How ePayables Can Benefit Your Business

ePayables are virtual payment cards that businesses can use to pay suppliers. Each ePayable card is assigned to a specific supplier. When the supplier sends an invoice, the buyer pays the supplier by instructing their financial institution to transfer the invoice amount to the virtual card. The supplier charges the ePayable, and the money is transferred to their bank account.

One way to think about ePayables is to compare them to using your credit card online or over the phone. Instead of swiping your physical card, you use your credit card as a virtual card. Only the card number, expiration date, and CVC are used for the transaction. ePayables cards are usually provided by credit card providers such as Visa, Mastercard, or financial institutions like Bank of America.

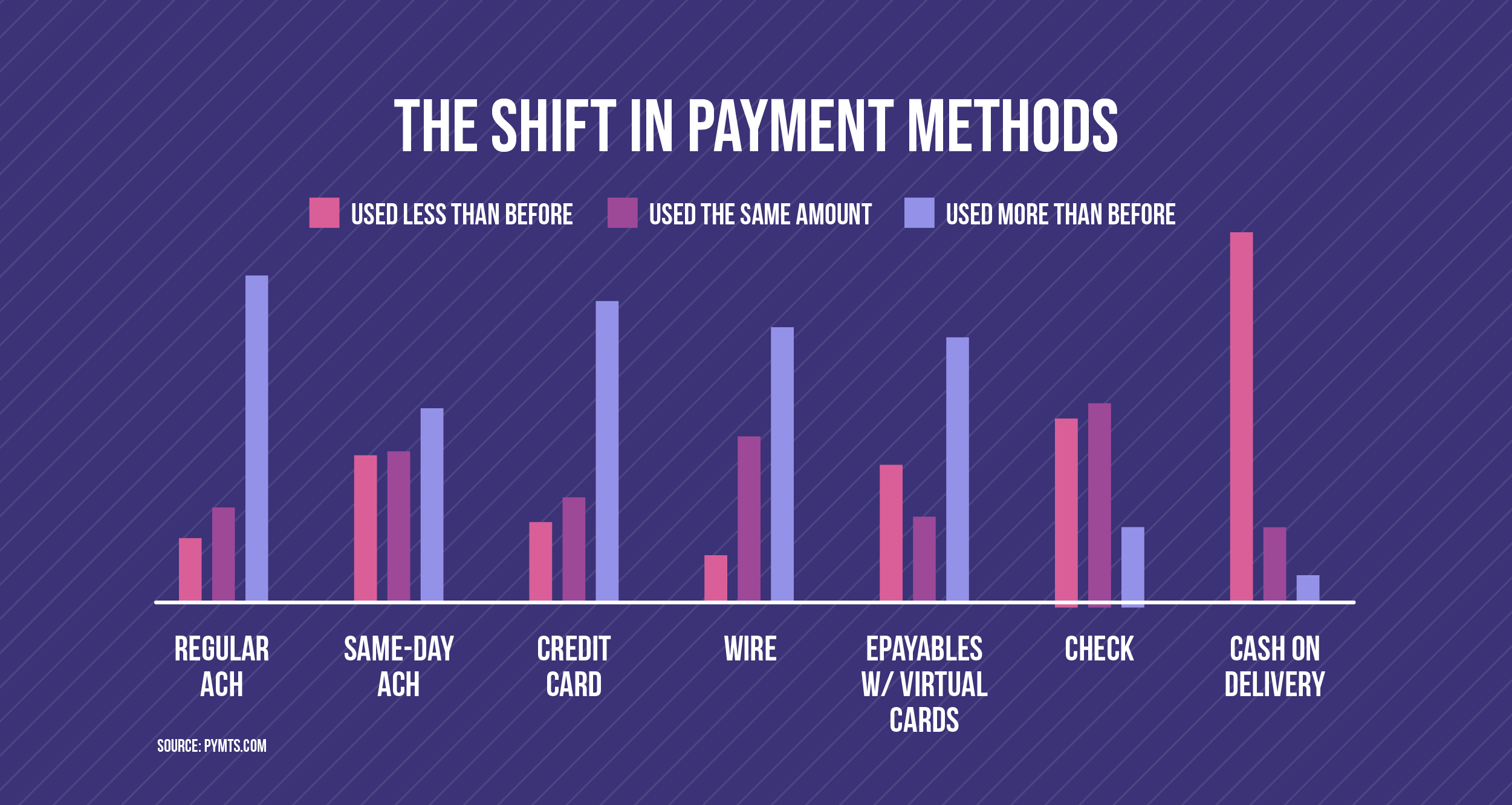

The use of ePayables and virtual cards for B2B payments is growing, and they are quickly becoming an alternative to checks and ACH in the accounts payable payments process. A 2021 study by Juniper Research predicts that the global value of virtual card transactions, including ePayables, will grow from $1.9 trillion in 2021 to $6.8 trillion in 2026. And a 2022 report by PYMNTS.com indicates that 55% of CFOs now use ePayables more frequently, and 40% have reduced their paper check usage.

CFOs have expressed increased interest in adopting electronic payment methods, with 47% saying that increased efficiency was driving their decision to move to automated payment solutions. According to a 2021 survey of AP departments by Stampli, 61% of companies make virtual card payments, and 63% have a program to convert suppliers to accept virtual payments.

This article will look at how ePayables work, their pros and cons, and how you can incorporate ePayables into your current AP process.

