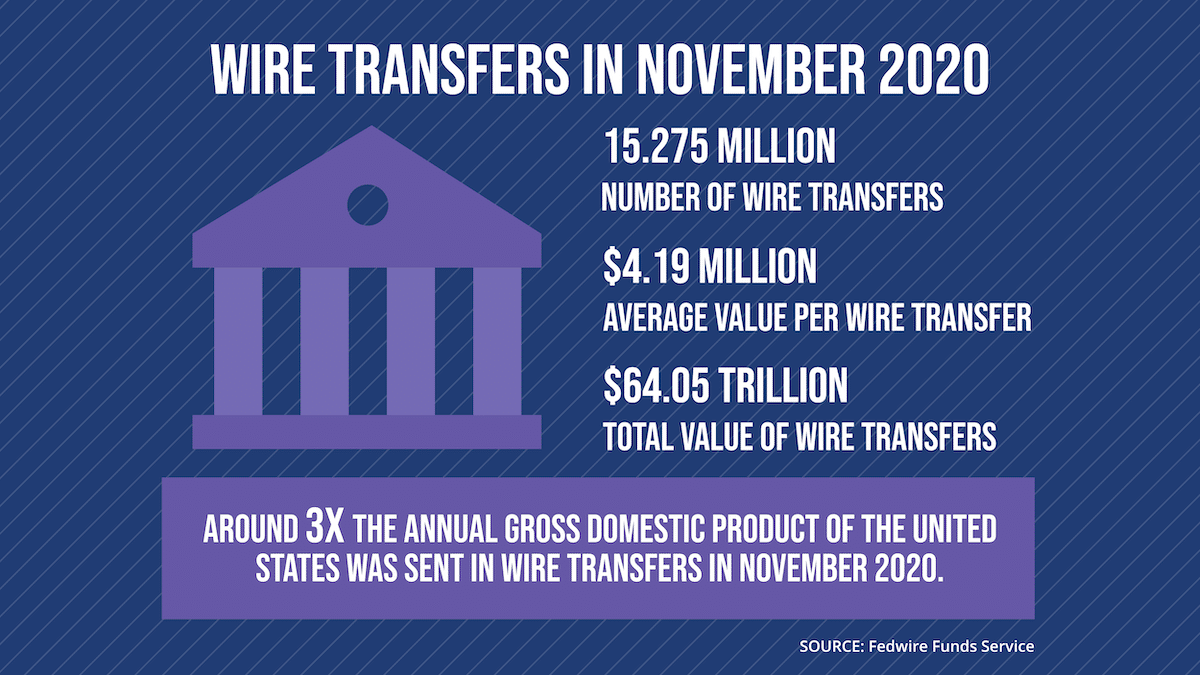

Wire transfers are both significantly lower in volume and tend to be used for higher-dollar transactions than ACH payments. Fedwire Funds Service reported an average value per transfer of $4.19 million in November 2020 and 15.275 million wire transfers in all. While that’s an absolute drop in the bucket compared to the 6.8 billion ACH payments in the third quarter of 2020, it still equals around 200 million wire transfers per year. A few trillion dollars gets transferred by wire each and every day.

On a side note, while it’s well-documented that the economy has been on shaky ground for months amidst the COVID-19 pandemic, one possible sign of recovery could be that average daily wire transfer volume in November 2020 hit its highest point since the beginning of 2015, with 803,978 wire transfers.

EFT Drawbacks

Be prepared to pay a lot more in wire transfer fees in comparison to the ACH. As Business Insider notes, “Wire transfer fees are generally between $25 and $30 for outgoing transfers to a bank account within the US, and between $45 and $50 for transfers going out of the US.”

Generally, a wire transfer is worth doing either if a customer demands it or if the time constraints or dollar amount of the transaction makes using the ACH infeasible. In the hypothetical case we speak of here, the law firm determined that its investigator needed her $80,000 so soon that a wire transfer was really their only option. The firm initiated the payment and within two hours, the investigator had her money.

Summing up EFT vs. ACH and How AP Automation Helps

All was well within the hypothetical law firm’s world. Their investigator got paid a large sum very promptly and the money got to her securely and without any other problems.

As mentioned at the outset of this, though, every situation in business is different. Here are some general pointers on when to use EFT vs. ACH payments.

Recap: When to Use ACH

If it’s routine, the ACH should work just fine for payments. It’s why the fictional law firm we speak of and many real-life companies trust the ACH to handle direct deposit of employee paychecks. It’s also why around 75 million payments will be made on the ACH Network each and every day.

There are limits of course to the effectiveness of the ACH, with the money needing up to five business days to get to the recipient’s bank account and some financial institutions placing limits on how much can be transferred via the ACH.

All in all, the ACH is great. But it’s not for every payment situation.

Recap: When to Use EFT

For larger dollar transactions or ones that need to arrive in short order, EFT payments like wire transfers can be a smart way to go.

While the fees are several times higher for wire transfers than ACH payments, sometimes as much as $50 per transaction, that can be a small price to pay for the peace of mind that comes with knowing a large payment can be made securely and quickly.

It’s all about deploying EFT payments like wire transfers in the right situations. After all, if they were used every time out, businesses would quickly go broke.

AP Automation Software Helps With EFT and ACH Payments

It goes without saying that businesses needn’t go it alone on making EFT and ACH payments. Accounts payable automation software is making it increasingly easy for businesses to handle every step of the procure-to-payment process, with payment agnostic solutions allowing for remittance in whatever methods a vendor prefers.

After all, nobody ever really knows what the next situation will call for for a business.

Whether you prefer EFT or ACH, Stampli can work for you. Learn about our payment agnostic solution.