Six B2B Fintech Trends That Will Shape 2021

In a sense, the COVID-19 pandemic was like the perfect storm for the B2B financial technology space, as well as the broader accounting world.

Already, things had steadily been changing for some time, from more digital payments to increased automation to better awareness of the role artificial intelligence can play in the sector. This gave way in early 2020 to broadscale change as employees began working from home en masse and economic shockwaves rippled. Even with the development of multiple vaccines, these impacts don’t show signs of abating anytime soon.

Still, there’s no need to fear the unknown. With knowledge of some of the latest B2B fintech trends, it’s possible to get by and even to thrive in a vastly different business world.

COVID-19’s Impact on Pre-Existing B2B Fintech Trends

First, let’s look at what was already underway with B2B fintech trends when the pandemic began forcing business closures in March 2020.

1. Greater Flexibility for B2B Payment Options

More B2B payments are being made electronically than by check. It used to be that banks and traditional financial institutions more or less held a monopoly on B2B payments and that paper checks or cash were pretty much the only way people got paid. Today, AP partners are focusing on payment-agnostic platforms that provide maximum payment flexibility. Customers should be free to pay and get paid in whichever manner they prefer and technology can and does enable this.

2. Increased Usage of AP Automation

Another thing that’s changed a lot in recent years has been the sheer number of AP departments which have switched from manual accounting processes involving paper checks, data entry, and internal accounting systems to state-of-the-art, cloud-based automation platforms.

These systems allow for far more efficient and cost-effective accounting operations. AP automation also reduces data entry errors and increases security. Stampli, for example, streamlines invoice processing and the approval process by centralizing communication on the actual invoices, which reduces duplicate payments and ensures only approved personnel can access sensitive data.

All in all, AP automation software is like having an extra analyst (or 10) on-staff at the cost of the service.

3. Greater Acceptance of Artificial Intelligence and Machine Learning as a Means to Prevent Fraud

In recent years, some of the new systems to hit the market have leaned heavily on machine learning and artificial intelligence.

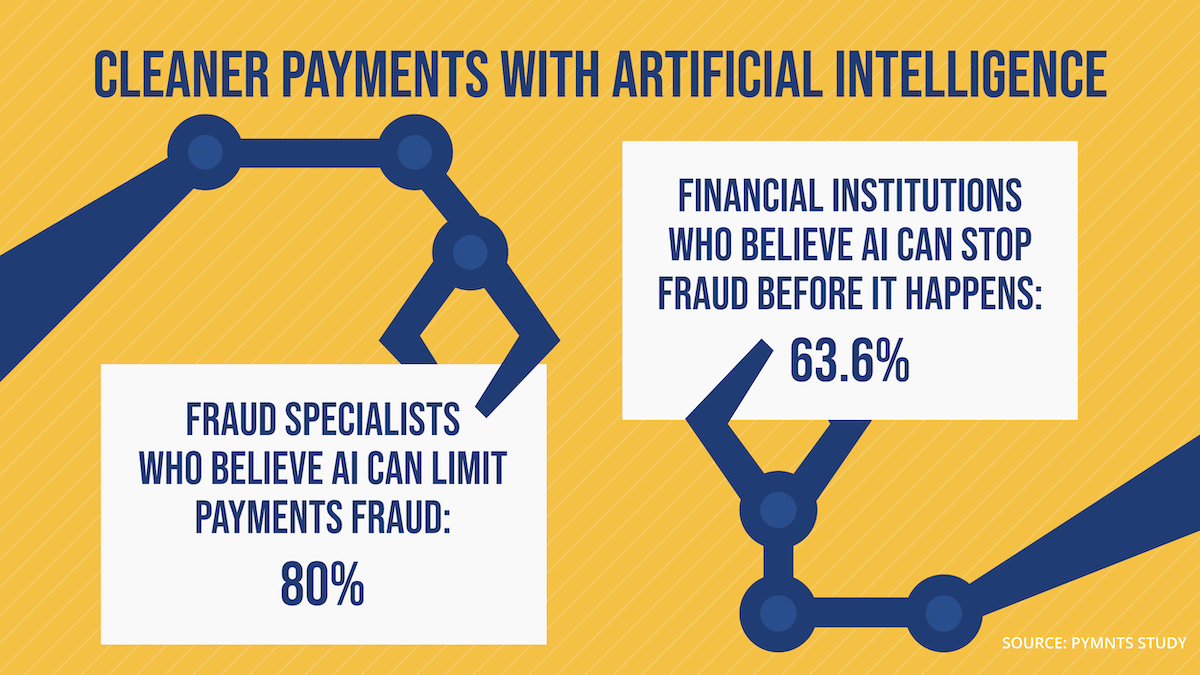

AI, like Stampli’s bot Billy, can pore through literally myriad transactions, analyzing payment trends and monitoring for possible signs of fraud. And there’s starting to be more understanding of what robots like Billy can do. In a PYMNTS study, 80% of fraud specialists who used artificial intelligence believed that it could limit payments fraud. In that same study, 63.6% of financial institutions believed that AI could help stop fraud before it even happened.

Interestingly, though, while PYMNTS noted that AI was being “rapidly being deployed by financial institutions… as the payments ecosystem becomes more complex,” only 5.5% of banks were using true AI, suggesting that there’s still a lot of room for it to develop within the payments space.

B2B Payment Trends We Can Expect to See Accelerate in 2021

Clearly, times are tough in the business world. Here are some B2B fintech trends being brought to the forefront by COVID-19.

