Where’s Your Money Going? Business Expense Accounts Explained

Every business spends money to make money. Companies use expense accounts to track and manage their expenditures during a specific financial accounting period. It’s essential to understand the different types of expenses and expense accounts, how expense accounts are created and managed, and how they affect your business.

In this podcast episode, Rachita Sundar, SVP at Hubspot, explains how detailed planning is the key to scaling a business. Expense account management is an important component of your plan.

Expense accounts are a way to organize and fund your company’s expenditures, identify and track different expense categories, and help manage large expenditures such as payroll. This article will explain expense accounts and take you through the basics of how you can implement and manage them in your business.

What are Expense Accounts, and How Do They Work?

In a double-entry bookkeeping system, there are four account categories used to track income and expenses. These accounts form the company’s general ledger and financial statements and change via debits and credit entries:

Expense Accounts

The record of your business expenses for a given period.

Income Accounts

The amount of sales revenue, gains on asset sales, and other income generated during a given period.

Asset Accounts

The value of the assets the business holds. Assets are resources used to generate revenue.

Liability Accounts

Amounts owed by the business, including accounts payable and long-term debt.

Businesses use expense accounts to track spending. Each time the business spends money on a product or service, it records a debit in the associated expense account, increasing the account. When the business credits an expense account, the account balance decreases. Expense accounts are considered temporary accounts. They are usually kept open for a specific time period (month or year), then the business closes the expense account balances to net income, and the company begins the new period with zero balances.

Companies include expense accounts in the profit and loss (P&L) statement, also known as the income statement.

Most business activities have corresponding costs. For example, if your company sells products, the corresponding cost would be the cost of producing those products. If you sell services, the corresponding cost would be the cost to deliver the services. These expenses are generally known as the cost of goods sold or the cost of sales.

In addition to the cost of sales, there are other expenses that a business incurs for operations, payroll, marketing, and other business activities. Expense accounts are how you track and manage these costs.

There are several ways that expenses can affect your business. Each expense causes a decrease in your company’s financial resources. This decrease can take the form of a decrease in assets or an increase in liabilities. For example, when your company incurs an expense, it usually pays cash, decreasing assets. You may also choose to use other assets to pay expenses or incur a liability in the case of accrued (unpaid) expenses. Expenses may also result in a decrease in equity or an increase in borrowing.

Expense accounts are considered temporary and closed at month end. They show debit balances that help determine the profitability of a company. Accounting professionals subtract expenses from a company’s overall revenue to calculate net income.

Most businesses categorize expenses by expense type and business activity. How you categorize your expenses will depend on what products or services you sell and your business operations.

Categories and Types of Expenses

Expenses are generally broken down by category and type. The expense category is determined by the business activity the expenses support, and expense types are determined by the actual product, service, or operational costs being incurred.

Expense Categories

Expense categories group expenses by their associated business activity in income statements and financial reports. Grouping expenses into categories makes it easier to calculate profits and understand the business’s financial health. There are several different ways to categorize your business expenses:

Cost of Goods Sold/Cost of Sales

Cost of goods sold or cost of sales are the expenses directly related to the sale of products or services, respectively. Each company defines these costs differently based on what they sell and how they produce or deliver it.

In most cases, the cost of goods sold or the cost of sales includes material costs and labor costs. For companies that offer goods, costs of goods sold usually also includes manufacturing and supply costs. For companies providing services, cost of sales includes the direct costs of delivering the service.

Operating Expenses

Operating expenses are costs that relate to the company’s main activities outside cost of sales. These are the costs associated with the general operations of the business.

Fixed vs. Variable Expenses

Operating costs are usually made up of fixed and variable expenses. Fixed expenses, such as rent, are constant no matter how much your business sells. Variable expenses, such as direct labor, change based on your sales volume or other factors.

Non-Operating Expenses

Non-operating expenses are costs that aren’t associated with day-to-day business operations. These can include financing expenses and losses from one-time transactions (disaster recovery, unexpected costs, legal costs, etc).

Deductible vs. Non-Deductible Expenses

Some business expenses are tax-deductible, which means you can deduct their costs, or a portion of their costs, from your company’s taxable income and reduce your tax liability. Grouping these expenses makes it easier to estimate your company’s tax liability and file your tax returns.