How ePayables Work

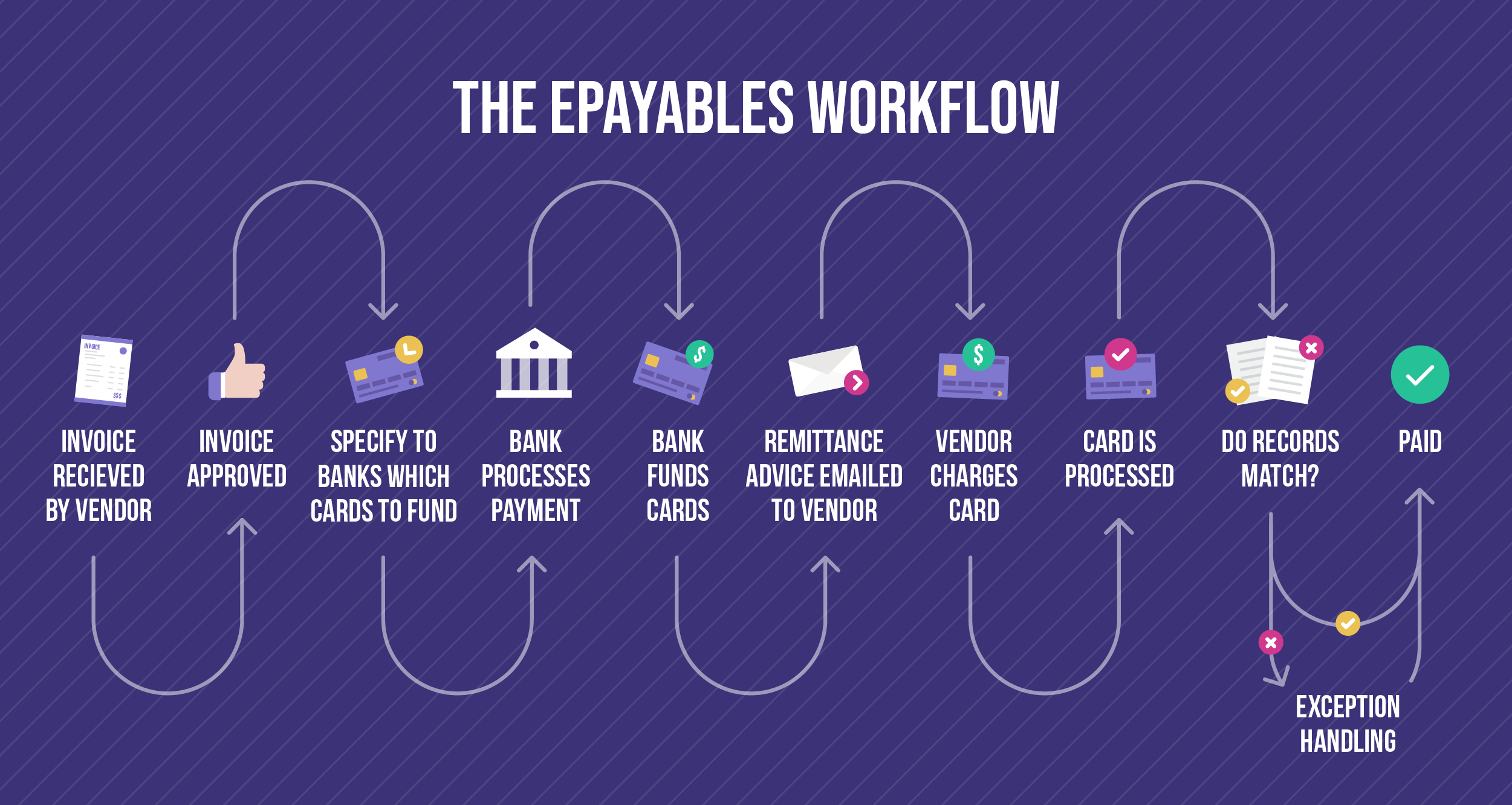

The ePayables process begins when the buyer or their ePayables provider enrolls the supplier in the program and provides them with a dedicated or single-use ePayables card account number. After enrollment, the supplier keeps the account information on file for future reference. When the buyer makes a purchase, the supplier sends them an invoice. The buyer’s AP department enters, reviews, and approves the invoice. Once the invoice is approved, the buyer sends payment information to the financial institution or ePayables provider, who then funds the supplier’s card by the exact amount and sends them a remittance advice. The supplier processes the payment by charging the virtual card for the invoice amount.

Benefits of ePayables

As the use of ePayables expands, it’s important to understand the advantages of using them to pay suppliers. ePayables can provide several benefits to both buyers and suppliers through increased efficiency and transparency in the payment process. Here are some of the main benefits:

Expedited Receipt of Cash and Improves Cash Flow

ePayable payments can reduce Days Sales Outstanding (DSO) for the supplier’s payments. Payments are generally available within 2 business days, compared to 3 to 5 days for ACH payments and 1 to 5 days for checks to clear. When you pay vendors faster, you’ll maintain a better vendor relationship.

Reduces Processing Costs and Streamlines Payment Administration

Virtual card systems automate and replace inefficient manual processes by integrating directly with your ERP and accounting systems. As a result, ePayables are faster and easier to process than paper checks, saving time and money and getting vendors paid on time. In addition, reduced dependence on paper-based processes minimizes the risk of errors and fraud, as well as the cost of organizing and storing paper documents.

Improves Data Quality and Analysis