4. Remote and Smaller AP Operations

While B2B payment has migrated more and more online in recent years, accounts payable had stayed a largely in-person affair, with staff generally having to come to physical offices to process invoices, track down approvals, and make payments.

This all changed with COVID-19. As the technology website Hacker Noon noted in November, “Due to the pandemic, we saw a shift in fintech trends where most companies switched from on-premise to remote overnight.”

For now, AP operations remain largely in-office, but this could change in time, too, with the dramatically-increased emphasis on remote work.

Many accounting staff have also been having to make due with less as they’ve transitioned to remote positions. PYMNTS noted that a study of 17,000 professionals conducted last March found that 44% of finance sector employees were anticipating layoffs at their companies. “This environment encourages businesses to adopt AP tools that will help them meet their payment obligations without overburdening the remaining staff,” PYMNTS wrote.

It’s another reason for any company that hasn’t done so already to look to AP automation in 2021. It might be that accounts payable departments remain lean and fragmented for the foreseeable future, needing every possible edge they can find. Automation software can play a vital role in helping shore up these types of environments.

5. Fewer Financial Institution Employees, More Collaboration with Fintech

Recessions have a way of rattling the financial sector, with the former Washington Mutual Bank going under in the financial crash of 2008 and, more recently, HSBC eliminating 6,000 jobs in October.

Accordingly, for the B2B payment world, shaky economic periods are as good time as any for businesses to reevaluate where they keep their money, if the financial institutions that they work with are distressed in any way, and if stresses are contributing to higher transaction fees, longer payment cycles, and such.

It also might be more difficult at this time for companies that need financial institutions to extend lines of credit for paying bills. For this reason, it’s smart for companies to try to do everything they can to get their bills lower, including by trying to pay them off sooner to capture the nominal 2% to 3% early payment discounts that vendors are often happy to extend.

Companies could also look to fintech companies ahead of looking to traditional financial institutions. The banks might be doing this already, anyhow, with one fintech executive writing in November, “Financial institutions are more likely to collaborate with FinTechs than compete with them as FinTechs continue to seek more traction in an extremely competitive market, and financial institutions seek more sophisticated partners.”

6. More Investment in B2B Lending and Other Fintech Solutions

Uncertain economic times can also mean tighter lending restrictions from traditional financial institutions, who might want a closer look at a company’s profit-and-loss statements before deciding whether to loan money.

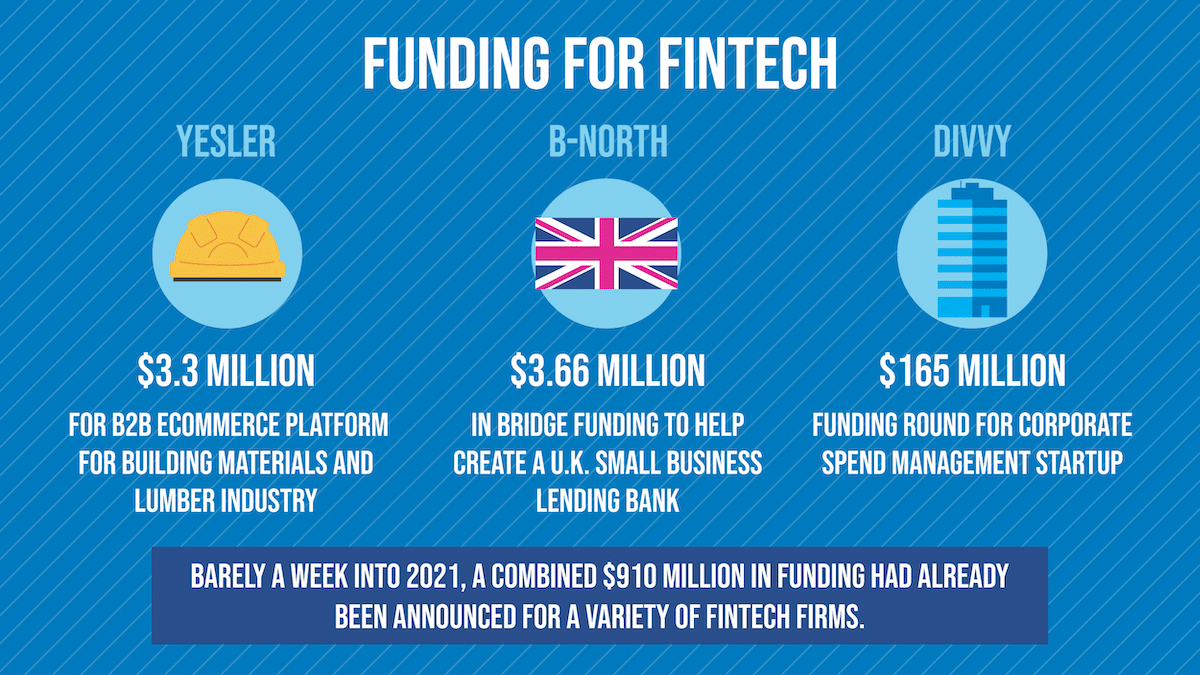

Even in normal times, funding can be a common stumbling block for small and growing companies — and traditional lenders often require intense application requirements for high-interest loans. Interestingly, though, B2B fintech startups are currently having a moment, with PYMNTS noting Jan. 8 that “industry players raised more than $910 million in combined funding” for industries including small business banking and lending.

It could be that these backers realized that in precarious economic times, having a diverse B2B lending landscape is a good thing for all involved.

Stampli can help you keep up with the latest fintech trends. Come see the difference today.