Types of Expenses

Expenses can also be sorted by expense type, which can help your business calculate the total cost of an expense across your entire business and identify opportunities for cost savings. For example, you might analyze your company’s total energy costs to look for areas where you could reduce costs through improvements in energy efficiency.

Typical operating expenses for a business include:

Payroll

Payments to employees in exchange for their services or labor. Payroll includes salaries, benefits, and payments to hourly workers.

Utilities Expense

Operating costs and associated with utilities like electricity, HVAC, water, and waste disposal.

Rent Expense

Rent or lease expense for property or equipment leased by the business. Some rented equipment, such as construction equipment, may be included under cost of sales.

Travel and Entertainment

Travel expenses include airfare, hotels, and meals associated with employee travel and entertaining prospective customers.

Office Supplies

Costs of supplies and consumables such as stationery, paper, toner cartridges, furniture, etc.

Advertising Expense

Cost of promoting brands, products and services, or the business. This cost can include broadcast and online advertising, direct mail, content marketing, etc.

Training

This category includes employee skills and knowledge development.

Maintenance

Repairs and maintenance of company equipment such as machinery, vehicles, furniture and fixtures, properties, etc. Major repairs can be considered a capital expenditure if they extend the life or capabilities of a piece of equipment.

Bank, Insurance, and Interest Expenses

Fees associated with financial transactions. Includes bank fees, insurance premiums, and interest payments on loans, credit cards, credit lines, and other financial services.

Depreciation and Amortization

The purchase of capital assets is not considered an immediate expense. Instead, the cost is spread over the useful life of the asset. This cost is considered the depreciation expense and is entered into the income statement as an expense. Amortization is a similar expense but is applied to intangible assets, such as software licenses.

License Fees and Taxes

Fees and taxes incurred for the legal existence and activities of the business. These fees include VAT and other taxes but do not include income taxes, which is a separate expense category.