Payment systems with analytical functionality, such as Stampli Insights, let you get payment data instantly, make informed decisions, monitor and control spending, and avoid duplicate payments. You can also access detailed information on supplier accounts and enhanced remittance information to provide more efficient back-end reconciliation and improve your ability to negotiate volume discounts with suppliers.

Bank reconciliations for ePayables payments are faster than the more complex reconciliations for checks and ACH transactions. Because check and ACH payments require more time, the transactions may still be in process at month end, creating more reconciling items to track.

Rebates on Spending

Some ePayables programs let you earn rebates or financial incentives based on your total spend amount, opening up an additional revenue stream.

Advanced Transaction Controls and Security

Virtual cards provide high visibility and control over transactions to help AP teams reduce errors and prevent fraud. For example, Stampli Card lets you assign spending limits by the cardholder, category, or other criteria. Users can also cancel cards during approvals, in response to failed payments, or even before a card is used. ePayables also replace paper checks, further reducing the risk of fraud.

Reduces NSF and Late Payments

ePayables significantly reduce the frequency of late or NSF payments to suppliers, benefiting supplier relationships and reducing NSF and late payment penalties.

With such clear advantages, ePayables are a potentially valuable payment method for any business that wants better control and visibility over its spending. So what are the challenges of adopting an ePayables solution for your business?

Challenges with Adopting and Implementing ePayables

In “How and Why Companies Choose Payment Types,” Stampli learned that only 4% of AP departments surveyed used virtual cards for supplier payments. So ePayables have all these advantages, why do so few companies use them today? And more importantly, how can your business overcome these challenges to take advantage of ePayables?