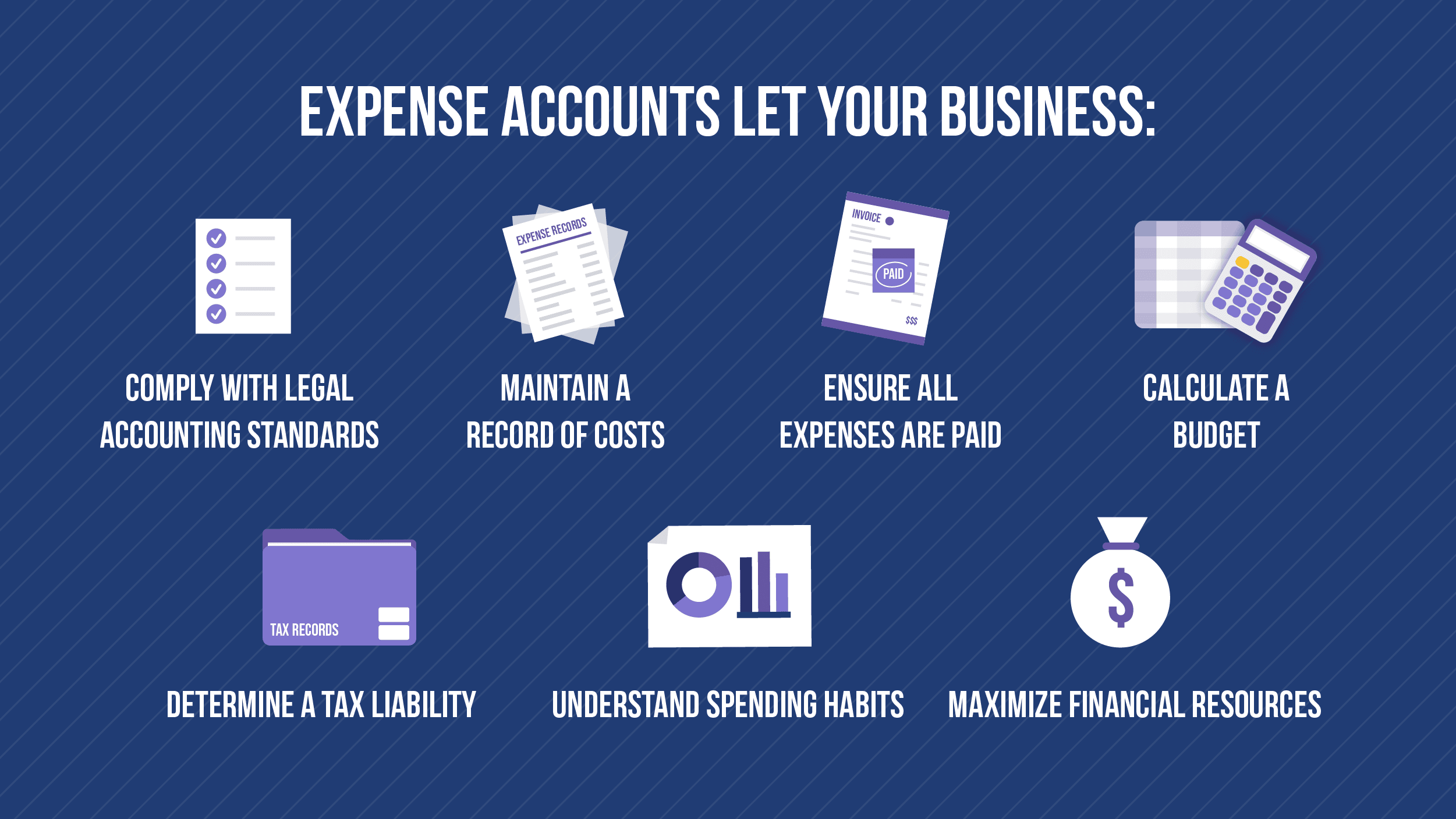

Each business tracks and reports these expenses differently on their income statement, depending on the nature of the business and their reasons for tracking expenses. It’s important to ensure that your business is closely tracking and managing its expenses so you know how money is being spent, and what your future expenses will be. With expense accounts, you can easily track your cash flow and see where your expenditures are going. Tracking your expenses has several benefits to your business:

- It keeps the business in compliance by ensuring that you file correct tax returns and comply with regulations

- It helps your business stay organized and helps managers understand where money is spent

- It helps you reduce or eliminate unnecessary expenses

- It helps you budget for future expenses and plan for future growth

Setting up expense accounts and reporting is a relatively simple but detailed project. The key is to keep everything as simple, clear, and organized as possible.

How to Create an Expense Account Policy

An expense account policy provides the guidelines and processes your business follows when incurring, reporting, approving, and reimbursing employee expenses. Here is a simple four-step process that you can follow to create an expense account policy for your company.

Step 1: Establish Allowable Expenses and Spend Categories

Begin by deciding on and writing down which business expenses you would like to allow, which you would not, and how much employees are permitted to spend. This step will give you the foundation for your list of expense categories. Typical business expenses fall into three main categories:

Fixed Expenses

Expenses that stay the same or change at a predictable rate.

Variable Expenses

Expenses that change periodically over time.

Periodic Expenses

Expenses that are unplanned or irregular and hard to predict.

You can break these core expense categories into subcategories to develop your expense account policy and processes. Categorizing expenses this way will make it easier to track and manage these expenses down the road.

Take a look at these common expense types to determine how you will handle each kind of expense:

Travel & Accommodation:

How are employees allowed to travel? What types of travel are allowed? Which are not? What are considered appropriate hotel accommodations? Do you set a cap on hotel rooms?

Food and Alcohol

What are the spending limits on food and alcohol? Do you allow employees to expense alcohol? Do you have a daily or per-meal reimbursement limit?

Business Purchases

What is your policy for employee purchasing? Do you have a formal purchasing process? Do employees need pre-approval for purchases, and if so, for what amount or type of purchase? What are the spending limits for each employee?

Entertainment

What is acceptable for employees entertaining clients or stakeholders? What are the spending limits?

Mileage

Do you allow employees to use personal vehicles for business purposes? Will you offer a mileage reimbursement? For what amount? (Many businesses use the IRS standard mileage rates)

Other Expenses

Consider other expenses your employees might incur, such as software subscriptions, charitable donations, and incidentals. These small expenses can slip between the cracks and add up to substantial costs if they aren’t carefully tracked.

After you itemize your allowable expenses, you can move on to creating your expense accounts.

Step 2: Set Up Expense Accounts in Bookkeeping

Set up your expense accounts and categories in your bookkeeping system. The structure and organization of your expense accounts can be complex, especially if you deal with numerous categories and subcategories of expenses. As a rule of thumb, it helps to sort expense accounts by category and subcategories. Many businesses also track deductible expenses separately to optimize tax deductions.

Once you’ve set up your accounts, it’s time to write your expense policy.

Step 3: Write Your Expense Account Policy

Begin drafting your expense policy using the spending rules from Step 1. Divide the policy into sections (Travel, Entertainment, etc.) to make it easier to use. Lay out your policy as clearly and simply as possible, and be explicit about what expenses are and aren’t allowed.

Include details about spending limits, disallowed expenses, expected prices or rates, preferred vendors, when preauthorization is needed, and whether receipts are required. It helps to include examples of different expense scenarios so employees know how the policy would apply.

Once you’ve drafted the policy, review it with management and stakeholders to gather feedback and questions. When the expense policy is finalized, ensure that employees can access it at all times and when they’re out of the office. Finally, you should include guidelines for dealing with employees who don’t comply with the expense policy, including what steps managers should take.

Step 4: Design and Implement an Expense Report Process

Before launching your expense policy, design the process and workflows that employees and managers need to follow to report, track, approve and reimburse expenses. A well-designed process ensures that expenses are managed with minimal waste, mistakes, and fraud.

A basic expense report process looks like this:

- The employee reviews the expense policy to see what expenses are allowed and what rules and spending limits apply.

- The employee incurs the business expense(s).

- They complete an expense report detailing the expense(s), along with the business reason for the expense and any receipts or documents, and submit it to their approver.

- The approver reviews the expense report, checks it against the policy to ensure the expenses are allowed, and approves or rejects the report.

- The approved report is forwarded to the Accounts Payable staff, who reimburses the employee for the expense(s)

After the expense report has been processed, the report and documentation are stored digitally for future reference.

Your expense report process may include steps for employees to obtain pre-authorization for expenses, reconciliation of costs to your company budget, expense report and approval templates, and procedures for tracking, analyzing, and reporting expense data.

Review your expense report process regularly after it has been implemented to ensure it’s working smoothly and identify any areas for improvement. You should also regularly review your actual expense accounts against your budgeted expenses to ensure your expenses are within budget and accounted for.

Next Steps: Automating Expense Tracking and Reporting

A well-designed expense account policy and process is an excellent way to control expenses and keep your business financially healthy. However, expense processes can become complicated, especially as your business grows in size and complexity.

At some point, old-school manual processes for tracking and approving expenses and handling reimbursements will become increasingly inefficient. Using manual processes, templates and spreadsheets to record and manage expenses can waste time and resources and can be prone to errors, which isn’t great for your bottom line.

Expense report automation solutions can streamline expense processes and make them more efficient and accurate. One automated solution that is particularly effective at improving expense reporting is the payment card or PCard.

PCards – Empower Your Expense Accounts

PCards are payment cards that your business and employees can use to pay for transactions. PCards can be physical or virtual, but they all serve the same purpose: to provide a controllable, trackable way for businesses to manage employee expenditures.

Pcards have several advantages over other payment methods, such as:

Improved Cash Flow Management

PCards may allow you to extend your Days Payable Outstanding and improve your company’s cash flow.

Low Payment Processing Costs

PCards typically have lower per-transaction costs than traditional credit cards.

Control Shadow Spend

PCards prevent employees from bypassing expense policies and making unauthorized purchases.

More Control Over Spending

You can assign spending limits and other restrictions to prevent overspending and unauthorized expenditures.

Integration with Accounting Platforms

Most PCard platforms can integrate with accounting platforms to automatically update your expense accounts in real-time when expenses are incurred.

Improved Expense Data Reporting

Collect expense data in real-time and analyze it by expense type, category code, location, and more.

Bottom Line: PCards provide real-time, accurate, and categorized expense data to keep your expense accounts current, so you can check your company’s financial health at a glance. They’re one of the best investments in expense management for your business.

Stampli Card – AI Empowered Payment Management

Stampli Card is an AI-powered PCard platform that lets you track, record, organize, and analyze your expense account data in real-time. Stampli Card comes with an easy-to-use, informative dashboard that lets you check your expense accounts at a glance, anytime and anywhere.

With Stampli Card, you can control expenses and approvals to streamline processes, reduce risk, and ensure accurate, real-time expense data reporting. Stampli cards can be customized and assigned by employee, category, project, location, or vendor, and you can set individual spending limits to keep costs under control.

Get a free demo of Stampli Card and empower your expense accounts today!