There are two main reasons why the adoption of ePayables has been slow: lack of internal buy-in and support for implementing ePayables as a payment method, and supplier resistance to adopting ePayables as a preferred method of payment. We’ll break these down for you.

Lack of Internal Buy-In

Stampli’s survey also revealed two interesting facts: 31% of companies surveyed said they used a payment method because “we’ve always done it that way,” and 23% said it was for the convenience of their AP staff. These results reveal significant internal resistance to adopting any new payment type, not just ePayables. So how do you move forward?

Implementing ePayables requires changes in business processes and integration of business systems that impact departments across the organization. To succeed, you need buy-in from every affected department, including procurement, AP, accounting, IT, and senior management. That means developing a business plan that indicates the benefits ePayables can bring your business through reducing costs and risks, improving supplier relationships, enhancing data collection and analysis, and improving process efficiency. Once you complete the business plan, it’s a matter of securing buy-in from each affected department.

However, internal implementation is only half the battle. There remains the potentially more challenging job of getting suppliers on board.

Getting Suppliers on Board With ePayables

Although ePayables bring some significant benefits to suppliers, supplier resistance to adopting ePayables can be challenging. Since suppliers are much more likely to adopt an ePayables program if they can see real benefits, your ePayables business plan needs to balance the benefits of adopting ePayables for your business with the benefits to your suppliers.

Your ePayables solution is only effective if suppliers get on board, so you must develop a strategy to convince suppliers to participate. You can do a couple of things to make this work for your business.

Start by creating a short list of suppliers most likely to accept ePayables, with whom you can maximize mutual benefits, and who are most critical to your business. To get started, add suppliers that fit these scenarios:

- Suppliers who already accept virtual cards or ePayables and are familiar with the benefits

- One-off high-value purchases because virtual cards can eliminate financing and contract requirements

- High cost of capital because ePayables can expedite payments faster than other credit options

- Long payment cycles or DSO where ePayables can shorten the payment cycle

- Competitive sectors where suppliers may be willing to accept ePayables to retain or grow business

- Upcoming contract renewals where you can make ePayables a requirement under the new contract

Then with your shortlist in hand, define your goals and success criteria for implementing ePayables with your suppliers. Include specific and realistic metrics such as the number of check payments to eliminate, the payment amount you can convert by engaging each supplier, and the percentage of suppliers who you need to adopt ePayables to make the implementation feasible. Also include timelines for transitioning key suppliers and forecasts of when your business will see benefits from each transition. Your ePayables provider may also be able to advise you on other ways you may be able to engage suppliers, such as incentive packages.

Ensure your strategy includes the flexibility to adapt as you add new suppliers, or if your procurement needs change.

Once you’ve developed your business plan, begin reaching out to suppliers to get them on board.

Empowered ePayments with Stampli Direct Pay and Stampli Card

Stampli’s newest payment innovation combines the flexibility of Stampli Direct Pay and the power of Stampli Card into the most intelligent and versatile ePayables solution on the market. We enable your AP team to code, approve, and pay supplier invoices with Stampli Card, ACH, and check, all within the award-winning Stampli AP automation platform.

When you use Stampli Card, your vendor invoices are paid instantly, and payment approval is based on the payment account (credit line). Each payment account has a reference number, and Stampli Card payments are automatically approved or canceled following your approval workflow. You can choose to notify vendors of Stampli Card details via a remittance advice email or through the payment banner in the Stampli Vendor Portal.

Here are some of the key benefits:

Take Control, Speed Up Processing and Reduce AP Workloads

Maintain precise controls over your credit card spend. Use Stampli to take control of AP, speed up payment processing, and reduce the hours required to process AP. Simplify your month-end reconciliation and close your books faster by shifting payments to Stampli Card and reducing the number of items you need to monitor.

Make Informed Decisions with Actionable Data

Stampli’s Advanced Search feature empowers your AP team to cancel Stampli Cards during approvals, in response to failed payments, or even before a card is used.

Pay Vendors Fast

Pay vendors faster than ever to improve supplier relationships and take advantage of early payment incentives, credit card rebates, and rewards.

When you use Stampli’s AP Automation, you’re better positioned to scale your business and process more transactions. Contact us today to find out how Stampli can improve business results.